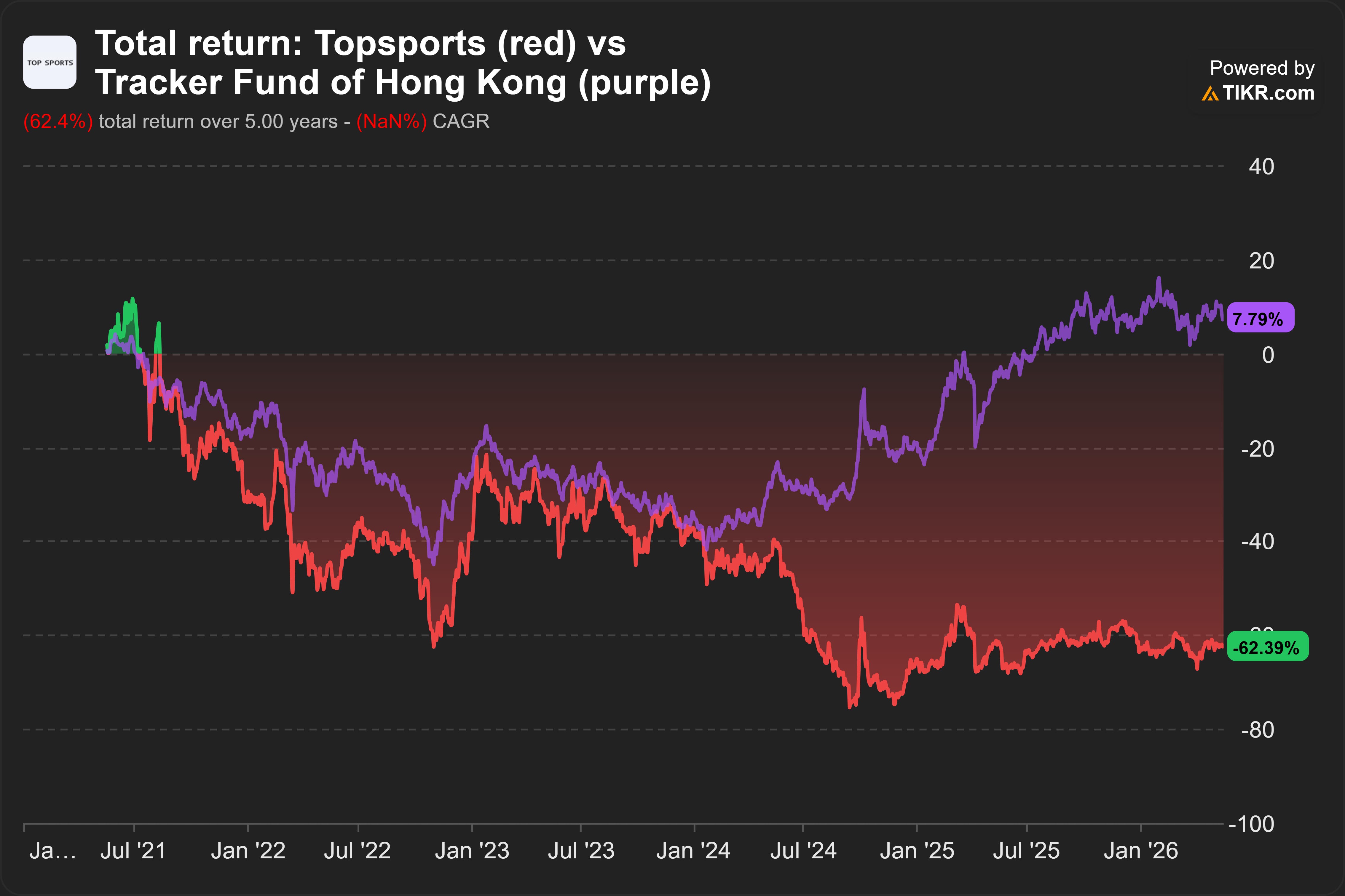

Topsports: 10% dividend yield. But I decided to pass. Why?

[First Take] Topsports International Holdings Limited (6110 HK)

Summary

I decided to pass because Topsports’ competitive advantage is deteriorating. Consumer preference is shifting towards competitors’ brands, and it is difficult to tell how far this trend can run.

Corporate governance can be improved.

Most importantly, I believe the high dividend yield is not sustainable.

About (19 May 2026)

Share price: HKD 2.93

Market capitalisation: HKD 18,170 mn (USD 2,320 mn)

Enterprise value (EV): HKD 21,650 mn (USD 2,764 mn)

Average daily volume (ADV): HKD 30 mn (USD 4 mn)

NTM P/E: 12x

Time spent: ~1 day

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Pass

Background

Topsports International Holdings Limited (6110 HK) is one of the largest retailers of sportswear in mainland China. It is the main retailer of Nike and Adidas sportswear.

Competitors like ANTA and Li Ning are trading around 14x NTM P/E and 3% dividend yield.

Meanwhile, Topsports is trading at only 12x NTM P/E and offers an attractive 10% dividend yield.

What’s the catch?

Business model

Topsports’ financial year ends in February. Unless stated otherwise, all time references will follow the company’s financial year. For example, FY2025 refers to the year ending on 28 Feb 2025.

Breakdown of FY2025 revenue (CNY 27 bn; -7% YoY):

85% Retail (-7% YoY)

15% Wholesale (-6% YoY)

Topsports is the largest distributor and retailer of NIKE, Inc. (NKE US) and adidas AG (ADS GR) products in mainland China.

As of FY2025, Topsports operates 5,020 stores, down from 6,144 in the prior year. I estimate it holds ~17% revenue market share.

Customers are mainly mass-market consumers in mainland China. No revenue derived from transactions with any single customer represent 10% or more of total revenue.

Purchases from its five largest suppliers accounted for ~95% of Topsports’ total purchases. Purchases from its largest supplier included therein accounted for ~67% of the company’s purchases. This is likely NKE 0.00%↑ .

The closest public comparable is Pou Sheng International (Holdings) Limited (3813 HK), which also distributes Western sportswear like Nike and Adidas under the brand of ‘YYsports’. Pou Sheng is smaller. I estimate it holds ~ 12% revenue market share.

Other competitors include ANTA Sports Products Limited (2020 HK), Li Ning Company Limited (2331 HK) and Xtep International Holdings Limited (1368 HK).

These are domestic sportswear brands. I estimate they hold 45%, 18% and 8% revenue market share respectively.

My reasons

Deteriorating competitive advantage

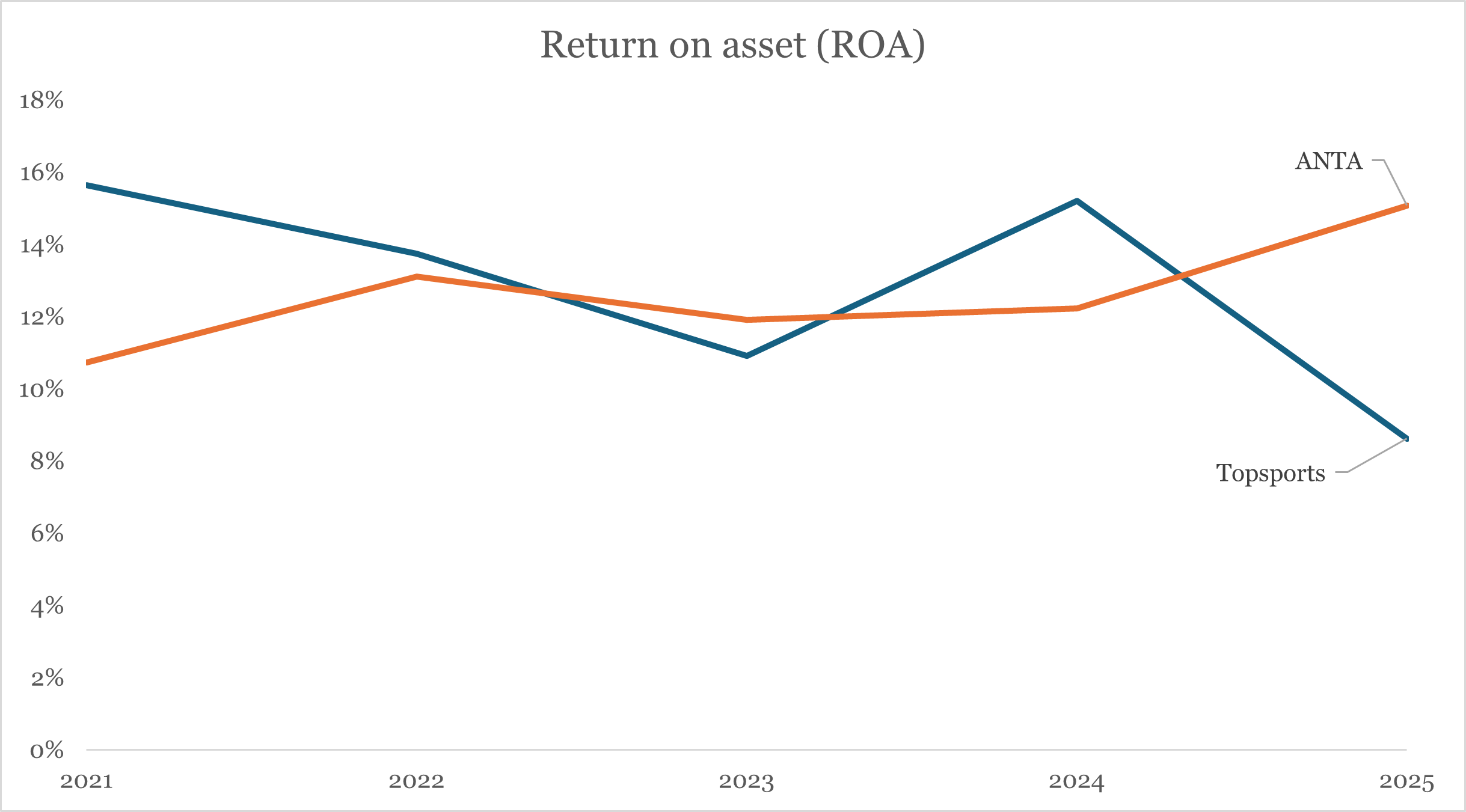

Declining return on assets (ROA). Over the past 5 years, Topsports’ ROA averaged ~13%. This is similar to ANTA.

However, in recent years, Topsports’ ROA started diverging and is on a downward trend. In FY2025, Topsports’ ROA is 9%, much lower than ANTA’s ~12%.

Source: Angsana Anderson’s estimates based on Tikr

Topsports’ declining ROA and ANTA’s improving ROA suggest Topsports’ competitive advantage is deteriorating.

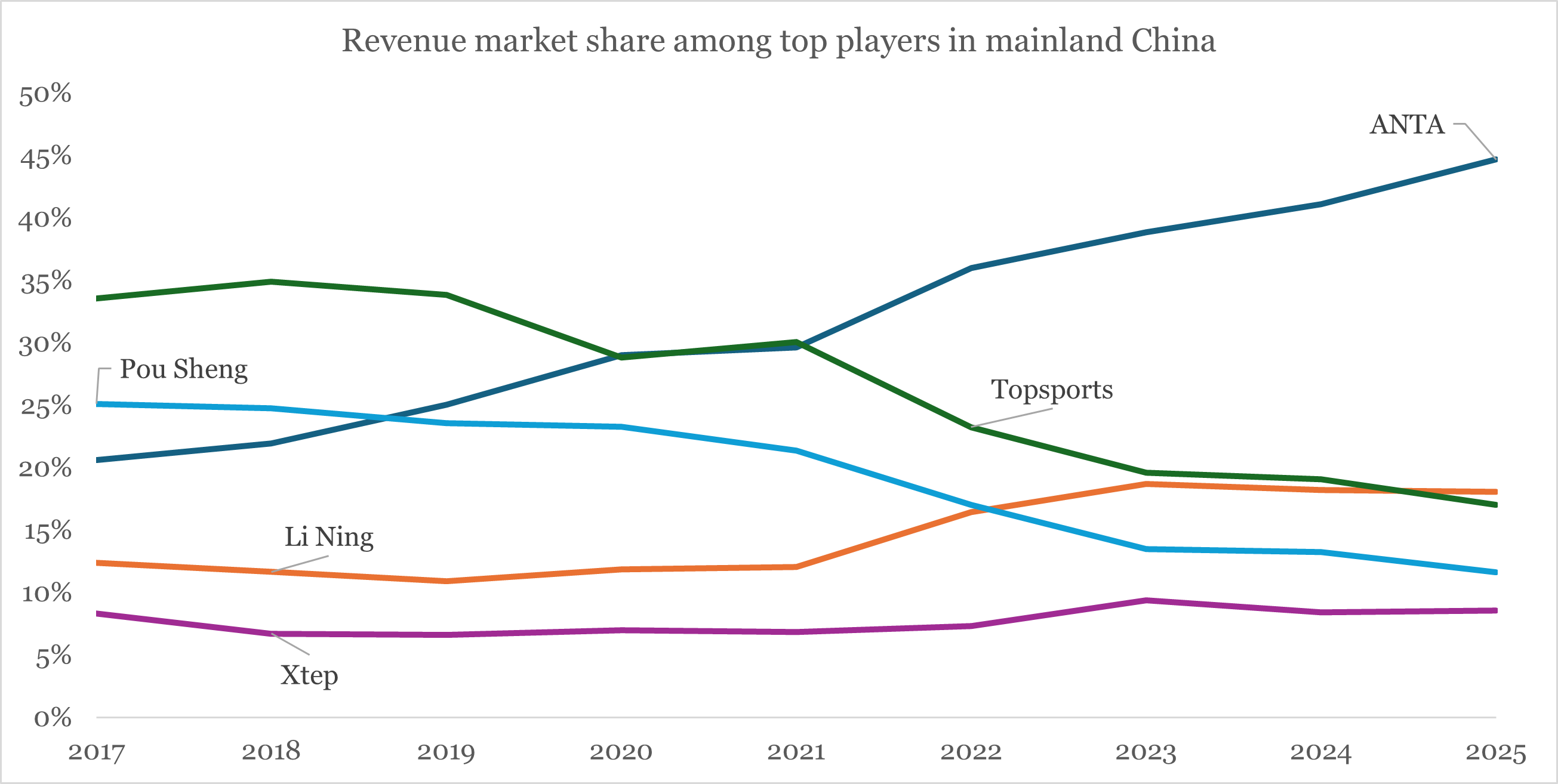

Consumer preference shifting towards domestic brands. Since FY2017, Topsports’ revenue market share has halved from around 30% to 15%.

Source: Angsana Anderson’s estimates based on ANTA, Topsports, Pou Sheng, Li Ning and Xtep data

In FY2022, Topsports’ market share suffered ~7 percentage points (ppt) drop. This was because of the Mar 2021 Xinjiang cotton incident.1

Consumers in mainland China boycotted Western brands like Nike and turned towards domestic brands. ANTA gained ~6 ppt market share. Li Ning gained ~4 ppt.

This is part of a broader trend. Consumers in mainland China increasingly prefer domestic brands.

Starbucks is losing market share to Chinese rivals like Luckin and Cotti. According to Euromonitor, Starbucks’ market share in mainland China has declined from 34% in 2019 to 14% in 2024.2

In calendar 2025, Huawei edged out Apple to reclaim the No. 1 spot in mainland China’s smartphone market.3

It is difficult to tell how far this shift in consumer preference will go on.

Corporate governance

Concentration of power. Yu Wu is the CEO, board chairman, member of the nomination & remuneration committee and is also a substantial shareholder.

Key management pay rising as profits fall. In FY2022, compensation to key management personnel is ~4.4 bps of revenue. By FY2025, it increased to 5.3 bps.

Over the same period, Topsports’ operating profits halved.

Limited disclosures. Despite being significantly impacted by the 2021 Xinjiang cotton incident, I could not find any management discussion over this matter in their annual reports.

Furthermore, I am surprised there has been no impairment of goodwill. Market share and operating profits have declined significantly, and there seems to be little visibility over recoverability.

High dividend yield likely not sustainable

Dividends funded by borrowings. In the past 5 years, operating cash flow totalled CNY 21.6 bn.

After capex, debt repayment and other business needs, there was actually a deficit of – CNY 3.5 bn. Topsports borrowed CNY 15.5 bn and used that to fund CNY 12.2 bn of dividends.

In the last twelve months (LTM), net debt has more than doubled to reach CNY 3.2 bn (2x of operating profits).

Topsports has already begun to reduce dividends. In FY2025, dividends per share declined -22% from CNY 0.36 to CNY 0.28.

Factors that could lead to a re-assessment of my decision

Strong evidence that the unfavourable shift in consumer preference will reverse.

Improvement in corporate governance (e.g. more transparent disclosures, separation of CEO and Chairman roles).

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in 6110, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.

ROA is more important than ROIC in the long term where Profitability Regression is certain to happen.

The higher is the ROA, the higher resistance to Profitability Regression.

That's the reason why Henry Singleton uses ROA in measuring the Return of New Project.