3 interesting ideas

Takeover/privatisation targets made me a lot of money. Here's 3 potential targets

I thought investing was fun.

Pick a stock. Read the annual reports. Meet management. Buy. Profit.

As with most things in life, the reality is much harder. If you buy a stock and it drops -20%, you’ll hear the much dreaded ‘ding’ as your boss Teams you. You will probably be forced to sell before your thesis plays out.

That’s the problem.

You need ideas that can make you money but won’t blow you up in the process.

I don’t have a silver bullet. But I have something I believe that’s very close to one: takeover/privatisation targets.

Now, I am not talking about merger arbitrage, where you bet on the successful closing of announced takeovers. People often say this is “picking up pennies in front of a bulldozer” or “earning the last penny from the guy (or gal) who earned the dollar”. I can’t argue with that.

I am talking about the person who earned the dollar. I am talking about companies that have not been taken over but are likely to be.

To attract your attention, let me share two examples.

In Aug 2022, I bought Evergreen Gaming Corporation (TNA CN). This is a small casino in the US. 4 months later, a competitor acquired it. I made +78%.

Last month, FirstCash Holdings, Inc. (FCFS US) offered +35% premium to buy Ramsdens Holdings PLC (RFX LN).

The takeovers were predictable.

FirstCash wants to expand into the UK and had just acquired Ramsdens’ competitor (H&T) in Aug 2025.

Maverick Gaming, Evergreen’s competitor, was on an acquisition spree. It tried to buy Evergreen before, but the deal fell through because of COVID-19. After the lockdowns ended, it revived the takeover.

So, there were signs. Competitors on an acquisition spree, an aging management team /shareholders without clear successor, history of takeover/privatisation attempts, etc.

More importantly, this strategy can be market-neutral. Evergreen contributed a lot to my portfolio’s +7% return in 2022, despite the bear market.

I want to be clear that I am not purely betting on the deals happening. That’s a greater fool game. I buy because I find the stock attractive. The potential takeover/privatisation helps me realise the stock’s value. It’s the cherry on top of the cake.

Enough talk! Let’s run through 3 interesting ideas at a high-level.

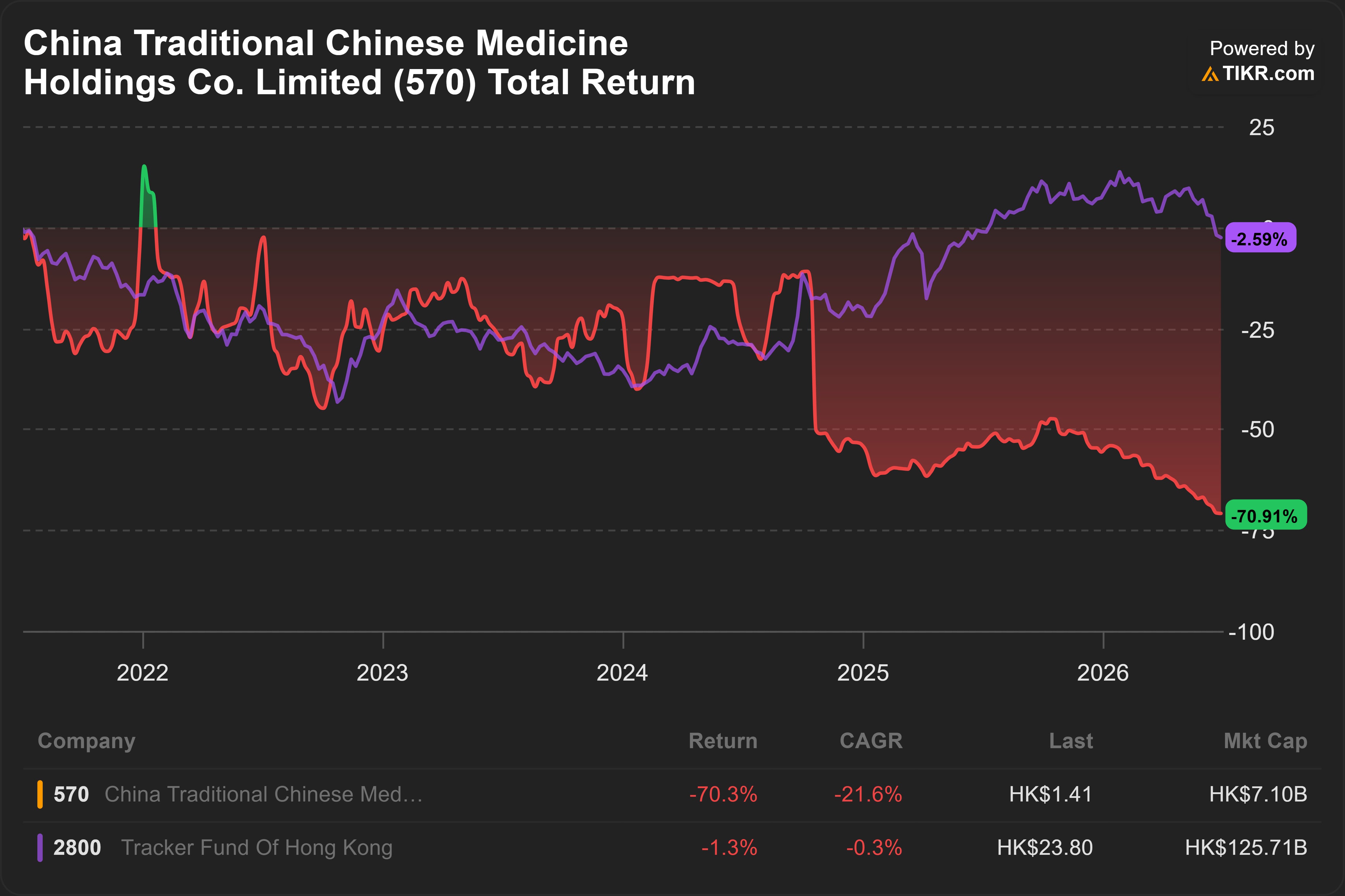

China Traditional Chinese Medicine Holdings Co. Limited (570 HK)

About (3 Jul 2026)

Share price: HKD 1.41

Market capitalisation: HKD 7,100 mn (USD 905 mn)

Enterprise value (EV): HKD 7,012 mn (USD 894 mn)

Average daily volume (ADV): HKD 19 mn (USD 2 mn)

NTM P/E: 9x

China TCM manufactures and sells traditional Chinese medicine (TCM) products, mainly in mainland China.

My initial estimate suggests ~ 8% free cash flow yield on EV, which is an attractive ~6% premium over China 10y government bond yield.

Good business, temporary headwinds?

Regulatory pressures. After Sinopharm’s takeover offer lapsed around late 2024, China TCM’s share price collapsed and continued to decline because of volume-based procurement (VBP).

VBP is a government-led centralized bidding system that forces pharmaceutical companies to cut prices (often 50%–90%) in exchange for guaranteed sales volumes in public hospitals. VBP started targeting China TCM’s products from Aug 2023.

As a result, China TCM’s operating profit declined -40% in 2024 and another -43% in 2025.

Government rolling back pressure. In Oct 2025, Caixin Global reported that China has tweaked the VBP rules and, for the first time, has not publicly disclosed the winning prices.

This signalled a policy shift aimed at easing excessive competition and fears of companies bidding below their production costs.1

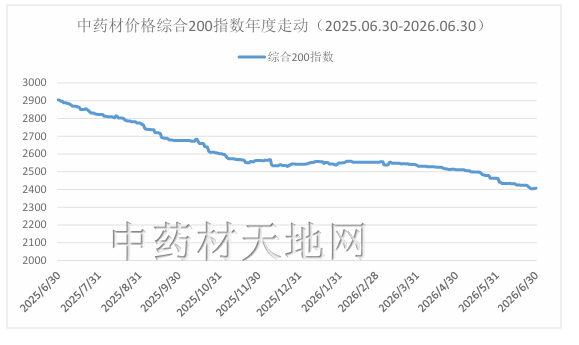

Prices stabilising. In June 2026, the China Medicinal Herbs Composite 200 Index (中药材综合200指数) started showing signs of stabilization.

Source: 中药材天地网 (2026)

Inventory days normalising. Inventory days peaked at around 318 days in 2020 and has returned to ~203 days in 2025. Historical average is ~204 days.

With inventory days closer to a normal level, margins should be near a bottom.

Privatisation?

Largest shareholder wants to privatise. Sinopharm repeatedly tried to privatise China TCM. It holds ~ 33.5% stake.

In 2021, China TCM disclosed that Sinopharm was exploring a privatisation. In 2022, Sinopharm was reportedly preparing a potential offer of ~ HKD 6 per share.2

In early 2024, Sinopharm officially launched a take-private bid at HKD 4.60 per share. This bid ultimately lapsed in late 2024 because it didn’t receive the necessary approvals from Chinese regulators for outbound direct investment.3

Sinopharm can make another privatisation attempt from ~ Oct 2025 onwards.

Factors to focus on

Is pricing pressure from VBP really over?

Receivable days ~ 7 months because they sell to public hospitals, who have strong bargaining power. Benchmark against peers. Is this normal? Collectable?

Why were the privatisation approvals not received?

With the industry downturn, will the regulators be more open to consolidation?

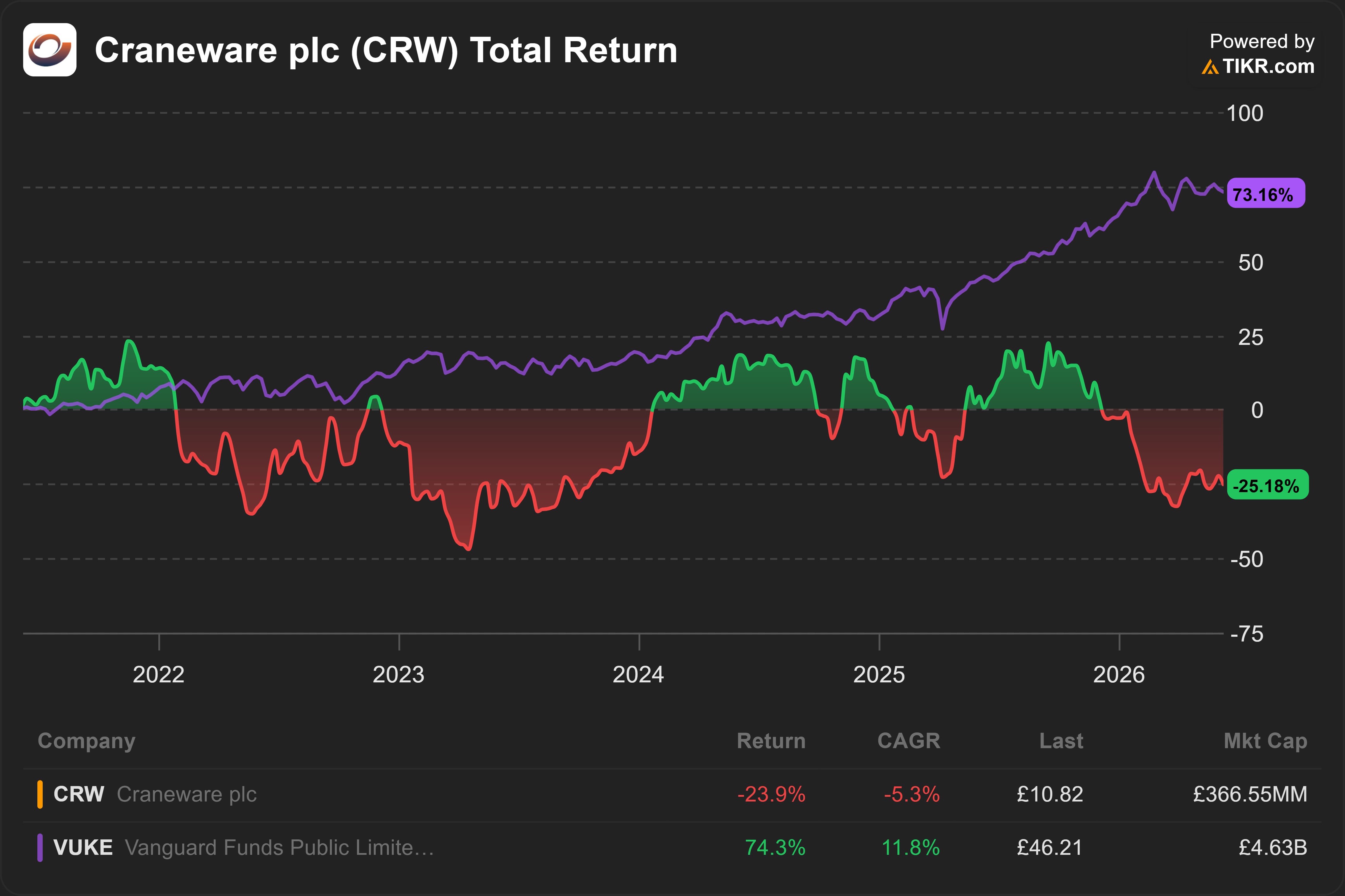

Craneware plc (CRW LN)

About (3 Jul 2026)

Share price: GBP 10.82

Market capitalisation: GBP 367 mn (USD 489 mn)

Enterprise value (EV): GBP 356 mn (USD 476 mn)

Average daily volume (ADV): GBP 2 mn (USD 3 mn)

NTM P/E: 12x

Craneware sells healthcare financial software to hospitals.

Their software make sure the hospital gets paid what they are owed without getting bogged down in messy paperwork or rejected claims. It earns most of its revenue from the US, with ~40% market share.

I estimate ~ 9% free cash flow yield on EV. This is an attractive ~5% premium over US 10y government bond yield.

Good business, temporary headwinds?

Revenue likely pushed into next year. In Jul 2026, CRW announced that their performance during the year ending in Jun 2026 will be below consensus’ expectations. The stock fell -24% in just a day.

The Board blamed slower conversion of 340B opportunities into revenue and the deferral of some enterprise contracts. They expect to recognise these revenues in FY2027 instead.

As a result, FY2026 revenue will likely be flat. Before the update, consensus was expecting revenue to grow ~ +10% in FY2026.

I am surprised that the consensus is surprised. There was advance warning that +10% was probably too optimistic. Unearned revenue declined -2% YoY in H2’24 and another -2% YoY in H1’25.

However, there is a chance that the headwinds are temporary. Unearned revenue returned to growth (+2% YoY) in H2’25.

Takeover?

CRW rejected PE takeover. Bain Capital, a private equity (PE) firm, offered GBP 26.50 per share in May 2025. CRW rejected it. The board argued the offer undervalued the company.4

Today, CRW is trading at GBP 11.10

With the recent selloff, Bain Capital and other PE firms may try again.

Factors to focus on

More details on why customers are pushing their spending into FY2027. Are the issues really temporary?

The company operates a platform for hospitals to automate billing, compliance, etc. Any opportunities to grow through cross-selling, etc?

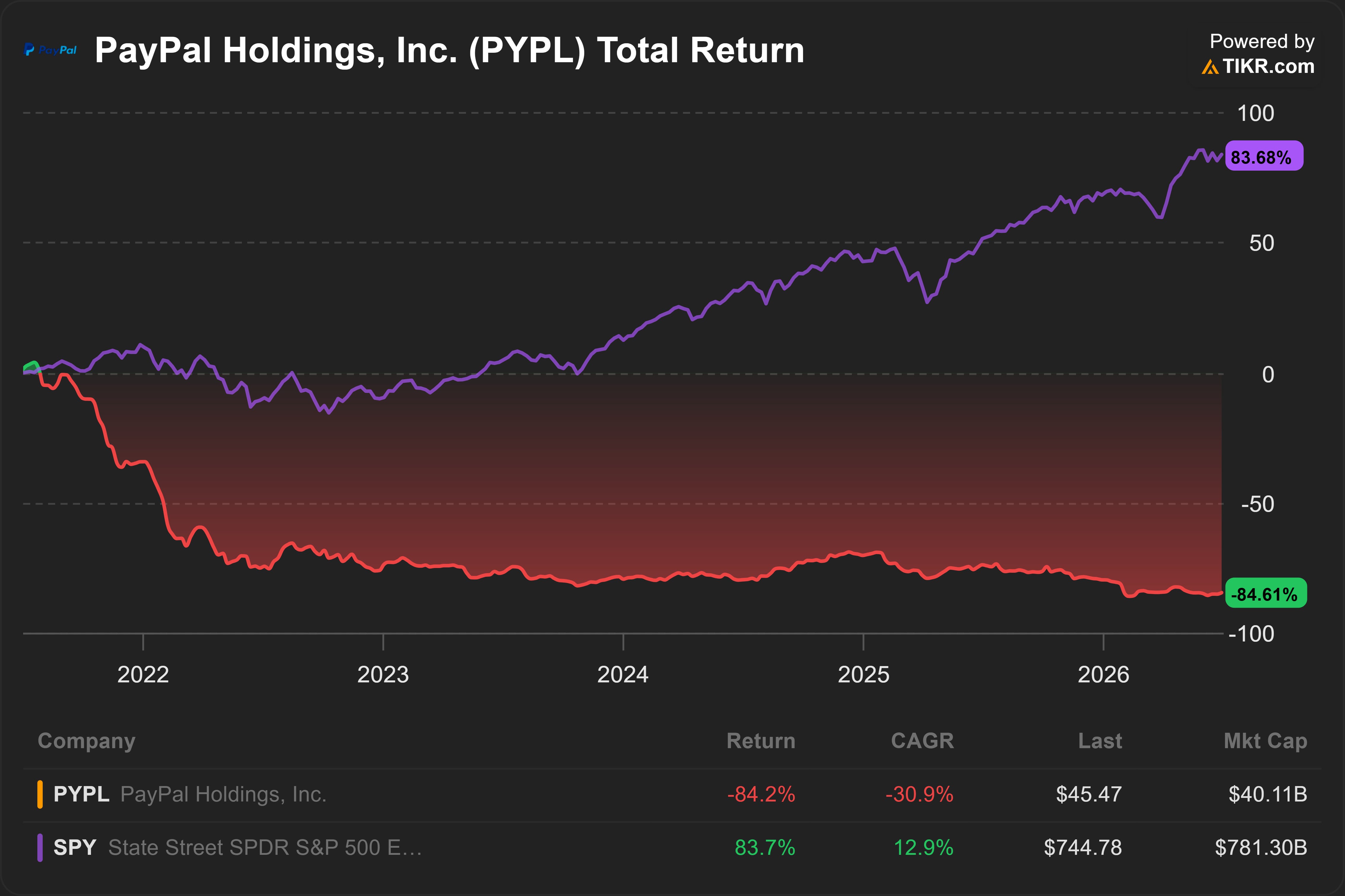

PayPal Holdings, Inc. (PYPL US)

About (3 Jul 2026)

Share price: USD 47.47

Market capitalisation: USD 40,109 mn

Enterprise value (EV): USD 42,437 mn

Average daily volume (ADV): USD 689 mn

NTM P/E: 8x

Last month, I argued why I find PYPL interesting - PayPal: Undervalued at 7.8x P/E?

I now believe the probability of a takeover is higher.

Recently, PayPal shut down its PayPal Ventures. This was its corporate venture arm that makes investments in startups, etc.5 The new CEO has also reorganised the company into 3 standalone segments: PayPal, Venmo and Payment services.

Cost-cutting and streamlining make the company more attractive to buyers and easier to sell.

Private equity is active in fintech. The sector is attractive because of depressed valuations.

In 2024, Advent International bought Nuvei Corporation (NVEI CN).6 Last month, Nuvei announced it will be buying its peer, Payoneer Global Inc. (PAYO US). CVC Capital considered buying Nexi S.p.A. (NEXI IM) earlier this year.7

Email me for 2 bonus ideas

I am actually running through 2 more ideas as I am writing this.

If you would like to hear about them, reply to this email or comment below.

Vote for the best idea

Use the poll to tell me which idea is the most interesting to you. That may be the next idea I analyse in detail.

Coming up next

At first glance, DiDi Global Inc. (DIDIY US) looks very cheap.

EV/Revenue is only 0.30x, compared to 2.5x at GRAB US and UBER US.

However, DIDIY’s true EV/Revenue is actually closer to 1.4x.

The difference is simply because of accounting. DIDIY recognises revenue in a different way than GRAB and UBER.

In my next email, I will explain this in detail.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.