[Thesis] Springer Nature AG & Co. KGaA (SPG; SPG GR)

I became a shareholder because of (a) under-recognised growth and (b) attractive capital returns

Disclaimer: This is a record of my investment decisions, not financial advice. I may change my decisions without notice. Use this only for education and entertainment. All analysis and opinions expressed are solely my own, and SPG has not reviewed or endorsed this post. Do not rely on this for your investment decisions. I own shares in SPG.

About

Share price: EUR 19.00

Market capitalisation: EUR 3,779 mn (USD 4,378 mn)

Enterprise value (EV): EUR 5,021 mn (USD 5,817 mn)

Average daily volume (ADV): EUR 1.1 mn (USD 1.3 mn)

NTM P/E: 12x

My Decision

I decided to become a shareholder of SPG.

I bought my shares at EUR 15.20. Within 3 to 5 years, I expect to sell my shares for at least EUR 24.00.

Over 3 years, I expect to earn ~21% p.a. (16% capital gains; 5% dividend yield). Over 5 years, I expect to earn ~15% p.a. (10% capital gains; 5% dividend yield).

Background

Nature is to science what Hermès is to fashion.

Shares in Springer Nature AG & Co. KGaA (SPG; SPG GR) dropped as much as -24% amid the ‘SaaSpocalypse’. However, the market is probably wrong.

SPG is not software. SPG is a brand. It owns Nature, one of the most prestigious journals in the world. Together with its other portfolio of journals, SPG is the second largest publisher of journals in the world.

I decided to become a shareholder because of (a) under-recognised growth and (b) attractive capital returns.

In this Substack post, I walk through these reasons in detail. I also explain why I am watching out for “tomatoes roaming the fields”.

Business model

Breakdown of 2025 revenue (EUR 1,926 mn, +4.3% YoY):

79% from Research (+7.5% YoY)

10% from Health (+1.5% YoY)

11% from Education (-7.1% YoY)

Research revenue mainly comes from long‑term institutional subscriptions and transformative agreements for journals and eBooks, complemented by open‑access publishing fees. The main customers are academic research libraries.

The Health segment earns revenue from clinical publishing, pharma marketing services, and medical education for healthcare professionals.

Education earns revenue mostly from selling school and language-learning materials while Professional earns revenue from specialist publications, digital tools and industry events for European professionals.

SPG earns ~39% of its revenue from Europe, Middle East and Africa (EMEA), 32% of its revenue from Americas and the remaining 29% from Asia Pacific. Asia Pacific is the fastest growing region.

Most of its revenue is under contract like subscriptions and transformative agreements (52%). The remaining 48% revenue is transactional.

SPG is diversified, with no single customer dominant. In the Research segment, the top 50 customers account for only about 56% of subscription revenue, and overall revenue is spread across thousands of institutions worldwide.

The largest expense is personnel costs (36% of revenue). This mainly consists of wages and salaries for its 9,200 employees across editorial, technology/product, sales and marketing, and corporate/operations roles.

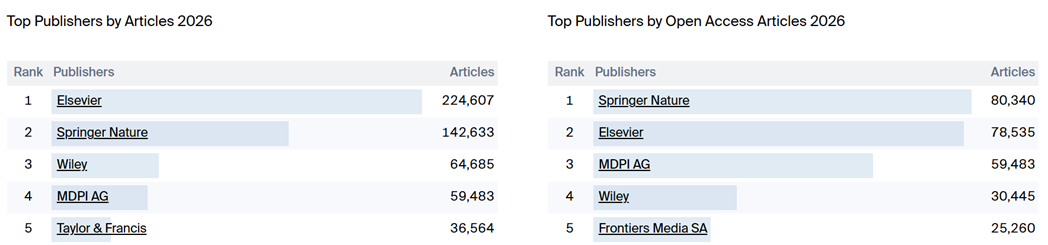

According to Scilit, an online index of research publications, SPG remains the second largest publisher in the world so far in 2026. Its market share has increased to ~12%, up from 9% in 2025.

SPG has even supplanted Elsevier as the largest publisher of open access articles.

Source: Scilit Rankings (2026)

Relevant public comparables include John Wiley & Sons, Inc. (WLY; WLY US), RELX PLC (REL; REL LN), Informa plc (INF; INF LN) and Wolters Kluwer N.V. (WKL; WKL NA).

Source: Tikr (13 Mar 2026)

REL owns Elsevier, WLY owns Wiley, INF owns Taylor & Francis while WKL owns Wolters Kluwer Health.

WLY is the closest comparable to SPG because it focuses on publishing. Other publishers like REL have significant non-publishing activities.

Holtzbrinck Publishing Group owns just over 50% of Springer Nature and effectively controls the company. It is a long‑established German family media group that focuses on high‑profile publishing brands and has a reputation for being astute business owners.

BC Partners, a European private equity firm, owns ~35%.

The free float is largely owned by a mix of mainstream institutional investors and long‑only funds, with no single holder standing out as dominant.

No prominent activist or other alternative‑asset investors are on the shareholder register.

My reasons

Under-recognised growth. The market seems to be trading SPG like it is a software company.

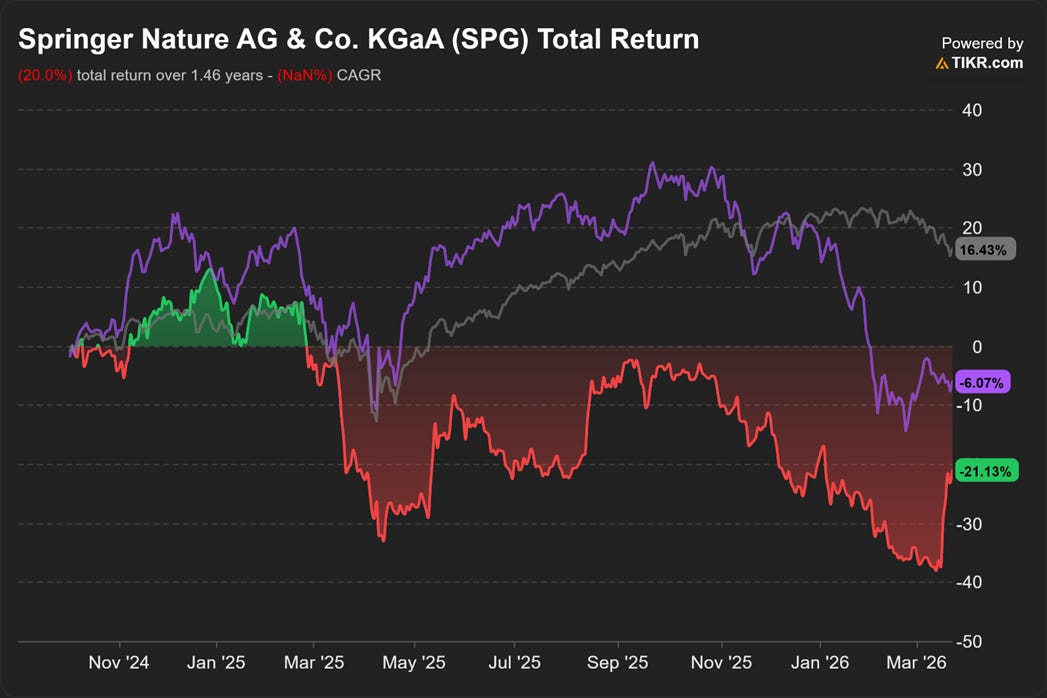

I plot the % change in the price of SPG (green/red) against the price of IGV (purple). IGV is one of the largest ETFs tracking North American software stocks. I also provided SPY, an ETF tracking the S&P 500 index, as a baseline (grey).

SPG and IGV are generally correlated. Since Jan 2026, “SaaSpocalypse” sparked a sharp sell-off of software stocks. SPG sold off sharply too.

SPG delivers ~88% of its research digitally and 52% of its revenue is derived from contracts like subscriptions. However, this is where the similarities with software companies end.

SPG is not a software company. SPG is a brand.

Customers (such as academic libraries) choose SPG because of the quality and prestige of its journals. SPG’s flagship journal is Nature, which publishes many important breakthroughs and has featured work by more than half of Nobel laureates in medicine, physics, and chemistry. It is also among the most cited journals worldwide.

According to a customer at a university, if she faced budget cuts, she would prioritise publishers that she knows are heavily used and that would be missed if they are gone. SPG’s journals will be on that priority list because of their prestige and importance to students and faculty members.

For this reason, researchers choose SPG. For them to be fully recognised as experts in their fields, publication in many of SPG’s journals is often seen as a prerequisite. At some universities, having articles in SPG journals is considered almost essential for achieving tenure over the long run.

Some industry insiders likened SPG to a patent agency. The point of a patent is to register the fact that a researcher reached this discovery first. That’s fundamentally what academic publishing is. It’s about the scientific record. That’s how researchers get employment opportunities and tenure.

I believe the risk from generative artificial intelligence (gen. AI) is low.

Gen. AI helps researchers produce better research. However, I doubt it can completely replace researchers in analysing new data and drawing new conclusions from it. Gen. AI is trained on historical data.

No matter how gen. AI evolves, it won’t change the fact that SPG’s value lies in its branding and reputation, not software capabilities.

Some analysts raised the disintermediation risk. What if academics start reading journals through the likes of ChatGPT, thereby diminishing the brand value of SPG’s journals?

The truth is that people have already been accessing SPG’s journals through intermediaries. In the US, most academic libraries use the same integrated library system called Alma. SPG has integrated its content into that system so that it regularly pulls all new journal articles and loads them directly into the system.

In fact, gen. AI presents opportunities for SPG. WLY has been licensing its content to AI model makers like OpenEvidence and Perplexity. Though still in early stages, WLY forecasts this licensing revenue will contribute ~3% to group revenue in FY2026.

Yet the market is not fully recognising SPG’s ability to sustain or even accelerate its growth. The market seems to be pricing SPG like a software company facing existential threat from gen. AI.

SPG currently trades at 11.5x NTM consensus EPS. On my estimate of sustainable free cash flow to firm, SPG is trading at 8% yield on enterprise value. This is an attractive 5% premium over Germany 10y government bond yield.

Capital returns. In my shortlist of SPG on 13 Mar 2026, I explained why I believed there is a very good chance that SPG will increase dividends.

Indeed, on 17 Mar 2026, SPG raised its dividends from EUR 26 mn to EUR 165 mn. This is a 6.3x increase and just 6% below Fitch’s forecast1. On a per share basis, the dividends increased from EUR 0.13 to EUR 0.83.

When I was shortlisting SPG, the share price was EUR 15.06. This meant dividend yield of ~5.5%. After SPG announced the dividend increase, its share price has since rallied to EUR 19.00. This compressed the dividend yield to 4.4%. 4.4% is still attractive, but not as much as before.

Valuation

I estimate intrinsic value at EUR 24.00 per share based on a discounted cash flow valuation (see Excel model below).

I bought my shares at around EUR 15.20. At this price, I have ~37% margin of safety and 58% upside.

I had originally planned to publish this thesis before SPG released its earnings on 17 Mar 2026, but a severe flu left me bedbound until now. Unfortunately, the share price has increased significantly after the earnings release.

The current share price of EUR 19.00 implies 21% margin of safety and 26% upside. This is still attractive, but not as much as before.

On a near‑term earnings basis, SPG trades at 12x NTM P/E on consensus forecasts and 13x on my estimates.

At my intrinsic value estimate, SPG would trade at 17x NTM P/E. I view this as reasonable given: (a) the under-recognised growth and (b) attractive capital returns.

Prior to the ‘SaaSpocalypse’ sell-off, WLY, SPG’s closest comparable, traded ~ 16x NTM P/E.

Catalysts

1. Revenue growth sustained above low-single digit, driving the consensus to realise that SPG is not software and thus has better growth prospects

2. Higher capital returns

Risks

Transition to open access. Traditionally, libraries and institutions pay publishers for access to journals. This is known as the subscription model.

Academia is shifting towards open access. In the open access model, journals are free to read online. The publisher is instead paid upfront by the author’s funder or institution. This is typically via an article processing charge, or APC.

At first glance, this shift creates uncertainty. However, open access is positive for SPG.

By making journals free to read online, open access increases the demand for journal articles. Open access articles are downloaded 6x more and receive 1.6x more citations2.

Between 2016 and 2025, the number of articles published under open access grew 13% p.a., much higher than 2% p.a. for subscription articles3. SPG’s full open access journals delivered a compound annual revenue growth rate of 12.3% from 2021 to 2023.

I initially thought the shift to open access would mean more volatile revenue. SPG would become more exposed to research funding cycles.

Open access has shifted customers’ spending from library budgets to research-funding budgets. However, research-funding budgets are remarkably stable. Since 2000, global spending on research and development (R&D) has increased every year, including during the 2008 financial crisis and 2020 COVID-19 pandemic4.

In 2020, SPG published ~37% of its articles under open access. By 2025, this % had reached 55%. During this period, SPG’s revenue grew 3.4% p.a.

SPG managed the transition to open access through transformative agreements (TA). TA are multi‑year contracts that give researchers full access to subscription journals while also allowing them to publish their articles open access without paying individual APCs. The TA thereby acts as a transitional mechanism for shifting spending from subscription models toward open access.

In the foreseeable future, I expect TA will be the dominant model for 2 reasons.

First, the subscription revenue from high impact factor journals like Nature is too high. If Nature flips to open access, it would need to charge an APC in the mid-five-figure range to achieve parity with its subscription model. The APC for an open access journal average only between USD 1k to 2k.

Second, 100% open access would mean research-intensive universities will bear the brunt of research publication costs while other universities will ‘piggyback’ off their work. TA solves this problem by charging non-research universities subscription fees to access the best research like those in Nature.

If TA becomes the dominant model as I expect, then SPG will benefit. In its IPO prospectus, SPG reported that revenue from customers under TA grew 4.7% p.a. between 2019 and 2023. This is more than double the typical subscription price increase of ~2% p.a. during the same period. SPG attributes this to the higher usage of articles covered by TA, suggesting increased value creation of TA to its customers.

Private equity ownership. BC Partners, a European private equity (PE) firm is the second largest shareholder (~35% shareholding). There is a risk of prolonged undervaluation as the market anticipates discounted block selldowns.

However, BC Partners has not sold shares after its lock-up period ended in April 2025. This suggests the PE firm believes SPG is undervalued. BC Partners will likely only start selling after the share price has increased significantly.

BC Partners has the holding power to wait for a higher valuation. It currently holds its SPG shares in a continuation fund created in 2021. A continuation fund is typically set up with a 8 to 10 years term. This means the risk from PE overhang will become material only around 2030.

Risk from paper mills. In 2024, WLY suffered major reputational damage, journal closures, and USD 35 to 40 mn of lost revenue after paper mills infiltrated its Hindawi open‑access journals5.

Such risk appears low at SPG. Its portfolio of journals is established and reputable. However, it will be useful to monitor its new journals like the open access Discover journal series.

In June 2025, a group of academics criticised SPG’s new “Discover” journal series as a deliberate copy of MDPI’s high-volume, APC-driven publishing model, arguing it will further erode research quality and trust in science6.

The article mainly argues that Discover looks structurally like an MDPI clone and is therefore risky. However, it does not yet show strong direct evidence that Discover’s current article-level quality is as bad as MDPI’s worst cases. The MDPI article I found funniest was one on “tomatoes roaming the fields”7.

Because most Discover journals are still very new, it is too early to make a definitive judgement on whether the series might drift toward predatory‑style practices. There is currently no clear evidence of such behaviour, but it is still prudent to monitor how Discover develops over time.

Factors that could lead me to increase investment in SPG

1. Evidence that revenue growth can be sustained above mid-single digit for the foreseeable future (e.g. higher demand for open access journals that can be met without compromising quality)

2. Share price falls > 20% without significant deterioration in business fundamentals

Factors that could lead me to decrease investment in SPG

1. Evidence of pervasive predatory publishing

Upcoming events

Tue 31 Mar 2026: Publication of 2025 annual report

Tue 5 May 2026: Q1’26 earnings release

Thu 28 May 2026: Annual general meeting

For more analysis like this, subscribe to my Substack

Your deep dive into Springer Nature (SPG) highlights a classic "quality at a reasonable price" thesis, especially regarding their transition to Open Access. It’s a great case study on how a legacy gatekeeper can pivot its business model to capture value from the high volume of research output rather than just subscription access.

With the push toward "Plan S" and decentralized publishing, how do you see their profit margins evolving? Do you think the increased volume from Open Access APCs (Article Processing Charges) can fully offset the potential long-term erosion of their high-margin institutional subscription bundles?