[Update] MoneyMax Financial Services Ltd. (5WJ; MMFS SP)

2025 H2 results announcement. Maintain decision to pass because (a) earnings have more downside than upside; (b) market seems to be reaching saturation...

Disclaimer: This is a record of my investment decisions, not financial advice. I may change my decisions without notice. Use this only for education and entertainment. Do not rely on this for your investment decisions. All analysis and opinions expressed are solely my own, and 5WJ has not reviewed, approved, or endorsed this post.

About

Share price: SGD 0.76

Market capitalisation: SGD 672 mn (USD 525 mn)

Enterprise value (EV): SGD 1,546 mn (USD 1,208 mn)

Average daily volume (ADV): SGD 1.0 mn (USD 0.8 mn)

LTM P/E: 9x; LTM P/B: 3x

My decision

Pass

Background

In 2013, gold price fell -16%. Albemarle & Bond, the UK’s then second largest pawnbroker, resorted to melting gold jewellery to stave off bankruptcy.

Times have changed. MoneyMax Financial Services Ltd. (5WJ; MMFS SP), Singapore’s largest pawnbroker, reported +94% YoY growth in 2025 H2 earnings. Business is booming.

After the results, I revisited 5WJ and decided to stick with my original decision to pass.

In addition to the points from my first take, I am concerned that earnings now have more downside than upside. In this Substack post, I discuss why I believe if gold price simply stops growing, 5WJ’s earnings will decline significantly.

During the 2013 gold crash, 5WJ looked resilient on the surface, with headline earnings still growing low single digits.

But that was largely driven by opening more stores. On a per‑store basis, revenue and profit collapsed. With outlet density now near historical highs, I doubt 5WJ can repeat that playbook.

Business model

Breakdown of 2025 revenue (SGD 542 mn; +39% YoY):

78% retail and trading of gold and luxury items (+43% YoY)

18% pawnbroking (+46% YoY)

4% secured lending (-15% YoY)

Revenue from pawnbroking is earned from the provision of financing solutions secured by pledged collateral such as gold, jewellery and luxury timepieces.

Revenue from retail and trading of gold and luxury items is earned from the sale of brand‑new gold jewellery, pre‑owned jewellery, luxury timepieces and branded bags, including wholesale trading of gold.

Revenue from secured lending is earned from collateralised loans to individuals and businesses, including automotive and property financing and lease receivables.

In 2025, 5WJ earns 85% of its revenue in Singapore with 51 outlets. The remaining 15% is earned from Malaysia with 62 outlets.

The group serves:

Retail pawnshop customers who pledge gold, jewellery, luxury watches and bags for short‑term financing.

Retail customers who sell their gold and jewellery to MoneyMax.

Retail shoppers buying new and pre‑owned jewellery and luxury items, both in-store and online.

Borrowers (individuals and SMEs) using secured lending for automotive and property financing.

In 2024, the top customer accounted for ~34% of revenue. This major customer is from wholesale trading of gold and luxury items segment.

Breakdown of 2025 net profit after tax (NPAT) (SGD 76 mn; +83% YoY):

54% retail and trading of gold and luxury items (+107% YoY, 10% NPAT margin)

44% pawnbroking (+88% YoY, 34% NPM)

8% secured lending (-33% YoY, 24% NPM)

25% others (+84% YoY)

-30% consolidation elimination (likely offset against ‘others’)

The most relevant public comparables are its two competitors in Singapore: ValueMax Group Limited (T6I; VMAX SP) and Aspial Lifestyle Limited (5UF; ASPL SP).

5WJ holds ~ 21% market share by number of outlets in Singapore, up from 16% in 2016. In Malaysia, 5WJ holds ~6% market share, up from 3% in 2016.

My reasons

Earnings have more downside than upside. The bulls see 5WJ as a bargain. In the last 3 years, it has grown its net profit after tax (NPAT) by 48% p.a. yet it is still only trading at LTM P/E of 9x.

The segment that contributed the most to the NPAT growth is retail and trading of gold and luxury items (‘retail and trading’).

Over the past 3 years, this segment grew 64% p.a., much faster than the 47% p.a. growth in group NPAT. Retail and trading is now 5WJ’s largest segment, contributing to 54% of group NPAT.

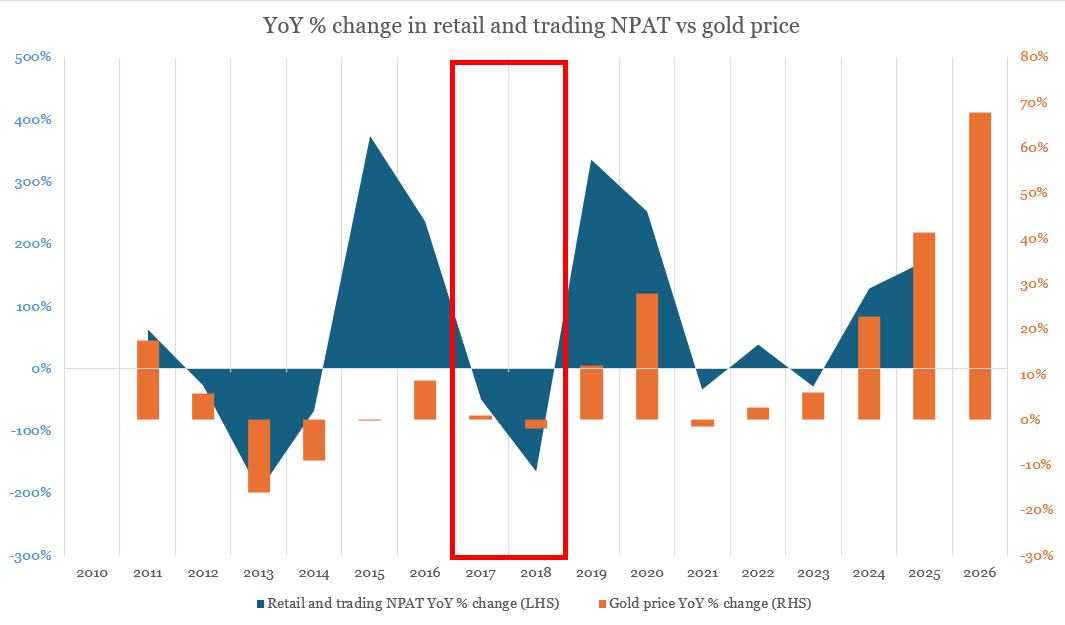

What drove the growth in retail and trading? The short answer: movements in gold price.

Source: 5WJ annual reports (retail and trading NPAT); Investing.com (gold price)

From the chart above, it’s obvious that when gold price rises, NPAT at retail and trading increases more than proportionately and vice versa.

When gold price rises, sales volume increases. People strapped for cash have more incentive to sell their gold jewellery. Aunties and uncles dig out long forgotten and unwanted gold jewellery from their closets to sell.

However, what’s not so obvious is that, when gold price is generally flat, NPAT from retail and trading decreases.

In 2017 and 2018, gold price was flat, but NPAT from retail and trading declined -50% and -165% YoY respectively. Why?

The short answer: time lag between the point when a pawnbroker buys gold from retail customers and the point when the pawnbroker sells it for scrap.

When a customer sells their gold to a pawnbroker, the pawnbroker typically holds the gold in inventory for processing until it is sold to its wholesale customer.

If gold price increases during this period, the pawnbroker enjoys a larger spread. If gold price is flat during this period, the pawnbroker will make a much smaller spread.

Gold price grew 23% and 41% in 2024 and 2025 respectively. Yet NPAT from retail and trading grew 129% in 2024 and 171% in 2025.

Besides higher sales volume, I believe the time lag is a strong contributor to the huge growth.

In the first two months of 2026, gold price increased 68% YoY. Retail and trading NPAT should continue to grow in Q1’26.

After rising +23% in 2024 and another +41% in 2025, how long can the gold price continue its meteoric rise? 1 year?

With the conflict in the Middle East, maybe yes. 2 years? 3 years?

Remember, if gold price simply stops growing, NPAT from retail and trading will likely decline significantly.

With earnings facing more downside than upside, I believe 5WJ is not an obvious bargain at LTM P/E of 11x.

Market likely reaching saturation. At first glance, 5WJ seems resilient to falls in gold price. In 2013 and 2014, gold price fell -16% and -9% respectively. 5WJ’s revenue fell only -13% in 2013 and grew 11% in 2014. NPAT grew +3% and +1%.

However, that’s because 5WJ added more outlets.

Number of outlets increased +23% in 2013 and +47% in 2014. On a per-outlet basis, revenue declined -30% and -24% in 2013 and 2014. Because of operating leverage, NPAT per outlet performed worse: -75% in 2013 and -70% in 2014.

If gold prices fall, can 5WJ add more stores to offset the fall in demand, just like in 2013 and 2014? I believe the answer is no because the markets are reaching saturation.

5WJ earns ~85% of its revenue from Singapore. Before the gold price crash in 2013, outlet density in Singapore was still not high.

The number of outlets per 1 mn people is only between 34 and 36. This allowed 5WJ to add more outlets when the gold price fell in 2013 and 2014.

By 2014, outlet density reached 42 outlets per 1 mn people and has plateaued around that level ever since.

Malaysia contributed only 15% of revenue in 2025, and is not big enough to offset any severe declines in Singapore.

Moreover, after stagnating between 15 to 20 outlets per 1 mn people during 2014-2020, outlet density increased rapidly in the past few years and reached an all-time high of ~27 in 2024.

This raises the question of whether the Malaysian market has added too many stores on the back of the gold rally in recent years, and how sustainable this can be.

Financial risk looks high. As of 2025, 5WJ carries a loan book of SGD 1,012 mn. This is funded by short-term borrowings of SGD 650 mn and long-term borrowings of SGD 219 mn. The remaining SGD 143 mn is funded by equity.

Just 14% of 5WJ’s loan book needs to default for its equity in its loan book to turn negative. From my experience with Ramsdens, the UK’s second largest pawnbroker, the % of a pawn loan book in default is usually ~25%.

5WJ is effectively a bank. It borrows from banks and lends to sub-prime borrowers on gold collateral.

But 5WJ’s financial risk is higher. 5WJ relies on bank loans for funding. Such wholesale funding is more ‘flightly’ and tends to disappear precisely when the borrower comes under stress.

You could argue that 5WJ’s financial risk is not as elevated as headline leverage suggests.

Although its SGD 650 mn of short-term borrowings is about 5x operating profit and looks high, this is partly offset by the fact that the current portion of its loan book stands at SGD 842 mn. Pawn loans are typically short-tenor (around six months) and collateralised.

However, if gold prices crash, the value of gold collateral can drop below the outstanding loan amount.

This increases the incentive for borrowers to default and forfeit their collateral. 5WJ may be forced to liquidate pledged gold at discounts to preserve capital and meet its own debt obligations.

In 2013, the UK pawnbroker Albemarle & Bond resorted to melting down gold jewellery to raise cash and avoid breaching covenants1. The pawnbroker eventually went into administration anyway.

Difficulty in assessing the quality of the loan book. You could argue that 5WJ’s financial risk is mitigated by the fact that the loans are collateralised.

However, management does not disclose its loan-to-value ratio (LTV ratio). There is also the risk that if gold price declines significantly, whatever LTV ratio that appears prudent now may not actually be sufficient.

In 2024, 5WJ’s allowance for impairment is only SGD 2.2 mn against a gross loan book of SGD 755 mn. This is 0.3%. The same % for Ramsdens is 7%.

At first glance, it seems like 5WJ may not have sufficiently provisioned against loan impairments. However, there may be good reasons why this % should be lower at 5WJ.

But because management does not disclose key metrics like % of the loan book in default, aging of loan book, LTV ratios, it is hard for me to assess whether 5WJ has sufficiently provided for loan impairments.

Capital intensive. Between 2016 and 2025, NPAT increased 12x but dividends only increased 4x. This is because the profits had to be reinvested into the loan book for growth. In fact, free cash flow to firm has been negative since 2017.

Whereas banks can rely on low-cost stable retail deposits to fund their growth, 5WJ has no such privilege.

5WJ has to reinvest all its profits and rely on bank loans to grow. This makes each dollar of earnings from 5WJ less valuable than the big 3 banks.

Because of this, I am not sure whether 5WJ (LTM P/E: 11x) can trade at the same LTM P/E multiple as DBS (15x), UOB (13x) and OCBC (13x).

On LTM P/B basis, 5WJ (LTM P/B: 3x) is already trading higher than DBS (2x), UOB (1x) and OCBC (2x). How sustainable is this?

Factors that could lead to a change in my decision

Diversification of earnings away from the current heavy exposure to gold price.

Strong evidence that the market remains underpenetrated in Malaysia and 5WJ is in strong position to capture the growth.

Reduction of financial risk by shifting short-term loans to long-term loans with friendly or no covenants.

Management disclosing key metrics on their loan book (e.g. LTV ratio, aging of loan book, % of loans in default) and the key metrics are healthy.

The business becomes less capital intensive (e.g. 5WJ securitising pawn receivables).

Share price falls to SGD 0.64 (~30% below my estimate of intrinsic value) without significant deterioration in business fundamentals.

If you want more analysis like this, subscribe to my Substack