HRnet: Reaching an inflection point?

[Thesis] HRnetGroup Limited (CHZ; HRNET SP)

Disclaimer: This is a record of my investment decisions, not financial advice. I may change my decisions without notice. Use this only for education and entertainment. All analysis and opinions expressed are solely my own, and CHZ has not reviewed or endorsed this post. Do not rely on this for your investment decisions. I own shares in CHZ.

About

Share price: SGD 0.73

Market capitalisation: SGD 722 mn (USD 580 mn)

Enterprise value (EV): SGD 412 mn (USD 343 mn)

Average daily volume (ADV): SGD 100 k (USD 80 k)

NTM P/E: 14.7x

My decision

I decided to become a shareholder of CHZ.

The share price now is SGD 0.73. Within 3 to 5 years, I expect to sell my shares for at least SGD 1.27.

Over 3 years, I expect to earn ~27% p.a (21% capital gains; 6% dividend yield). Over 5 years, I expect to earn ~18% p.a. (12% capital gains; 6% dividend yield).

Background

The share price of European recruitment agencies such as Adecco Group AG (ADEN; ADEN SW) is down -68% in the past 5 years. During the same period, Japanese recruitment agencies like Persol Holdings Co.,Ltd. (2181; 2181 JP) is up +12%. What happened?

The short answer: Japan is facing a tight labour market, while economic growth in many European economies has been weak.

Singapore’s labour market seems to be reaching an inflection point, yet this is not widely recognised.

HRnetGroup Limited (CHZ; HRNET SP) is Singapore’s largest recruitment agency. I decided to become a shareholder because (a) CHZ is a good business facing temporary headwinds; (b) potential for capital returns and (c) under-recognised growth.

In this Substack post, I walk through these reasons in detail and explain the risks I am watching. You can also access my Excel model in my Substack post.

Business model

Breakdown of 2025 revenue (SGD 584 mn, +3% YoY):

90% from flexible staffing (+3% YoY)

9% from professional recruitment (+2% YoY)

1% from others (+1% YoY)

Revenue from flexible staffing is earned from providing contractor employees to clients and billing them a marked‑up service fee on top of the contractors’ payroll and benefit costs, generally invoiced monthly as services are rendered.

Revenue from professional recruitment is earned from billing clients a fee calculated as a percentage of the successful candidate’s first-year remuneration, recognised when the candidate signs the employment contract or starts work.

84% of revenue is derived from private sector while 16% from public sector.

24% of revenue is derived from IT & tech, 21% from financial & insurance and 14% from retail and consumer. The remaining 41% is derived from healthcare, manufacturing, services and others.

No single customer accounted for > 10% of revenue. Top 5 clients contribute ~17% of revenue. These clients have been with them for an average of 18 years.

The largest expense is sub-contractor expenses (79% of revenue). This mainly consists of the payroll of contractor employees deployed to customers.

Because of this, breakdown by gross profit is more meaningful (SGD 123 mn, +1% YoY):

52% from flexible staffing (0% YoY)

45% from professional recruitment (+1% YoY)

3% from others (+7% YoY)

52% of gross profit is earned from Singapore, 43% from North Asia (mainly mainland China and Taiwan) and 5% from rest of Asia like Malaysia, Indonesia and Thailand.

At its IPO in 2017, CHZ is the largest recruitment agency in Singapore, with revenue market share ~20%1. The second and third players are Kelly Services (aka PERSOLKELLY) and Adecco. Both have ~10% revenue market share each. The remaining players are much smaller.

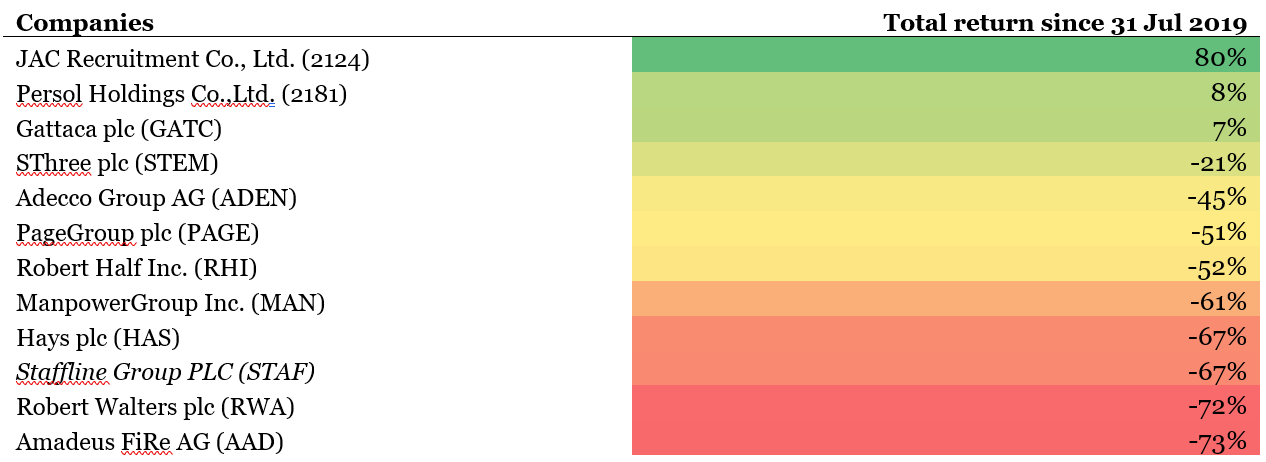

Relevant public comparables include Persol Holdings Co.,Ltd. (2181; 2181 JP), Adecco Group AG (ADEN; ADEN SW), ManpowerGroup Inc. (MAN; MAN US), Amadeus FiRe AG (AAD; AAD GR) and JAC Recruitment Co., Ltd. (2124; 2124 JP).

Source: Tikr (20 Feb 2026)

ADEN, MAN and ADD have significant exposure to Europe and are therefore the worst hit by the slowdown in economic growth in Europe. 2181 and 2124 earn most of their revenue from Japan. Because of the tight labour market in Japan, they performed among the best globally.

The Sim family owns ~80% of CHZ. Founder Peter Sim, his brother JS Sim and his daughter Adeline Sim serve as executive directors. In April 2025, Fidelity emerged as the second-largest disclosed shareholder (~8%), ahead of a long tail of broker and nominee accounts. No other visible activist or private equity players on the shareholder register.

Thesis

Good business, temporary headwinds. CHZ is a good business. Its competitive advantage arises from its position as the largest recruitment agency in Singapore with a long and proven track record.

Clients use CHZ for flexible staffing because it has a long track record and the balance sheet to fund these working capital requirements. Few competitors can support this level of working capital.

Clients use CHZ for professional recruitment because CHZ combines a structured search methodology with a strong brand and long track record. Clients have an incentive to use a widely recognised brand. If a client uses a no-name recruitment agency and the new hire turns out to be bad, the client will be blamed. If you’re the HR on the client’s side, why risk your career?

Because of these reasons, CHZ has achieved a good return on equity (ROE), despite a significant cash pile. Last twelve months (LTM) ROE ~13%. Prior to the current downturn, its ROE averaged 18%.

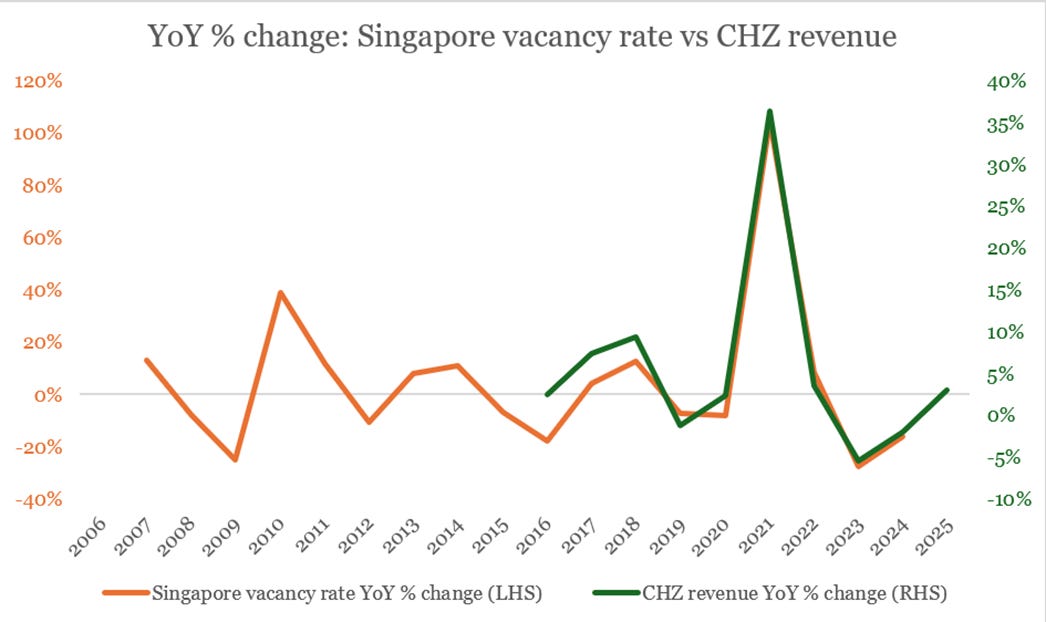

Like its global peers, CHZ has been facing economic headwinds. However, I believe an inflection point is here. In 2025 H2, gross profit grew +4.2% YoY. This is the first time gross profit grew since it started declining in 2022 H2. Analysis of Singapore’s job vacancy rate suggests that CHZ’s gross profit growth is sustainable.

Figure 1 shows that YoY % changes in CHZ’s revenue closely track YoY % changes in Singapore’s job vacancy rate. The job vacancy rate measures unfilled labour demand (job vacancies) as a share of total jobs. A rising rate indicates a tighter labour market with more unfilled positions. This is good news for recruitment agencies like CHZ.

Figure 1: YoY % changes in CHZ’s revenue closely track YoY % changes in Singapore’s job vacancy rate

Figure 2 shows YoY % change in quarterly job vacancy rate. The data has bottomed out around Q2’24 and has been on an upward trend ever since. The latest data in Q3’25 shows that the YoY % change in job vacancy rate has finally turned positive. The Ministry of Manpower (MOM) will only publish the data for Q4’25 around mid-Mar 2026. Nonetheless, past cycles suggest a high likelihood that the job vacancy rate will continue growing in Q4’25. This means CHZ’s revenue and gross profit will likely continue growing YoY. Barring any significant exogenous shocks, downside risk is low, at least for the next few quarters.

Figure 2: YoY % change in quarterly job vacancy rate finally turned positive in Q3’25

This view of a sustained recovery is further supported by trends in CHZ’s contract liabilities. In 2024, growth in contract liabilities finally turned positive. This pointed to a recovery in 2025. Indeed, in 2025, CHZ’s revenue and gross profit YoY growth finally turned positive too. In 2025 H2, other payables and accruals, which includes contract liabilities, increased +3% YoY.

Finally, during the earnings call on 26 Feb 2026, management reported that they already have visibility of the pipeline for H1’26. The pipeline quality has improved compared to last year.

However, the market has not recognised that CHZ is a good business, that its headwinds are temporary, and that an inflection point is here. CHZ currently trades at ~9% free cash flow to firm (FCFF) yield on enterprise value (EV), based on my estimate of sustainable FCFF. This is a very attractive ~7% premium over Singapore’s 10y government bond.

Capital return. I believe there is a good chance that CHZ will return more capital to shareholders.

In 2025, CHZ had ~SGD 336 mn cash pile (~47% of market cap.). Management has earmarked SGD 40 mn (~6% of market cap.) for dividends and SGD 10 mn (~1% of market cap) for share buybacks.

CHZ increased its dividends in 2025. The full year dividend reached 4.2 cents, up 5% from 4.0 cents last year. Dividend payout ratio increased to 78%, above its historical range of 50% to 60%. At the current share price, this implies a dividend yield of ~6%, an attractive ~4% premium over Singapore 10y government bond.

Management sees dividends of 4 cents per share to be strong and sustainable. They also indicated that when the business performs well and value is unlocked from its investments, it intends to share more with shareholders, as they have done this time. Unlike many peers that pay lip service to capital returns, CHZ has backed words with action through higher dividends.

Under-recognised growth. CHZ has earmarked SGD 156 mn of its cash pile for M&A and organic growth. During my meeting with Jennifer Kang (CHZ Group CFO), she explained CHZ hopes to execute a sizeable M&A deal.

For example, a business generating SGD 31 mn of NPAT, acquired at 10x P/E for a 51% stake — would imply a consideration of about SGD 156 mn. This is well within CHZ’s financial capacity, while retaining the optionality to take on debt if it enhances returns or accelerates growth.

On a pro‑forma basis, an M&A like this would add ~SGD 16 mn of attributable NPAT to CHZ. This will lift group NPAT by 30% to ~SGD 67 mn. Today’s market cap. of SGD 717 mn would equate to only ~11x pro‑forma earnings, suggesting the market is not pricing in CHZ’s M&A growth option yet.

Valuation

I estimate intrinsic value at SGD 1.27 per share based on a discounted cash flow valuation (see Excel model below). At the current share price, this implies approximately 43% margin of safety and 76% upside.

On a near‑term earnings basis, CHZ trades at 14.7x NTM P/E on consensus forecasts and 12.8x NTM P/E on my estimates, suggesting the market has yet to fully price in the earnings inflection ahead.

At my intrinsic value estimate, CHZ would trade at 22.4x NTM P/E, which I view as reasonable given: (a) the underlying business quality and largely temporary nature of current headwinds, (b) the potential for higher capital returns, and (c) attractive growth opportunities via M&A.

Japanese recruitment companies like 2181 and 2124 trade at ~ 22x on average in the past 5 years.

Catalysts

Acceleration in the growth of gross profits

Higher capital returns

M&A

Risks

Headwinds may not be temporary. There is a risk that a downturn in hiring activity could result in only a short-lived recovery of gross profits.

Nonetheless, this risk appears to be limited. The YoY % change in Singapore’s quarterly job vacancy rate bottomed out around Q2’25 and has recently turned positive in Q3’25. Historical trends suggest that this improvement is likely to persist for at least the next 12 months.

This outlook is further supported by positive working capital movements at CHZ and management’s recent commentary. Contract liabilities, a leading indicator of revenue, have increased for the first time in 2024 and has likely increased further in 2025. Additionally, management has highlighted an improved sales pipeline heading into the first half of 2026.

Mass unemployment from generative AI disruption. There is a risk that generative artificial intelligence (AI) will reduce junior white-collar jobs. CHZ is already seeing signs of this.

To mitigate this, CHZ is leaning into executive search. Senior roles are less impacted by generative AI. However, it is still not clear how much this pivot can offset the weakness.

I believe this risk is limited in the long run. Prolonged mass unemployment among young workers is socially unacceptable and politically costly. Governments will likely find ways to re-employ displaced workers. In fact, the Singapore government has already launched a slew of initiatives to do this.

Capital allocation. There is a risk that future M&As may destroy value.

In 2019, CHZ acquired a ~29% stake in Staffline Group PLC (STAF; STAF LN). According to SIAS, CHZ invested ~SGD 56 mn in STAF and suffered significant losses. SIAS questioned if it is prudent for CHZ to invest when it does not appear that CHZ has access to detailed financial information to carry out due diligence nor had CHZ been able to appoint a non-executive director to the board of STAF2.

In the same document, CHZ said the loss did not affect the group’s P&L because the investment is carried at FVTOCI. In my view, regardless of CHZ’s accounting policy, this is still an economic loss.

At first glance, it may seem that management has done a poor job of allocating capital. However, their investment performance needs to be understood in a wider context.

CHZ first invested in STAF on 31 July 2019. In the table below, I estimate the total return CHZ would have earned had it instead invested in other listed recruitment companies over the same period. Despite the unrealised losses on STAF, the data suggest CHZ had limited scope to do materially better within the listed recruitment sector, given the unexpectedly weak labour market in much of the world.

Source: Tikr

Finally, there are signs that STAF is also turning the corner. In STAF’s latest full year trading update, it reported it expects 2025 results to be significantly ahead of market expectations3

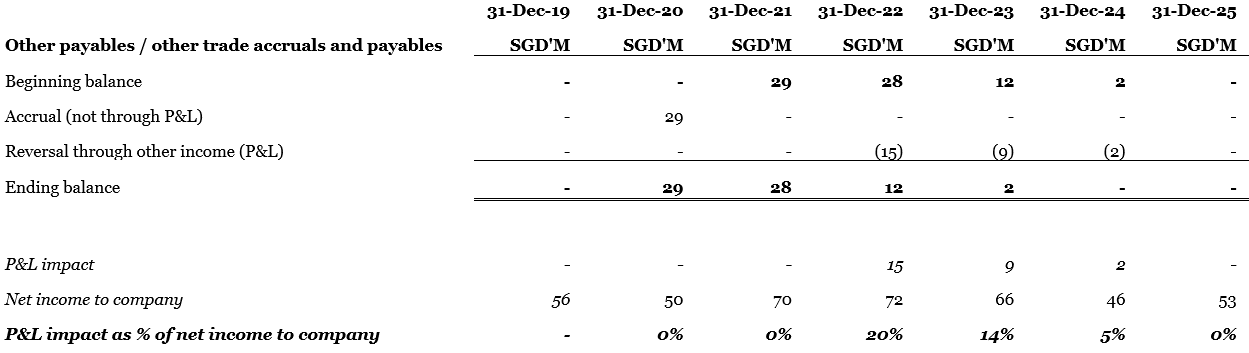

Other payables. Between 2020 and 2023, CHZ reported ‘other payables’:

SGX-ST queried CHZ on the 2022 balance. CHZ replied that these “…were monies set aside in year 2020 and 2021 for contingencies to respond to trade related situations during the pandemic. The counterparties are not related parties.”

When asked why the balance declined significantly in 2022, CHZ said “The reversal was made … after considering historical data and qualitative reasonable forward-looking information to estimate the amount that was no longer needed. The amount was S$14.8m ...”4

Although this item is non-recurring and will have no financial impact from 2025 onwards, I remain puzzled by its accounting treatment. The accrual recognised in 2020 does not appear to have affected the profit and loss statement (P&L). It is unclear how this other payable was initially recorded in 2020 and why, if it did not impact the P&L then, its subsequent reversal was routed through the P&L in later years. Because this is material, I am asking management for further clarification.

Factors that could lead me to increase investment in CHZ

Significant improvement in quarterly job vacancy rate

Value‑accretive M&A at an attractive valuation

Capital returns that are higher than expected

Share price falls > 20% without significant deterioration in business fundamentals

Factors that could lead me to decrease investment in CHZ

Material accounting treatments that I cannot understand

No meaningful use of the cash pile (dividends, buybacks, or value‑accretive M&A) over the next 3–5 years

Upcoming events

Sat 14 Mar 2026: SIAS Market Outlook - Corporate Connect with HRnetGroup (link)

Mid-Mar 2026: MoM publishes Singapore job vacancy rate for Q4’25 (link)

Tue 21 Apr 2026: Annual general meeting

If you want more analysis like this, subscribe to my Substack

Updates:

(1) Other payables no longer a risk factor.

Management has confirmed that the SGD 29 mn other payables first recognised in 2020 were "trade-related monies that were received and set aside as accruals to deal with uncertain commercial situations during the pandemic."

It seems to me that because of the uncertainties arising from COVID-19, management did not recognise as income some of the cash they received from customers.

Hence, they recorded those cash as other payables instead of income. When the uncertainty was resolved in later years, CHZ then recognised it as income.

I am satisfied with the explanation.

(2) YoY % change in Singapore's job vacancy rate dipped to 0% in Q4'25, down from +3.7% in Q3'25.

I see this as neutral. Overall, the upward trend is still holding.

MoM will release Q1'26 job vacancy rate around mid-June.