3 more interesting ideas

UK’s top pet retailer and vet operator; Indonesia’s largest sports retailer; Australia’s top pathology lab

I am back with 3 more interesting ideas.

As usual, let me know which idea looks the most interesting. You can vote using the poll at the end of this email.

I will look deeper into Craneware plc (CRW LN) this week. This was the idea you and I voted the most interesting last week.

After CRW, I will either share how I use working capital trends to forecast the semiconductor cycle, or why I invested in China Sunsine Chemical Holdings Ltd. (QES; CSSC SP).

I am still deciding. If semiconductor or QES will be more useful to you, reply to this email and let me know.

If you missed it, my previous post explained why DiDi is not dirt cheap, despite price-to-sales of only 0.4x. Grab and Uber trade at 3.6x and 2.5x.

Happy start to the week!

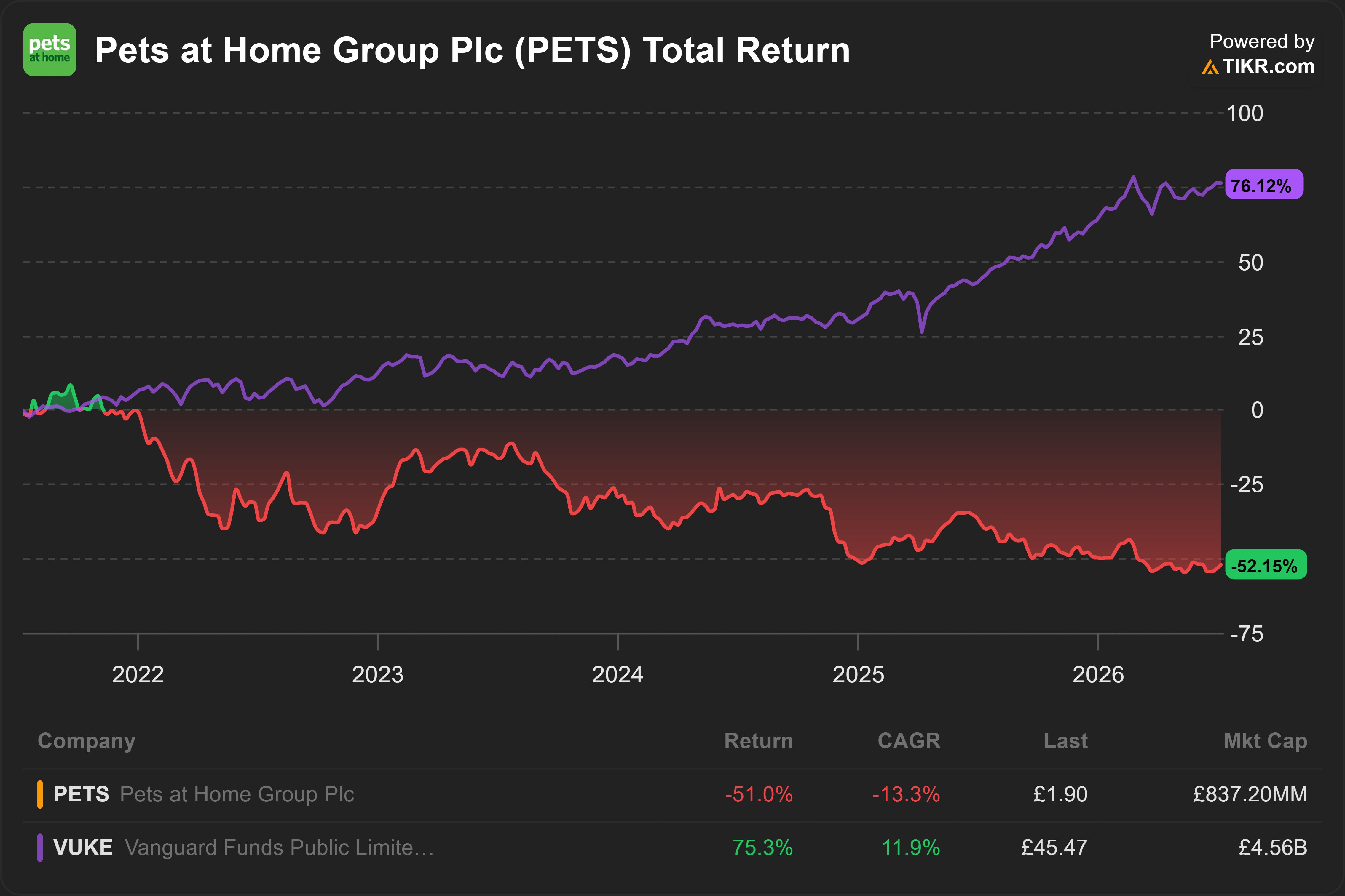

Pets at Home Group Plc (PETS LN)

About (10 Jul 2026)

Share price: GBP 1.90

Market capitalisation: GBP 837 mn (USD 1,122 mn)

Enterprise value (EV): GBP 1,194 mn (USD 1,600 mn)

Average daily volume (ADV): GBP 3 mn (USD 4 mn)

NTM P/E: 12x

PETS is one of the largest pet retailers and vet operators in the UK. It holds ~ 20% market share.

My initial estimate suggests ~ 9% free cash flow yield on EV, which is an attractive ~4% premium over UK 10y gilt yield.

Hidden asset?

Retail segment obscures growing Vet segment. Group underlying profit before tax (PBT) declined -30% in FY2026. Vet segment grew +10%. However, this growth was hidden by Retail segment’s -58%.

Group underlying PBT is also weighed down by startup costs at the Insurance segment. More on this later.

Good business, temporary headwinds?

Retail segment holds the largest market share in the UK.

Recently, this segment faced competition from discounters, a slump in high-margin accessories, and a messy distribution center consolidation.

However, early signs of recovery are finally breaking through. Logistics bottlenecks have finally eased. Retail revenue returned to +2% YoY growth in Q4’FY26. Price cuts increased volume more than proportionately.

Under-recognised growth?

The consensus seems to be under-estimating growth potential from cross-selling.

PETS will start selling pet insurance. In 2026, it received regulatory approvals from the Financial Conduct Authority (FCA). PETS estimates ~ GBP 2 bn market opportunity.

Takeover?

In Feb 2025, PETS share price spiked on rumours that BC Partners, a private equity (PE) firm is preparing a bid.1

The conclusion of the CMA’s veterinary market probe in Mar 2026 clears a significant roadblock for a takeover.

Factors to focus on

How likely can PETS sustain the recovery in Retail?

How much growth can PETS enjoy from cross-selling other products like pet insurance?

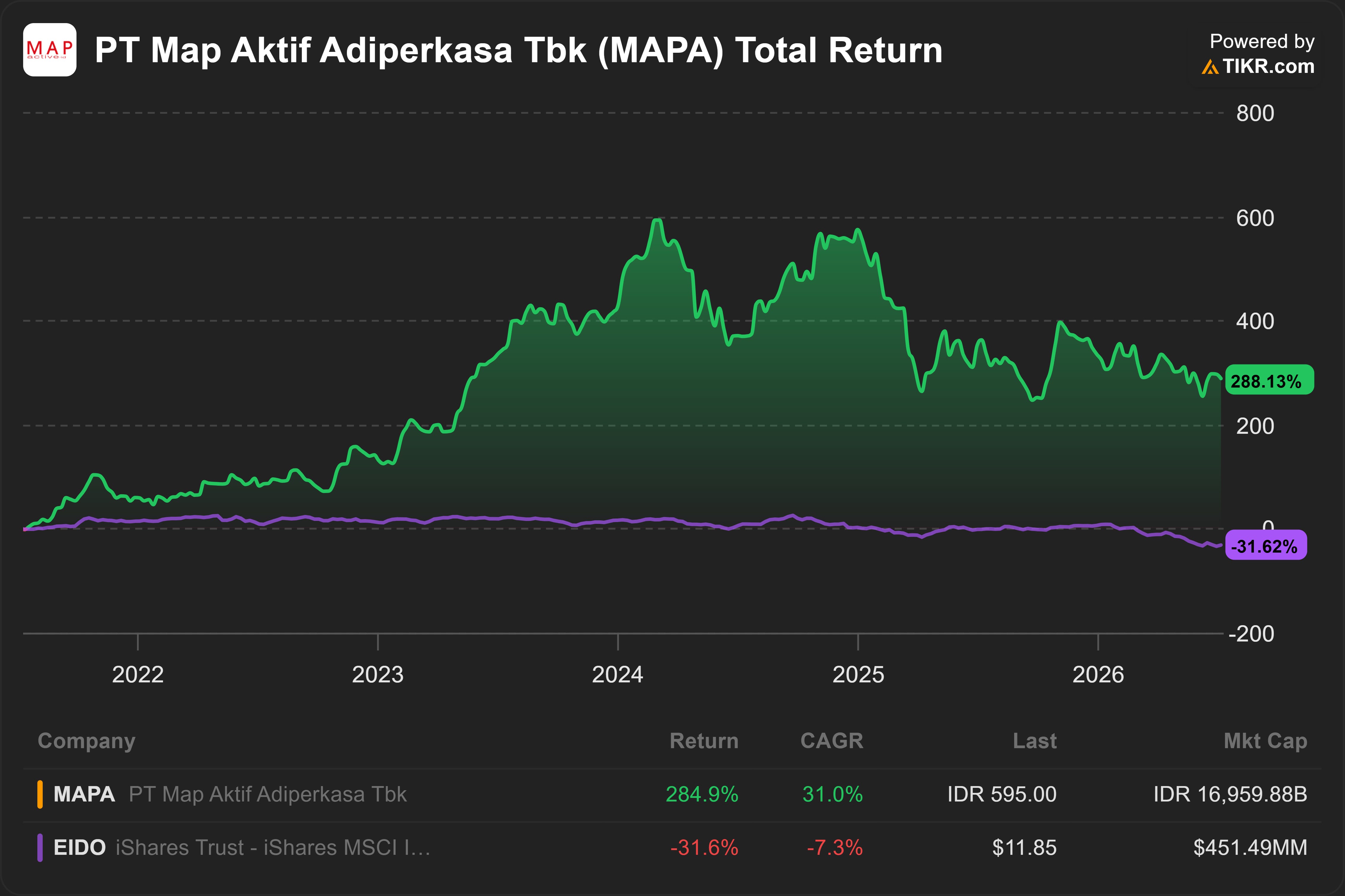

PT Map Aktif Adiperkasa Tbk (MAPA IJ)

About (10 Jul 2026)

Share price: IDR 595

Market capitalisation: IDR 16,960 bn (USD 939 mn)

Enterprise value (EV): IDR 17,561 bn (USD 972 mn)

Average daily volume (ADV): IDR 15 bn (USD 1 mn)

NTM P/E: 9x

MAPA is the largest sports retailer in Indonesia, with ~60% market share. The next closest competitor has only ~5% market share.2

My initial estimate suggests ~ 10% free cash flow yield on EV. This looks attractive, given EPS could grow ~12% per year over the next 2 years.

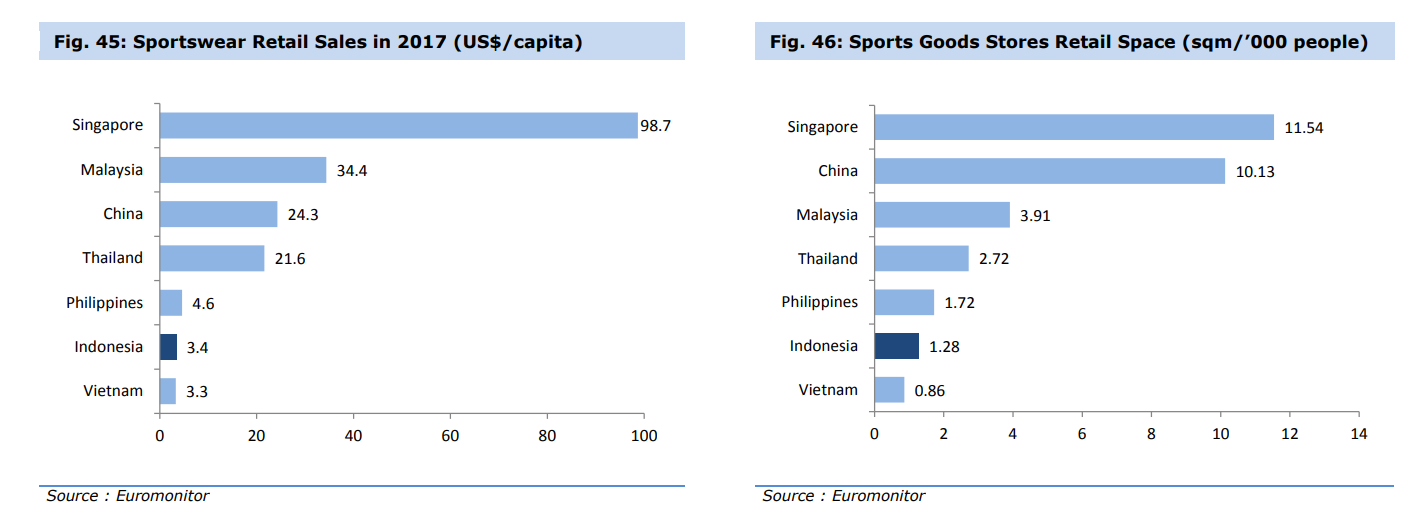

Under-recognised growth?

Under-penetration. According to Euromonitor, sportswear retail is underpenetrated in Indonesia.

Though this is the most recent data I could find, the Indonesian market likely remains underpenetrated:

Source: IndoPremier (2019)

Limited competition. Regulation restricts foreign competition.

Indonesia’s retail foreign ownership rules (GR 29/2021, Omnibus Law) govern retail market entry:

Stores < 400 sqm: Closed to foreign investment entirely. All must be 100% locally owned

Stores 400–2,000 sqm: Previously capped at max 67% foreign ownership with a special Ministry of Trade licence. This cap was removed after 2021, but non-mall locations remain reserved for domestic companies

Stores > 2,000 sqm: Foreign ownership permitted but the stores must be located within or integrated with a shopping mall.

Most retail stores in shopping malls are between 100 to 300 sqm. That’s why foreign brands like Nike and Adidas distribute their products through MAPA.

The government restricted the retail market to protect local players. I will be surprised if they liberalise it completely.

Privatisation?

Private equity acquired parent (MAPI IJ). CVC Capital Partners, a private equity (PE) firm, acquired 51% of MAPI in May 2026.3 MAPI owns ~69% of MAPA.

CVC just launched a mandatory tender offer to acquire more MAPI shares at ~11% premium. The offer will run through 17 Jul 2026.4

After the tender offer, CVC may look to increase its stake in MAPA or even privatise it.

CVC is investing in the MAP Group as a strategic investor wanting operational control and ASEAN expansion. A listed structure imposes disclosure burdens, minority veto rights, and valuation scrutiny. This creates friction for a PE owner.

Factors to focus on

Is 190 days of inventory normal?

Global peers like JD Sports Fashion Plc (JD LN) hold only ~ 110 days.

Maybe MAPA needs higher inventory because Indonesia is a large archipelago with less developed infrastructure.

Management seems to be targeting ~180 days.

Is consensus too optimistic over the short-term?

Sell-side consensus forecasts ~+10% revenue growth in 2026, despite management’s guidance for only high-single digit growth.

What will increase penetration?

After 2026, consensus expects revenue growth to accelerate to +13% in 2027.

What will drive the acceleration?

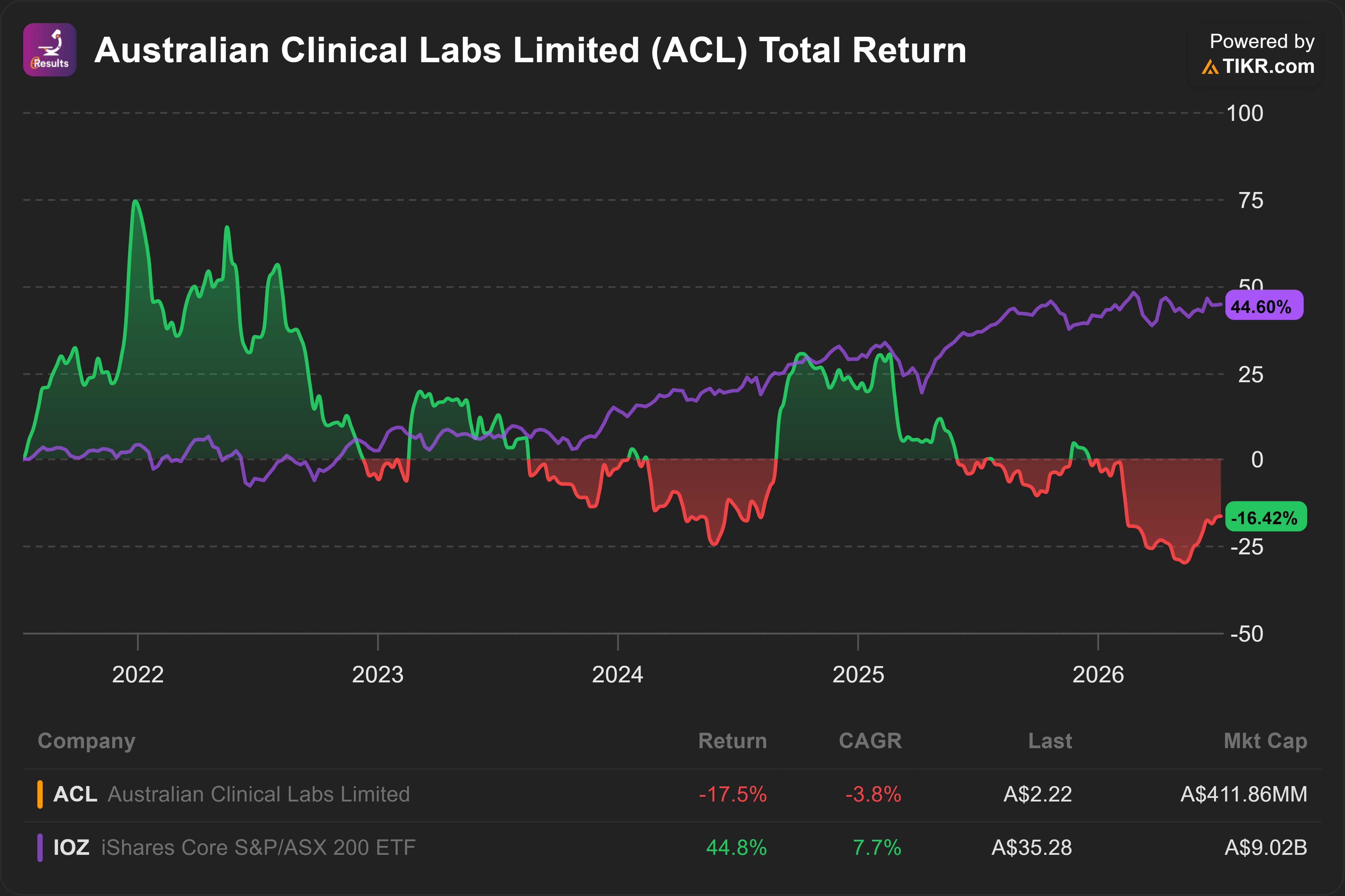

Australian Clinical Labs Limited (ACL AU)

About (10 Jul 2026)

Share price: AUD 2.22

Market capitalisation: AUD 412 mn (USD 295 mn)

Enterprise value (EV): AUD 704 mn (USD 498 mn)

Average daily volume (ADV): AUD 1 mn (USD 1 mn)

NTM P/E: 13x

In May 2026, I published - Australian Clinical Labs: Why I see an opportunity in Australia’s pathology service provider

I now believe the probability of takeover is higher.

ACL appointed Greg Horan as CEO.5 Before ACL, Greg was a Managing Director of Brookfield Australia, a PE firm.6

There has been quite some PE activity within the healthcare space in Australia.

Recently, competitor Healius is looking to sell its bioanalytical laboratory Agilex Biolabs in response to “several unsolicited approaches from credible parties”.7

Vote for the best idea

Vote for the most interesting idea. That may be the next idea I analyse in detail.

Coming up next

Among the 3 interesting ideas last week, you voted Craneware plc (CRW LN) the most interesting.

I agree.

The recent sell-off seems to have squeezed out all optimism.

However, there is a chance that CRW’s headwinds are temporary. Unearned revenue returned to growth (+2% YoY) in H2’25.

Bain Capital offered GBP 26.50 per share in May 2025. The board rejected it. If private equity likes it at GBP 26.50, they’ll like it even more at GBP 11.10?

Is there an opportunity? That’s what I will explore next.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in PETS, MAPA, ACL, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.