The dating app that's losing its best users first

Bumble lost 21% of its paying users in Q1'26. The decline may be structural.

Summary

BMBL looks cheap. 3x NTM P/E. 23% free cash flow yield on enterprise value.

However, I decided to pass.

Dating apps have a short lifespan. As they grow, they inevitably attract low-intent users, or even bots and scammers. These bad users drive out good singles, causing a vicious cycle of decline.

BMBL seems to be in that decline. In Q1’26, paying users declined -21% YoY.

Unlike MTCH, BMBL does not have a new product like Hinge to drive future growth.

The bulls argue that the founder, who just returned as CEO, will turn things around. I am hopeful, but I could not find meaningful precedents of successful turnaround of such scale.

I believe the consensus is too optimistic, both over the short-term and long-term.

Sell-side consensus estimate is looking for only -13% revenue decline in 2026. In Q1’26, revenue declined -14% YoY while advance payments declined -15% YoY.

Consensus also expects revenue to return to growth by 2028. However, management estimated terminal growth rate at 0% when they tested goodwill for impairment in Q4’25.

Major shareholder Blackstone looks to be preparing to sell BMBL. However, I am not sure whether they can get the price they desire.

About (01 Jul 2026)

Share price: USD 3.23

Market capitalisation: USD 421 mn

Enterprise value (EV): USD 891 mn

Average daily volume (ADV): USD 11 mn

NTM P/E: 3x

Time spent: ~2 days

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Pass

Background

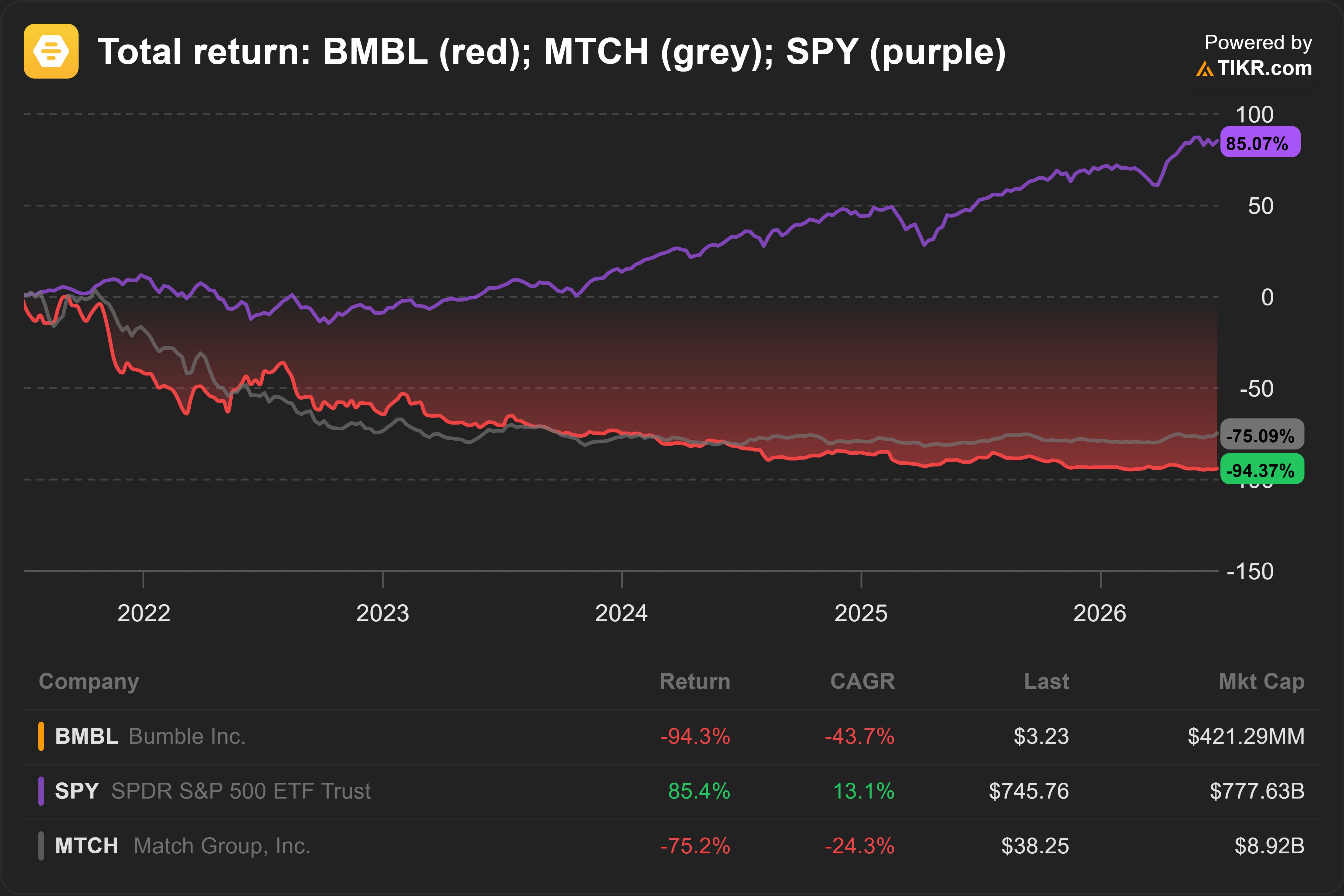

Bumble Inc. (BMBL US) has fallen -96% since IPO.

In Feb 2021, BMBL ended its first trading day at USD 75.

‘Growth’ investors point to its strong network effect, supported by its requirement for women to make the first move.

Today, BMBL is USD 3.

Paying users dropped -12% in 2025, and another -21% in Q1’26.

“Value” investors point to its 3x P/E. What’s the worst that can happen?

Are they right?

Business model

Breakdown of 2025 revenue (USD 966 mn; -10% YoY):

81% Bumble App (-10% YoY)

19% Badoo App and Other (-11% YoY)

The Bumble App segment consists mainly of the Bumble App.

This is a dating app built around a “women-first” design where women must initiate contact, a feature meant to reduce harassment and create a more intentional dating culture. The user base skews towards Western college-educated singles. Average revenue per paying user (ARPPU) ~ USD 27 per month.

The Badoo App and Other segment consists mainly of Badoo, a pioneer of web and mobile dating founded back in 2006.

Badoo is a traditional, high-volume, geolocation-based match-and-chat interface centered on rapid social discovery. It is popular among emerging markets in Latin America, Eastern and Southern Europe. Because of this, ARPPU is lower at ~ USD12 per month.

BMBL operates a freemium model. The basic use of Bumble and Badoo apps is free, but users can buy subscriptions to unlock more features like additional likes or to boost their profile’s visibility.

BMBL earns 44% of its revenue from the US. The remaining 56% is earned from the rest of the world. The US is the only single country contributing >10% of BMBL’s total revenue. Revenue declined -18% in the US. In the rest of the world, revenue declined slower at -3%.

Relevant public comparables include Match Group, Inc. (MTCH US), Grindr Inc. (GRND US) and Hello Group Inc. (MOMO US).

MTCH owns Tinder and Hinge. GRND specialises in dating apps for the LGBTQ communities worldwide. MOMO owns Tantan, known as the ‘Tinder of China’.

My reasons

Dating apps die young

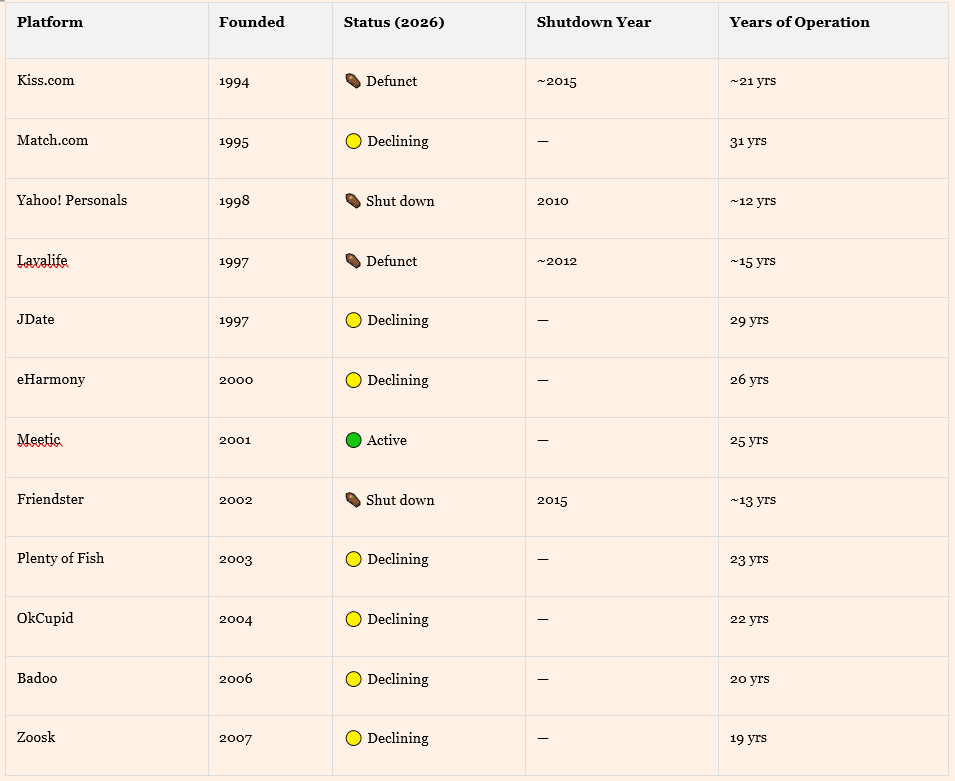

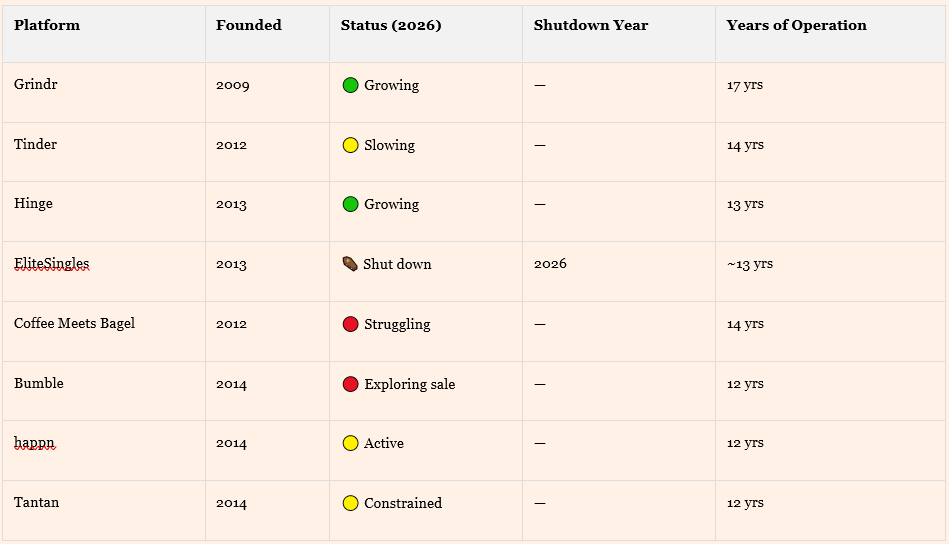

Dating apps have short lifecycles. I asked Perplexity, “Since the Internet started, what are the major dating apps? When did they start, and what’s their status today?”

Here’s what Perplexity compiled:

Source: Perplexity (2026)

The average lifespan seems to be ~15 years. 4 dating platforms shut down around this age. The platforms that survived beyond 15 years are in various states of decline.

The oldest is Match.com, at 31 years old. It is owned by MTCH. However, online reviews are very negative.1

Only two dating apps are clearly growing: Grindr and Hinge.

Why do dating apps die young?

Bad singles drive out good

Gresham’s Law. In economics, Gresham’s Law is the observation that bad money drives out good money.

If people are given two different types of currency that are legally worth the same, but one is secretly more valuable or higher quality, they will hoard the good one and spend the bad one. Eventually, the good stuff disappears from the market entirely.

In its general form, Gresham’s Law suggests when it is easy to flood a system with a low-quality version of something, the people offering the high-quality version will leave the market to protect themselves.

I suspect this is why dating apps live only ~ 15 years, and why BMBL is losing paying users.

Bad singles drive out good. In their infancy, dating apps thrive on a network of high-quality, genuine singles. As the apps scale, however, they naturally attract low-effort users, scammers, and bots. This degradation accelerated during the COVID-19 lockdowns.

BMBL, for instance, aggressively chased user growth by leaning heavily into performance marketing. While paid ads boosted user growth, they inadvertently flooded the ecosystem with low-intent users.

These low-quality users quickly overwhelm the platform with mass-swiping and copy-pasted messages that cost virtually nothing to produce, exhausting the high-intent singles who invest genuine time and emotional energy. Suffocated by dating fatigue, these good singles eventually leave or migrate to newer platforms like Hinge.

Compounding this systemic decay is the inherent irony of the dating app business model. A highly effective dating app naturally loses its best users, as high-intent singles successfully match and exit the ecosystem.

What does this mean for BMBL?

Difficult to estimate future cash flows

Losing users. Since Q1’25, BMBL has been losing paying users.

Source: BMBL, Angsana Anderson estimates

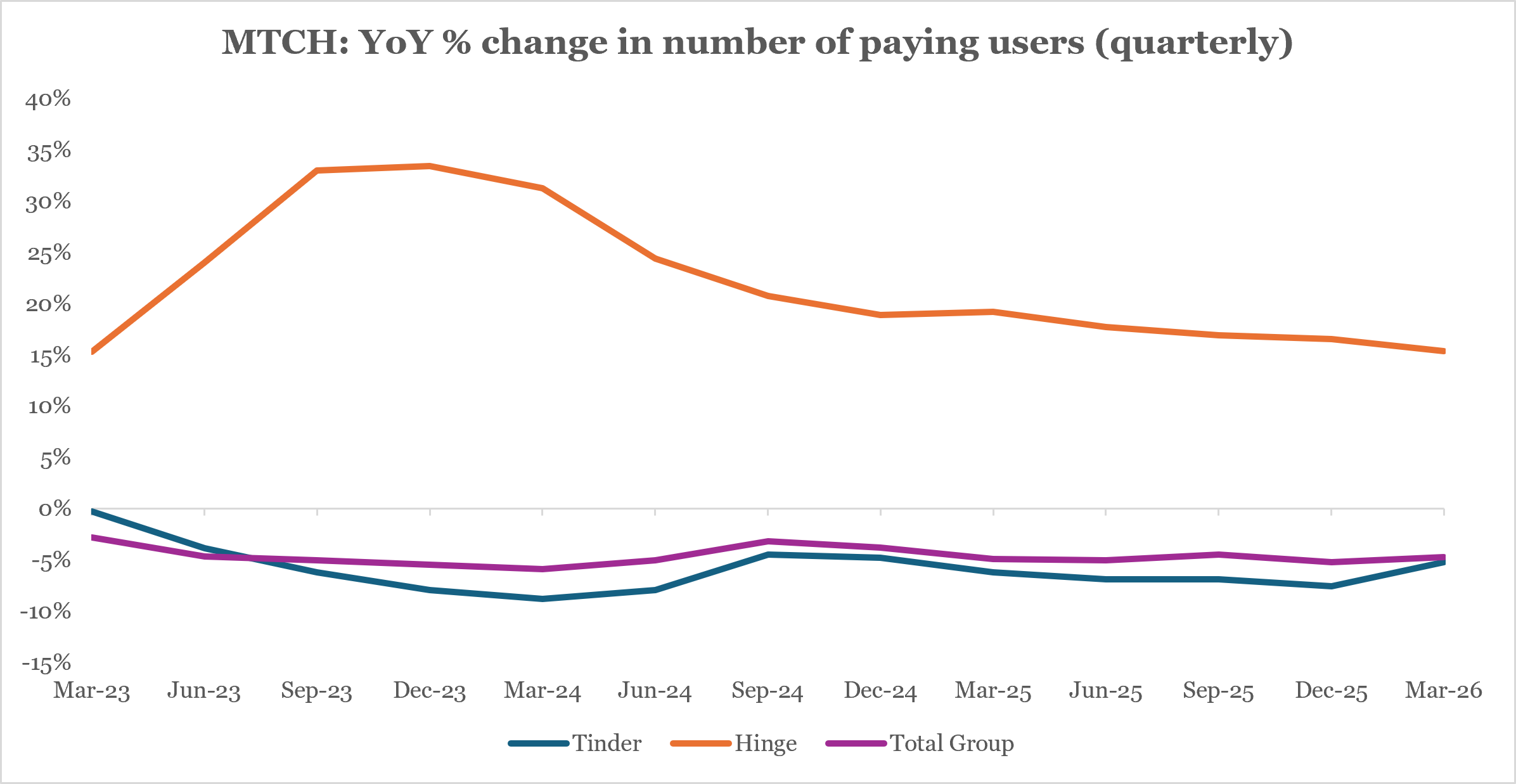

Tinder is also losing paying users.

Source: MTCH, Angsana Anderson estimates

However, Tinder’s user decline is partially offset by the rapid growth of Hinge.

MTCH fully acquired Hinge in 2018 to target singles looking for serious relationships. In 2018, Hinge was immaterial. By 2025, it is contributing ~20% to MTCH’s total revenue.

Therein lies BMBL’s problem.

No new products. BMBL gets ~80% of its revenue from its Bumble app, and the remaining 20% from Badoo. BMBL launched them in 2014 and 2006 respectively. Since then, BMBL has not released new major apps.

Given their short lifecycle, BMBL should be launching new apps.

Likely to continue losing users. The bulls argue that paying users will recover. Founder Whitney Wolfe Herd has returned as CEO in Mar 2025. BMBL is cutting performance marketing and purging bots and bad users. Eventually the user experience will recover and BMBL returns to growth.

Sadly, history is not on their side. I could not find meaningful precedents for a successful turnaround of such scale.

Revenue growth in 2026 likely below expectation. Consensus sell-side estimate is calling for -13% revenue decline in 2026.

I believe this is too optimistic.

In Q1’26, revenue declined -14%. Advance payments from customers (deferred revenue) declined -15% YoY, suggesting a steeper revenue decline in the short term.

Long-term growth likely below expectation. The bulls argue BMBL will eventually return to growth. Consensus estimates show revenue returning to +2% growth in 2028.

Compared to BMBL’s own estimates, this seems too optimistic.

BMBL tested goodwill for impairment in Q4’25. Most goodwill pertains to the Bumble and Badoo apps. To quantify the goodwill impairment, management is required to estimate BMBL’s terminal growth rate.

What was the terminal growth rate BMBL used?

0%.

Other matters

Largest shareholder likely wants out. On 26 Jun 2026, Reuters reported BMBL is exploring a sale.2 Blackstone is the single largest shareholder, with ~17% of the shares outstanding.

Given that Blackstone made its initial acquisition in Jan 2020, they have now held the asset for just over six and a half years. This puts them at the tail end of a traditional private equity holding period, which typically spans 3 to 7 years.

In Nov 2025, Blackstone and founder Whitney cleaned up BMBL’s balance sheet by relinquishing all their future rights to the Tax Receivable Agreement (TRA) in return for a significantly smaller cash payment upfront.

Without going too much into the technicalities, the TRA is essentially a debt that BMBL has to repay to Blackstone and Whitney when it starts earning taxable profits.

Blackstone and Whitney also converted their Common Units into tradeable common shares. Blackstone has been selling down its shares, with the latest sale happening on 29 Jun 2026.

These actions are consistent with preparations for a full exit from their remaining holdings.

But will they get the price they desire? I don’t see many buyers.

MTCH would probably trigger antitrust issues, given that they overlap significantly in the US.

MOMO, fresh off acquiring happn in 20253, will likely face an uphill battle to convince the Committee on Foreign Investment in the United States (CFIUS).

A consortium led by STORY3 Capital Partners, an alternative asset manager, is probably a front-runner to acquire BMBL.

STORY3 already has strong knowledge of BMBL. It was one of the lenders to BMBL’s refinancing round in Mar 2026. Furthermore, STORY3 is a specialist PE firm that explicitly targets consumer brands, commerce, and digital media.

The buyers will likely drive a hard bargain.

Factors that could lead to a re-assessment of my decision

Number of paying users stabilizes.

BMBL releases new products, and they are gaining traction.

Inflection in advance payments from customers.

Coming up next

I will show you how to inflate revenue.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in BMBL, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.