[Update] HRnetGroup Limited (CHZ; HRNET SP)

2025 H2 results announcement and earnings call. Thesis remains on track

About

Share price: SGD 0.75

Market capitalisation: SGD 737 mn (USD 583 mn)

Enterprise value (EV): SGD 439 mn (USD 347 mn)

Average daily volume (ADV): SGD 100 k (USD 80 k)

NTM P/E: 16x

My decision

Continue holding my shares

Background

Following my shortlist of HRnetGroup Limited (CHZ; HRNET SP), I completed my thesis and bought shares in CHZ.

On Wed 25 Feb 2026, CHZ released 2025 H2 results after the market closed. On Thu 26 Feb 2026 at 10.30am SGT, CHZ hosted an online earnings call.

In this Substack post, I will evaluate whether my thesis remains on track. I will also share my key takeaways from the earnings call.

In a future post, I will publish my complete thesis and valuation model for CHZ. To receive these updates, click on the link below and subscribe to my Substack.

My reasons

Thesis looks on track.

Good business, temporary headwinds. I see a higher probability that CHZ is approaching an inflection point. In H2’25, gross profit grew 4.2% YoY. This is the first time gross profit grew since it started declining in H2’22. Other payables and accruals, which include contract liabilities, increased 3%.

In the first 8 weeks of 2026, CHZ already has visibility on the pipeline for H1’26, and the pipeline quality has improved compared to last year. The market in Singapore is stable. Growth potential is concentrated in Taiwan and core ASEAN markets like Malaysia and Indonesia. Recovery in mainland China is still patchy. Hong Kong and Japan remain weak. Vietnam is still small because it has only been in operation for 2 quarters, but performance has been promising.

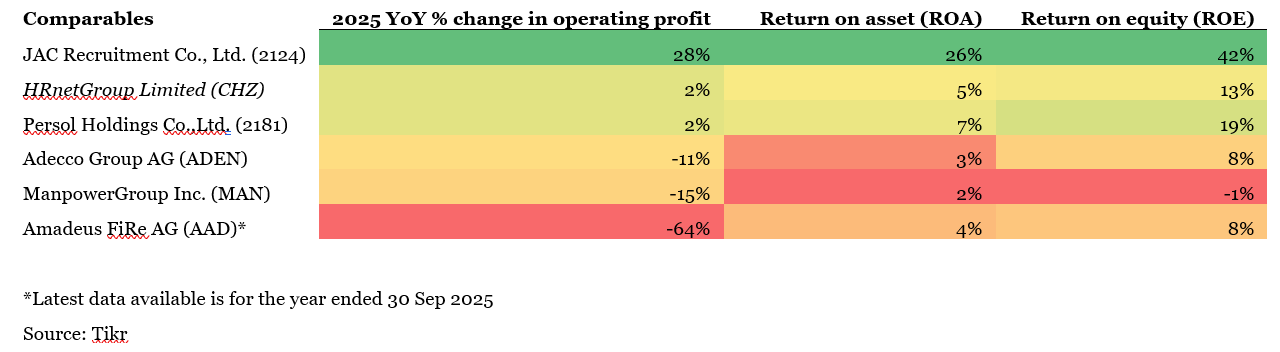

CHZ continues to display characteristics of a good business. It achieved a good return on equity (ROE), even with significant net cash (~46% of market capitalisation). It improved its ROE from 12% in 2024 to 13% in 2025.

Among the group of comparables that I track, CHZ performed among the best in 2025.

However, the market has not recognised that CHZ is a good business, that its headwinds are temporary and an inflection point is near. CHZ currently trades at ~10% free cash flow to firm (FCFF) yield on enterprise value (EV), based on my estimate of sustainable FCFF. This is a very attractive ~8% premium over Singapore’s 10y government bond.

Capital returns. CHZ increased its final dividend by 3%. The full year dividend reached 4.2 cents, up 5% from 4.0 cents last year. Dividend payout ratio increased to 78%, above than its historical range of 50% to 60%. At a share price of SGD 0.745, this implies a dividend yield of 5.6%.

As in H1’25, CHZ has earmarked about SGD 10 mn for share buybacks, equivalent to roughly 1.4% of its market capitalisation. Management intends to deploy this opportunistically when the share price trades below their assessment of fair value. I suspect this pool will be drawn down mainly during periods of market stress when trading liquidity is higher. The shares’ normal average daily trading value is only ~ SGD 0.1 mn, which constrains execution capacity. Bear in mind that SGX considers buyback activity to be excessive when it exceeds 30% of daily volume1.

Management sees dividends of 4 cents per share as strong and sustainable. They also indicated that when the business performs well and value is unlocked from its investments, they intend to share more with shareholders, as they have done this time. Unlike many peers that pay lip service to capital returns, CHZ has backed words with action through higher dividends. This suggests to me a good probability of higher capital returns in the future. Yet, the market seems to under-recognise this. CHZ is trading at a dividend yield of 5.6%, an attractive ~3.6% premium over Singapore 10y government bond.

Earnings call

The following are my notes from the earnings call. Although I do my best to note down the key points, this is not intended to be a complete or fully accurate transcript of the call. CHZ has not reviewed nor approved this.

Participants:

1. Adeline Sim (Chief Corporate Officer)

2. Jennifer Kang (Group CFO)

3. Fadzlin Rashid (Director of Marketing & Corporate Communications)

4. Various shareholders and analysts (though the Q&A session seems dominated by private shareholders)

Company overview

HRnet Group operates two core business segments: Professional Recruitment (headhunting/executive search) (PR) and Flexible Staffing (contract workforce deployment) (FS). In 2025, the group placed 4,766 talents and supported an average of 16,421 contractors per month across Asia. Although Singapore remains the largest market (52% of gross profit), other markets like Taiwan have grown strongly, continuing geographic diversification. Gross profit contribution from North Asia increased from 41% in 2024 to 43% in 2025. The business is diversified across IT & Tech (24% of revenue), Financial & Insurance (21%), Healthcare (14%), and Retail & Consumer (14%).

Performance in 2025

Revenue grew 3% to SGD 584 mn. Net profit after tax (NPAT) rose 14.3% to ~ SGD 53 mn, aided by SGD 7 mn increase in other income (mainly from fair value gains on investments) and tight cost control. Gross profit was stable at SGD 123 mn. Professional recruitment gross profit increased for the first time since 2021, driven by stronger senior executive search activity. The group achieved a 43% GP-to-NPAT conversion ratio, underpinned by a co-ownership model that instils cost discipline among business leaders.

Over 33 years, HRnet has navigated the AFC, dot-com crash, SARS, GFC, and COVID-19, with smoother revenue cycles and faster profit recovery than global recruitment peers. In 2025, HRnet’s 14% net profit growth contrasted with sharp declines or losses at most peers. Flexible staffing provides a recurring revenue base that covers ~1,000 internal headcount costs, giving operating stability in uncertain markets.

I asked management to share more details on what drove the difference in regional performance. PR gross profit improved in North Asia and Rest of Asia, but not Singapore. Management shared that growth is very strong in Taiwan. The story is similar in other ASEAN countries like Indonesia, where CHZ is seeing strong wage growth and strong demand. Although GDP numbers are good in Singapore, it has not translated as much into strong job growth. It has been a while now that the middle tier (permanent placements) has remained sluggish. But management remains hopeful that Singapore will improve soon.

Dividends and capital allocation

CHZ declared a final dividend of 2.2 cents per share, bringing the full-year payout to 4.2 cents per share. This represents ~78% of profits and ~79% of free cash flow. At the recent share price of SGD 0.745, the dividend yield is ~5.6%.

The balance sheet carries zero borrowings, with a cash pile earmarked for the following purposes: SGD 130 mn working capital, SGD 40 mn dividends, SGD 10 mn share buybacks, and SGD 156 mn for M&A and organic growth.

2026 business focus

Adeline Sim, Chief Corporate Officer shared 3 points.

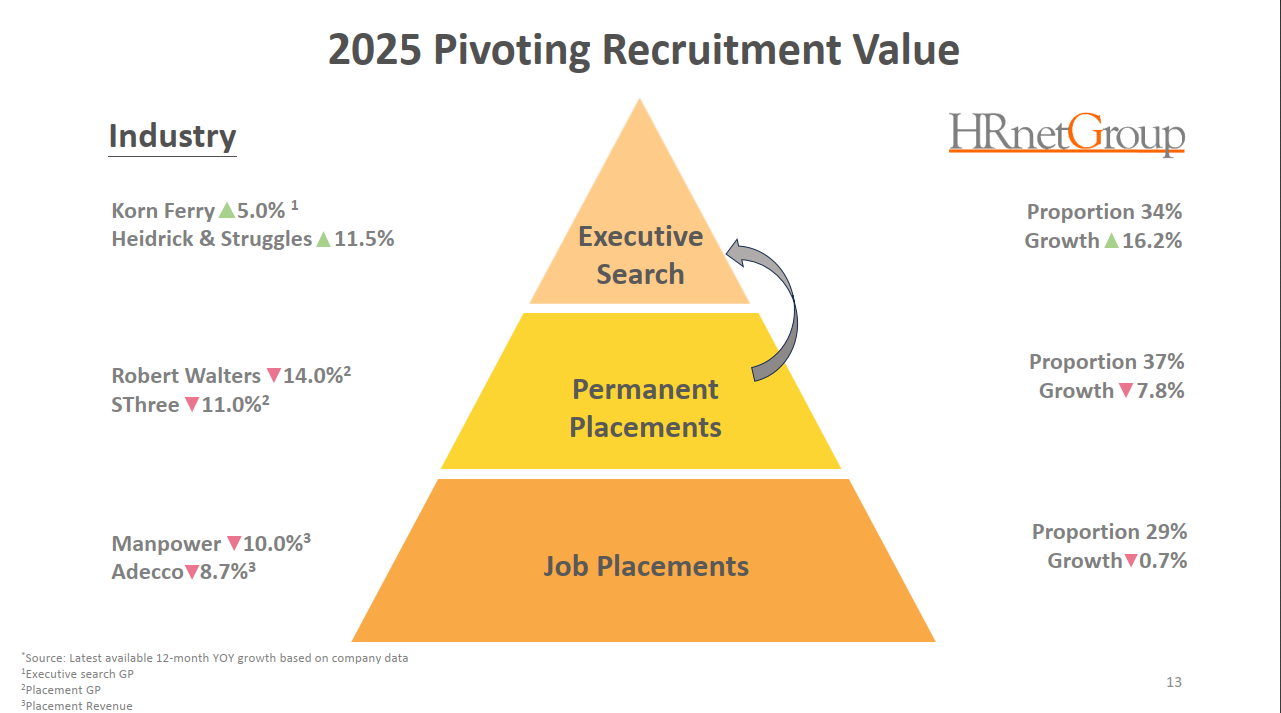

First, pivoting PR towards executive search because permanent placements remain stagnant. CHZ plans to continue offering competitive pricing at high quality service level to gain share.

At the same time, expand the flexible staffing offering across cities in Indonesia, Taiwan, etc.

Finally, continue to cultivate recurring revenue streams like flexible staffing and workforce management app, Octomate.

On the topic of pivoting PR towards executive search, I asked if competition within permanent placement remains intense, how much more can executive search offset? 37% of gross profit is attributable to permanent placement while 34% is attributable to executive search. Management explained the difference between permanent placement and executive search and how they are pivoting to executive search. However, they stopped short of giving an estimate on how much more can executive search offset.

Source: 2025 CHZ Presentation

2026 outlook

In the first 8 weeks of 2026, management sees pipeline quality is improving. Taiwan and Malaysia show strong expansion, Indonesia continues to grow, and Vietnam is in early stages. China’s recovery remains patchy while Hong Kong and Japan remain weak.

Miscellaneous

Singapore Equity Market Development Programme (EQDP): I asked how CHZ plans to benefit from Singapore EQDP. A lot of small and mid-cap companies in Singapore have benefited from Singapore EQDP, but it looks like the benefits have not flowed to CHZ yet. Management replied that they have reached out to almost all the fund managers that have received allocation from the Singapore EQDP. Furthermore, in Oct 2025, they made a placement of shares to 5 investors. Among these 5, there were 2 fund managers (Lion Global and Avanda) that received EQDP allocation.

Government grants: I asked how CHZ sees the risks of government reducing grants? This risk is not immaterial, given that government grants reached 7.5% of CHZ’s 2025 gross profit in 2025. What mitigating actions are available? Management explained that government grant is a matter of government policy. Management shared the following chart from IRAS showing the Progressive Wage Credit Scheme (PWCS), one of the government grants CHZ receives.

Source: IRAS (2026)

This chart shows the chronology of how the PWCS co-funding support has worked in the past. The trend is that when economic times are challenging, the government will come up with higher grants and subsidies to help companies continue employing many people. The co-funding support for 2026 actually increased from 20% to 30%. In Budget 2026, the government announced 30% for 2027 and 20% for 2028. CHZ will work with this.

In a future post, I will publish my complete thesis and valuation model for CHZ. To receive these updates, subscribe to my Substack.