[Update] HRnetGroup Limited (CHZ; HRNET SP)

“We had to handle cases where people passed away on the job. HR is not as easy as people think.”

Disclaimer: This is a record of my investment decisions, not financial advice. I may change my decisions without notice. Use this only for education and entertainment. Do not rely on this for your investment decisions. I own shares in CHZ.

Background

Following my shortlist of HRnetGroup Limited (CHZ; HRNET SP), I met Jennifer Kang at CHZ’s headquarters in Singapore. Jennifer joined CHZ in 2003 and became Group CFO in 2022.

We discussed a wide range of topics. How is generative AI impacting the labour market? Why is CHZ’s net profit growing while global peers are struggling? What are CHZ’s plans for its cash pile (~44% of market capitalisation)?

In this Substack post, I summarise the main takeaways from our conversation. I would like to thank Jennifer for her time. She has reviewed this post for factual accuracy. I retained full editorial independence.

In a future post, I will publish my complete thesis and valuation model of CHZ. To receive these updates, subscribe to my Substack:

Business model

Flexible staffing (FS)

Clients choose CHZ over competitors because of CHZ’s proven track record in providing this service. Furthermore, this is a capital-intensive business. CHZ pays its contractors first and bills the contractors’ payroll to clients with a markup. Clients typically pay in ~60 days, some even longer. Not many companies have the balance sheet to fund this working capital requirement. CHZ’s position as the largest recruitment agency in Singapore gives it an advantage. CHZ keeps ~3 months of payroll in cash.

Some smaller competitors try to compete by offering lower markups in exchange for upfront cash payments from their clients. Even so, large customers still tend to stick with proven providers like CHZ.

CHZ hires ‘back-to-back’ and does not keep contractors in inventory. This is the standard practice around the world, except in Japan. Because of the tight labour market in Japan, recruitment agencies tend to keep contractors in inventory. Their focus will be on utilisation rate. However, this model can only work in Japan because of their tight labour market.

Since 2015, number of contractors at CHZ grew ~5% p.a while the number of professional recruitment placements shrunk. Many years ago, contract work was considered inferior. Over time, especially after COVID-19, the mindset of jobseekers has changed. The current generation of workers prioritise work-life balance and don’t mind working as contractors. On the demand side, companies also increasingly prefer to hire flexible staff and only convert them when things become more certain. This trend will likely continue in the foreseeable future.

Gross profit (GP) per contractor is flat or declining slightly. Singapore makes up ~52% of gross profit. Growth in Singapore is limited because it is a mature market.

To drive the next phase of growth, CHZ is prioritising international markets, particularly Taiwan and Indonesia, where the addressable market is larger and volume growth potential is strong. While margins in these markets are structurally lower than in Singapore, the strategy is to build scale and market share first. As the platform matures and client relationships deepen, pricing and profitability can be progressively optimised over time.

Over the long term, gross profit margins in international markets are expected to improve. When CHZ enters a new market, it typically begins with sectors that have lower barriers to entry, allowing it to build scale, establish a track record, and earn client trust. As relationships deepen and operational credibility is established, CHZ progressively expands into higher-value staffing segments with stronger pricing. This progression is already evident in markets such as Taiwan.

The largest contributors to gross profit, in descending order, are Singapore, Taiwan and Mainland China.

Professional Recruitment (PR)

To understand why clients choose CHZ over competitors, we need to look at how CHZ started. CHZ started around 1992 as a retained search agency. Korn Ferry (KFY; KFY US) and Heidrick & Struggles are examples of global retained search agencies. In this model, the agency charges fees in stages over the timeline of the project.

This model is less common now because of various factors including online job channels like Jobstreet and LinkedIn that have disrupted the market. CHZ shifted into success-based recruitment and achieved higher market share. Today, most of CHZ’s recruitment is success-based. Typical success-based recruitment is a transactional approach focused on headcount fulfilment. It starts with a Job Description from HR listing the role requirements. The tool used is a standard CV for client review.

Because of CHZ’s roots in retained search work, it has its differentiating consulting-led recruitment methodology that works through a rigorous process with the hiring manager to understand the immediate challenges, the company’s unique selling point (USP), and the role’s unique requirements. The tool used is a Candidate Profile Report that emphasizes achievements and fit based on CHZ’s expert opinion.

Furthermore, CHZ’s brands are now widely recognised. This is a function of CHZ’s long track record and public listing. Clients have the incentive to use the brand that is widely recognised. If a client uses a no-name recruitment agency and the new hire turns out to be bad, the client will be blamed. If you’re the HR on the client’s side, why risk your career?

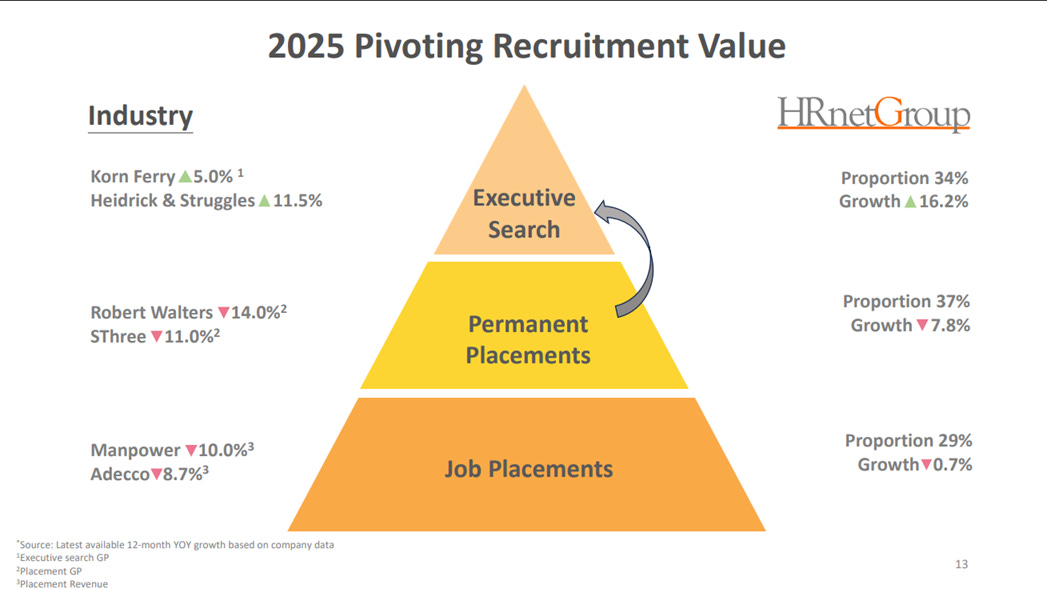

Within the PR segment, CHZ is pivoting towards executive search. This segment focuses on senior leadership roles and is growing.

Industry trends

The middle of the pyramid is currently being squeezed. This involves junior level white collar work with tasks such as data analysis that is vulnerable to disruption by generative artificial intelligence. Even CHZ themselves are trialling generative AI to automate billing tasks by analysing offer letters and service contracts, etc.

The bottom of the pyramid is also affected, but not as much because automation and digitalisation are still difficult to achieve in these roles. For example, roles in retail, logistics, etc.

Source: 2025 CHZ Presentation (PS)

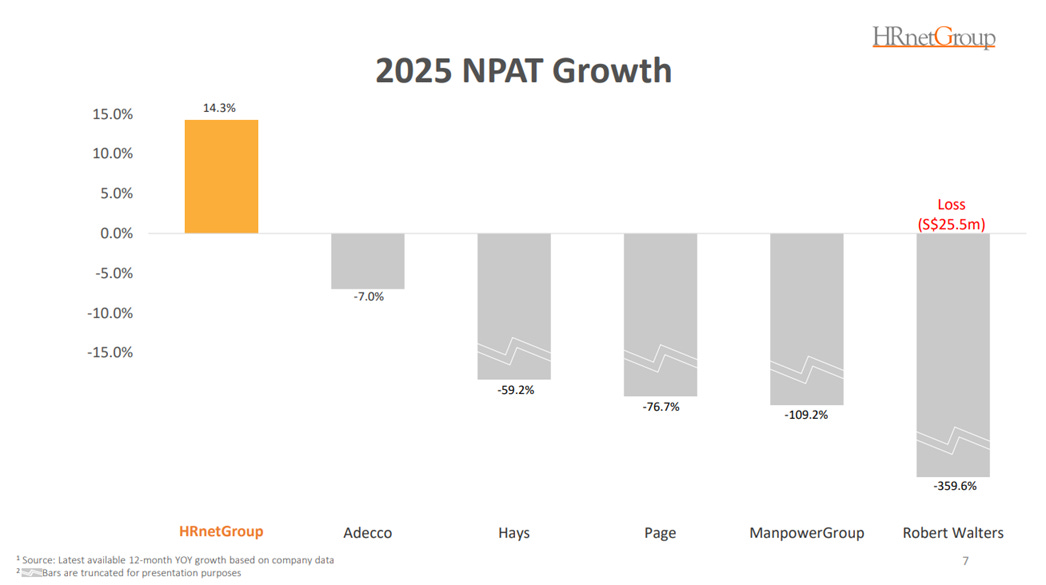

In 2025, CHZ’s net profit after tax (NPAT) growth outperformed many global peers, especially those in the West. This is a function of the economic environment in different markets. The economic environment in markets like the UK and EU is still difficult. NPAT is a function of both revenue and cost. Even though some of these recruitment agencies have international operations, their weak NPAT performance may be attributable to sub-optimal cost structure too. On the other hand, recruitment agencies in Japan generally perform better because of the tight labour market in Japan.

Source: 2025 CHZ PS

Capital allocation

Investment in Staffline Group PLC (STAF; STAF LN)

This was an opportunistic purchase. STAF’s share price collapsed because of a payroll incident. In the UK, contractors must be paid for the time they take to change into and out of uniforms. However, neither STAF, the customers nor the contractors tracked this because they were not aware of this rule. A whistleblower complained. With that, STAF’s accounts had to be delayed, triggering the share price collapse. CHZ’s investment came after the collapse.

CHZ started with a small investment in STAF. Then Brexit happened. The adverse impact was bigger than expected. Soon after that, COVID-19 struck. Under STAF’s previous CEO, STAF made ~8 acquisitions. All of these had to be impaired.

Ultimately, STAF was not material to CHZ. It was not a transformative acquisition. It was simply an effort to access blue-collar staffing market in the UK. It did not divert significant management attention away from CHZ’s core business.

CHZ accounted its investment in STAF at fair value through other comprehensive income (FVOCI). CHZ does not have a board seat on STAF. In any case, it was not in CHZ’s advantage to account for STAF as an associate since it was making losses for a number of years.

CHZ owns 29.95% of STAF. This % fell to as low as ~15% at one point as STAF issued more shares as part of its recapitalisation. The % rose to ~20% because STAF started share buybacks. Recently, CHZ has started paring down its stake.

Various investments

CHZ’s quoted equity securities carried at FVOCI (2025: SGD 19 mn ) consist of investments in STAF and Bamboos Health Care Holdings Limited (2293; 2293 HK).

CHZ’s quoted equity securities carried at fair value through profit and loss (FVTPL) (2025: SGD 10 mn) consist of investments in publicly listed HR companies, including some based in Japan. The purpose of becoming shareholders is to deepen knowledge of the industry around the world and to get to know other players.

CHZ holds some gold certificates, although the amount is not material. The purpose is to have a diversified pool of instruments for liquidity (e.g. cash, bonds, gold).

CHZ has ~ SGD 2 mn of unquoted equity securities carried at FVTPL in 2024. These are venture capital investments in a HR-related company. CHZ has already recouped its initial investment cost.

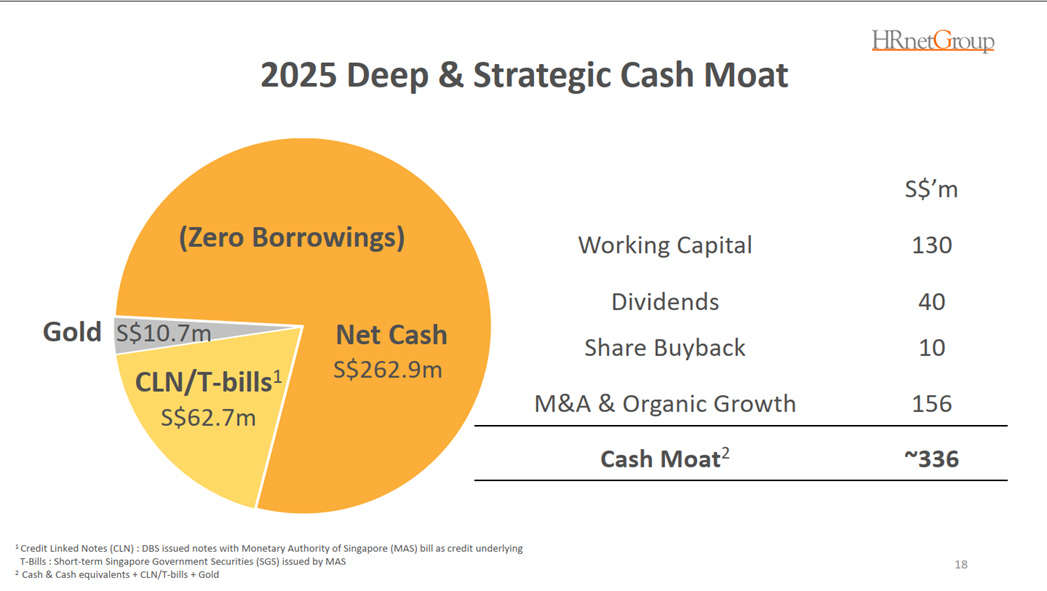

Cash pile

Out of the SGD 336 mn cash moat, SGD 156 mn is earmarked for M&A and organic growth. CHZ hopes to execute a sizeable M&A deal. For example, a business generating SGD 31 mn of NPAT, acquired at 10x P/E for a 51% stake — would imply a consideration of about SGD 156 mn. This is well within CHZ’s financial capacity, while retaining the optionality to take on debt if it enhances returns or accelerates growth.

Source: 2025 CHZ PS

Citing UOB’s acquisition of Citibank’s consumer business in 2022, Jennifer said what’s important is to be patient and have significant dry powder ready. Good opportunities are rare and fleeting. Financing from bankers can be fickle, and with little notice they can demand that CHZ put up more equity. When a good opportunity appears, scrambling for financing signals desperation. That’s not good for the acquisition price. That’s why CHZ keeps a significant portion of its cash on standby for M&A.

Closing

When asked what investors misunderstand the most about CHZ, Jennifer said this is a people business. Outsiders often think recruitment is easy, just matchmaking between employers and jobseekers. However, it is much more complex. A lot of things can go wrong during the process. For example, a candidate reached the final recruitment stage but decided to back out after their family voiced concerns about working overseas. CHZ had to address their concerns to salvage the deal. That’s just one example.

Barriers to entry are high in the FS segment because of the significant working capital requirements. You must pay your contractors first before you bill your clients. Clients typically pay in ~60 days, some even longer. Few companies are large enough, like CHZ, to fund this working capital requirement.

Barriers to entry are low in the PR segment. It’s easy for a person to register as an employment agency (EA) with the MOM. As long as you are disciplined, you stand a good chance of making good money. But the problem is, how do you scale up from a one-man show? It’s difficult to scale up and build an army of disciplined salespeople with a repeatable process that works. That’s what CHZ has achieved.

Subscribe to my Substack for more updates like this