Duolingo: Is it AI-resistant?

[First Take] Duolingo, Inc. (DUOL US)

About (07 May 2026)

Share price: USD 113.61

Market capitalisation: USD 5,293 mn

Enterprise value (EV): USD 4,134 mn

Average daily volume (ADV): USD 293 mn

NTM P/E: 16x

Time spent: 1 day

My decision

Pass

Background

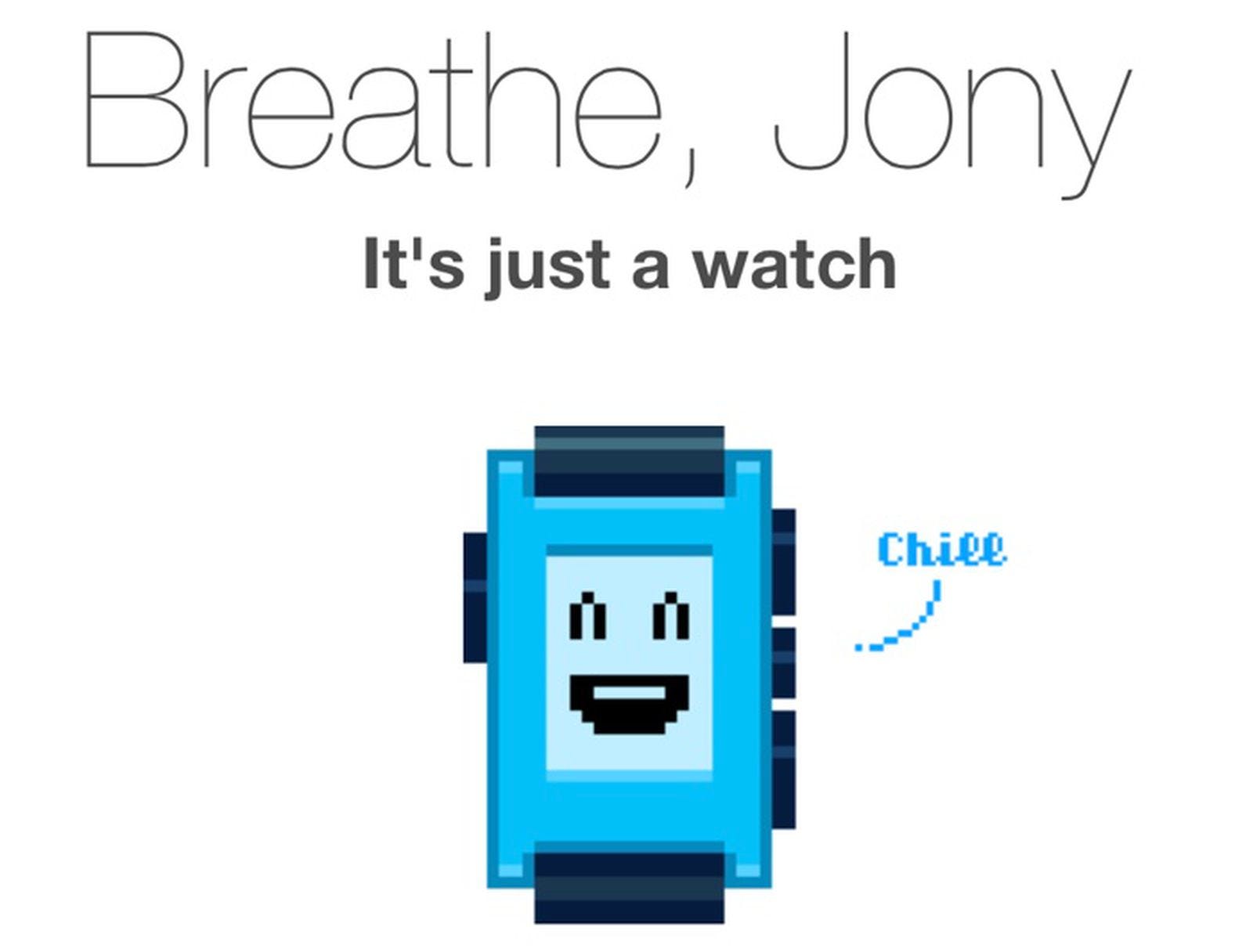

In Apr 2015, Tim Cook launched the Apple Watch.

This looked like a huge threat to Pebble, a smartwatch pioneer.

Eric Migicovsky, the CEO of Pebble, brushed these concerns aside. Migicovsky revealed that Pebble’s sales continued to increase, experiencing a double-digit percentage growth. “Apple Watch had no material impact.”

By Dec 2016, Pebble had shut down.

In Nov 2022, OpenAI released ChatGPT.

The bulls argue generative AI cannot replace the gamified and social experience Duolingo offers. “Look at how DUOL grew its revenue by +41% p.a. since 2022!”

Is Duolingo really AI-resistant?

I am not sure.

In my latest post, I explain why I believe generative AI threatens Duolingo’s business model, but not in the way that most investors think. I also highlight some early warning signs.

Business model

Breakdown of 2025 revenue (USD 1,038 mn; +39% YoY):

84% Subscription (+44% YoY)

8% Advertising (+45% YoY)

4% Duolingo English Test (-8% YoY)

4% In-App Purchases (+5% YoY)

DUOL earns subscription revenue mainly through two products: (a) Super Duolingo and (b) Duolingo Max. These products unlock additional features such as Video Call, where subscribers can practice speaking with Lily, an AI persona.

Subscribers pay in advance. DUOL offers monthly or annual subscriptions. DUOL also offers an annual family plan, which includes up to six users on one subscription.

DUOL also earns revenue from in-app purchases (IAP). Users can purchase consumable in-app virtual goods such as ‘energy refills’, which let users continue lessons once they run low on ‘energy’.

DUOL’s main customers are individual language learners. It is especially popular among Gen Z and young millennials. As of 2025, DUOL reported 133 mn monthly active users (MAU), 53 mn daily active users (DAU) and 12 mn paid subscribers.

In 2025, 38% of revenue comes from the United States. This is down from 45% in 2023. The remaining 62% comes from the rest of the world. No other country accounted for more than 10% of revenue.

Public comparables include Chegg, Inc. (CHGG US), Coursera, Inc. (COUR US) and Udemy, Inc. (UDMY US).

DUOL delivers gamified, bite-sized language lessons. COUR and UDMY both focus on professional upskilling. COUR offers formal university credentials while UDMY hosts a crowdsourced marketplace of independent courses.

Finally, CHGG is a student homework-help platform. To survive AI disruption, it is currently pivoting toward career training.

My reasons

Not 100% AI-resistant

Prima facie, DUOL appears AI-resistant. In Nov 2022, OpenAI released ChatGPT. Many EdTech companies suffered.

CHGG’s revenue has declined -21% p.a. since 2022. Its main products were paid homework help and study support. CHGG charged students a subscription fee to see worked solutions, ask questions to human “experts,” and access study materials.

These were suddenly matched or replaced by AI tools that are free, instant, and always available. Students could paste the same questions into ChatGPT and get reasonably good explanations without paying. Even search engines like Google began answering questions directly with AI instead of sending traffic to CHGG.

In contrast, over the same period, DUOL grew its revenue by +41% p.a. It hasn’t suffered the same pain mainly because it offers a gamified and social experience to learning new languages.

One of the most important features is streak. It tracks the number of consecutive days a user has completed at least one lesson. As the streak grows, it transforms into a digital trophy that users are emotionally invested in and afraid to lose.

Streak creates a strong anchor that drives consistent daily engagement. DUOL even offers “Friend Streaks” with up to five people, which increase only when all participating users complete their daily lessons.

Prima facie, there seems to be strong evidence that AI does not impact DUOL.

ChatGPT’s chatbot interface is great for answering homework questions. That’s why CHGG was significantly affected. However, the chatbot interface is not great at replicating DUOL’s gamified and social experience of learning languages.

However, I believe DUOL’s gamified and social experience may only delay the impact of AI. It does not completely remove the AI-disruption threat.

In other words, it seems to me that DUOL is not 100% AI-resistant.

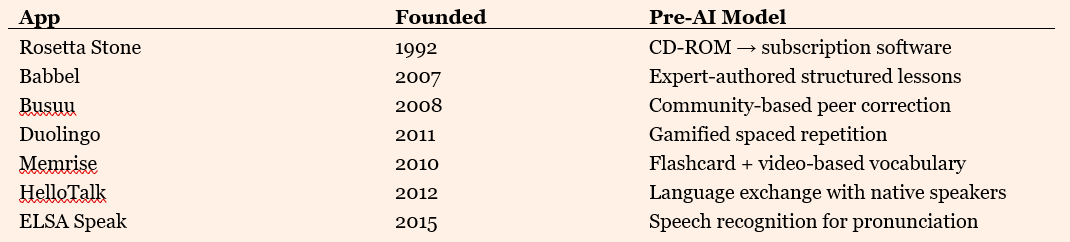

But AI has lowered the barriers to entry. Before generative AI, the language learning app market was dominated by a small set of incumbents that had been around for years. The major players were all well-established:

Source: Perplexity (2026)

There were not many new entrants. Designing lessons was labour intensive and expensive.

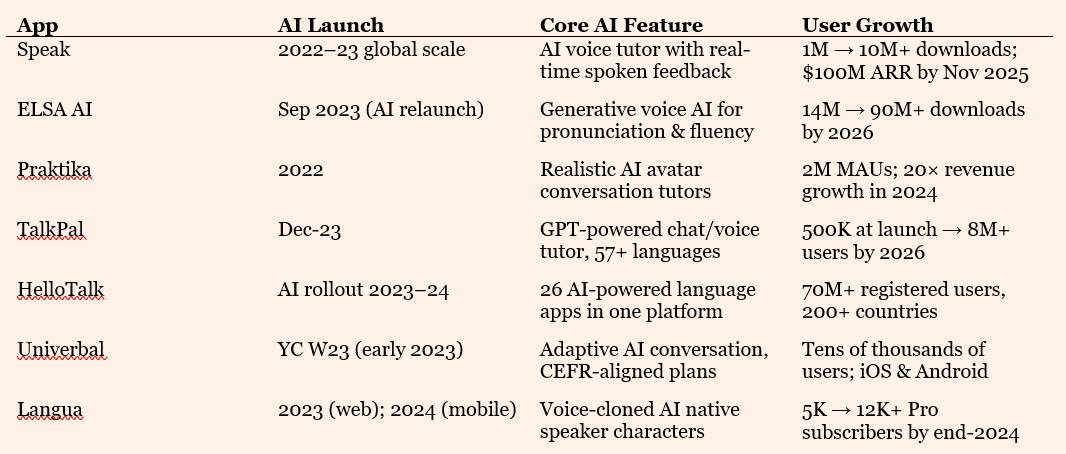

It all changed when OpenAI launched ChatGPT in Nov 2022. Large language models (LLMs) suddenly made it possible for startups to build convincing AI tutors at low cost, triggering a wave of new entrants:

Source: Perplexity (2026)

Early signs of weakness

Bookings growth decelerated. On 4 May 2026, DUOL released their Q1’26 earnings. Their share price dropped as much as -10% mainly because management guided a weak bookings growth in Q2’26.

Are we starting to see the negative impact from increased competition enabled by generative AI?

“Nothing to worry about!”, the bulls argue. Management expects bookings growth to recover and accelerate during the second half of 2026.

I am not so sure of recovery. Humans tend to extrapolate the status quo and fail to recognise paradigm shifts.

In Apr 2015, Tim Cook launched the Apple Watch. This looked like a huge threat to Pebble, a smartwatch pioneer.

Eric Migicovsky, then CEO of Pebble, publicly downplayed these concerns, noting that Pebble’s sales were still growing at a double‑digit rate.

According to Betanews, he said the Apple Watch had ‘no material impact’ on the company and attributed this to differences in their target markets.1

“Pebble is dealing with the threat of Apple’s upcoming Apple Watch by making jokes about the enthusiasm Apple employees have shown for the device.” Source: MacRumors (2014)

In just over a year after Apple Watch launched, Pebble shut down.2

Corporate history is filled with victims of technological change. Pebble is just one of them. Others include Sound Blaster developed by Singapore’s Creative Technologies3 and WordPerfect4, the predecessor to Microsoft Word.

DUOL does not sell watches, sound cards or word processors. I highlighted these examples to show that in most cases, people failed to recognize the paradigm shift until it was too late.

User engagement may have declined. In DUOL’s case, I see a few early warning signs.

Revenue from in-app purchases (IAP) declined -11% YoY in Q1’26. IAP revenue comes from users buying consumable virtual goods such as ‘energy refills’.

This decline is inconsistent with the supposedly higher user engagement suggested by the improvement in DAU/MAU ratio.

High short interest. There is increasingly more short selling of DUOL. By 15 Apr 2026, the short interest in DUOL has increased from 3.7% to 20.0%. Such extraordinarily high short interest suggests high conviction on the part of short sellers.

Factors that could lead to a re-assessment of my decision

New entrants fail to gain meaningful market share in the next 3 to 5 years.

Bookings growth accelerates more than expected.

Sustained growth in IAP revenue.

Coming up next

ThaiBev: When will the hangover stop?

It’s 2016. You’re lying on the beach in Phuket. Hot sweltering heat. Cold refreshing beer. Paradise on earth.

Back in your office, you discovered Thai Beverage Public Company Limited (Y92; THBEV SP) is the brewer of your favourite beer in Thailand. Chang and its rival Singha form a duopoly that dominates the beer market.

Your heart skipped a beat when you realised ThaiBev is listed on the Singapore Stock Exchange. Despite its seemingly expensive NTM P/E of 20x, you bought a significant block.

After all, you know the product well. The company has steadily grown its revenue by ~6% p.a. over the past 10 years. Surely, 20x P/E is not that expensive for such a quality stable stock?

Fast forward 10 years, you’ve suffered a total loss of -20%.

What happened?

More importantly, with its NTM P/E at all-time low of 9x, is ThaiBev finally cheap enough to buy?

I’ll discuss this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in DUOL, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.

I think it’s far worse as a user experience than it was 10 years ago

Great read! I share your concerns regarding the AI resistance of the business model. Predicting the future here is very difficult which is why I rely on the financials.

I recently looked at DUOL applying my Financial X-Ray methodology that translates financials into visible fair value and found that margins, cash flow and capital efficiency are strong while only growth is normalizing. I see the stock trading below its fair value.