ThaiBev: After falling -50%, is it time for me to buy?

[First Take] Thai Beverage Public Company Limited (Y92; THBEV SP)

Summary

I decided to pass because near-term demand looks weaker than expected, but capex continues to increase.

While management has a great track record in Thailand, their capital allocation outside Thailand has delivered disappointing returns so far.

About (11 May 2026)

Share price: SGD 0.43

Market capitalisation: SGD 10,681 mn (USD 8,405 mn)

Enterprise value (EV): SGD 21,207 mn (USD 16,688 mn)

Average daily volume (ADV): SGD 8 mn (USD 6 mn)

NTM P/E: 10x

Time spent: ~1 day

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Pass

Background

It’s 2016. You’re lying on the beach in Phuket. Hot sweltering heat. Cold refreshing beer. Paradise on earth.

Back in your office, you discovered ThaiBev brews your favourite beer in Thailand. Chang and its rival Singha form a cosy duopoly.

Your heart skipped a beat when you realised ThaiBev is listed in Singapore. Despite its seemingly expensive NTM P/E of 20x, you bought a significant block.

After all, you know the product well. The company has steadily grown its revenue by ~6% p.a. over the past 10 years.

Surely, 20x P/E is not that expensive for such a quality stable stock?

Fast forward 10 years, you’ve suffered a total loss of -20%. What happened?

More importantly, with its NTM P/E at an all-time low of 9x, is ThaiBev finally cheap enough to buy?

Business model

ThaiBev’s financial year ends in Sep. Unless stated otherwise, all time references will follow the company’s financial year. For example, Q2’26 refers to Jan 2026 – Mar 2026.

ThaiBev is the largest beverage company in ASEAN by sales.

The company holds ~90% volume market share in Thailand’s spirits market. Through its beer brands like Chang and Bia Saigon, ThaiBev holds a strong market share of 35% to 40% in Thailand and Vietnam.1

Breakdown of FY2025 revenue (THB 333 bn; -2% YoY):

37% Beer (-2% YoY)

36% Spirits (-2% YoY)

19% Non-alcoholic beverage (-1% YoY)

7% Food (-2% YoY)

1% Others (-11% YoY)

The Beer segment produces and sells branded beer such as Chang beer, one of Thailand’s most popular beers.

The Spirits segment produces and sells branded spirits such as Hong Thong and Ruang Khao. These are the best-selling brown and white spirits in Thailand, respectively.

The Non-alcoholic beverages segment produces and sells branded water, ready-to-drink coffee, energy drinks, green tea, fruit flavored drinks and dairies product. Brands include Fraser & Neave (F&N) and Oishi.

The Food segment operates restaurants such as KFC Thailand and Oishi Sushi.

In 2025, 65% of revenue comes from Thailand, 15% from Vietnam, 7% each from Malaysia and Myanmar.

Main customers include distributors and retailers. ThaiBev did not disclose any major customers.

Public comparables include Emperador Inc. (EMI PM) and Carabao Group Public Company Limited (CBG TB).

EMI is a Philippines‑based global spirits company that produces brandy and Scotch whisky brands such as Emperador, Fundador, The Dalmore and Jura.

CBG is a Thai beverage company that produces Carabao‑branded energy drinks and related beverages.

My reasons

Demand looks weaker than expected

Declining spirits. In FY2025, the Spirits segment recorded a -2% YoY decline in revenue. Sales volume declined by -3%. This was partially offset by +1% increase in average selling price (ASP).

FY2025 is the third consecutive year of sales volume decline. In fact, Spirits sales volume has never recovered to its peak in FY2020.

Management denied this was a structural issue. They attributed the weak volume to a weak post-COVID economy and high household debt levels resulting in weak consumer purchasing power.2

I am not fully convinced. Since 2020, Thailand’s real annual GDP growth rate has recovered and hovered around low-single-digit.

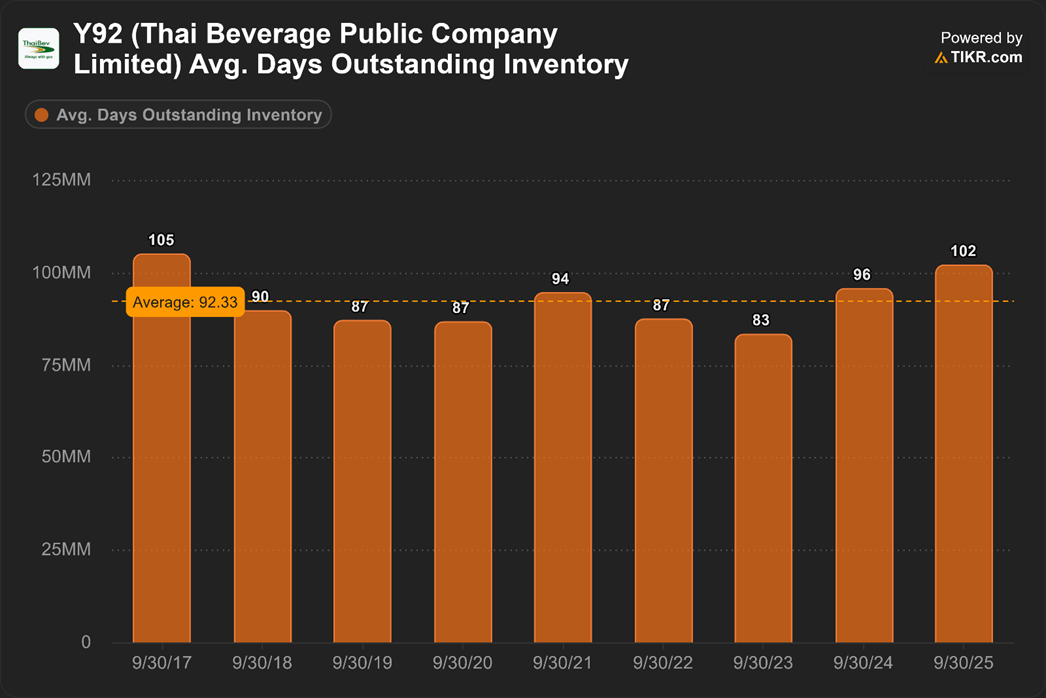

Near-term demand looks weaker than expected. Consensus forecasts revenue growth will recover from -2% in FY2025 to +3% in FY2026. However, working capital trends suggest near-term demand remains weak.

Average inventory days increased for the second consecutive year and is now above 10-year average.

The increase was concentrated on finished goods. Coupled with the revenue decline, this suggests demand was weaker than expected in FY2025.

At the same time, raw materials were flat. Management likely does not see demand recovering in FY2026.

But capex continues to increase

Capex reached all-time high. In the past 10 years, capex averaged 3% of revenue. It started increasing from FY2023 and reached THB 18 bn in FY2025 (~6% of revenue). ThaiBev allocated 40% of the elevated capex to the non-alcoholic beverage segment and 20% to the beer segment.

I estimate the bulk of the capex for non-alcoholic beverage went into F&N AgriValley, a dairy farm in Malaysia. This is a ~THB 25 bn project that will see up to 20,000 dairy cattle when completed.

But demand is not obvious. The dairy industry is quite mature in Malaysia. Roland Berger, a consultancy, forecasts low growth over the next 10 years.3 Milk consumption per capita is already among the highest in Southeast Asia.4

Management explained, “It’s more that Malaysian actually consume a lot of recombined milk, right, not the fresh milk. So our goal is to provide good access to quality fresh milk for Malaysian people.”

Competition is strong. The market is dominated by incumbents such as Dutch Lady Milk Industries Berhad (DLADY MK) and Farm Fresh Berhad (FFB MK).

DLADY is the market leader with ~28% overall market value share. It has been operating in Malaysia since 1963. FFB started around 2009. It grew quickly by focusing on chilled fresh milk, eventually dominating the segment with ~60% market share.

Mixed record in capital allocation

Great track record in Thailand. The Sirivadhanabhakdi family showed extraordinary management skills. They first launched Chang beer in 1995. Through low price, good timing, and aggressive business practices, Chang has overtaken Singha, the incumbent beer brand.5

Not so great outside Thailand. However, outside of Thailand, their track record is mixed.

In 2007, ThaiBev acquired 54% of Saigon Beer - Alcohol - Beverage Corporation (SAB VN) for USD 6.5 bn.6 SAB is Vietnam’s largest beer brewery.

Today, ThaiBev’s stake is worth only USD 1.2 bn. I estimated ThaiBev collected around USD 0.6 bn of dividends from SAB.

It is difficult to calculate the exact cost per share that ThaiBev paid for Vietnam Dairy Products Joint Stock Company (VNM VN).

However, the fair value of its stake in VNM is only 40% of its carrying value. This suggests ThaiBev likely is incurring a loss on this acquisition too.

Risk of write-down. So far, ThaiBev has not written down the carrying value of its stake in VNM.

I suspect this is because they believe the value in use of VNM remains above the carrying value.

However, if the fair value of VNM remains significantly below the carrying value, I would view this assumption as increasingly optimistic.

Factors that could lead to a re-assessment of my decision

Spirits volume recovers better than expected

Inflection in working capital trends that suggest near-term demand will be better than expected

Better-than-expected returns on capex in Malaysia

Turnaround in VNM and SAB

Free cash flow to firm (FCFF) yield on enterprise value increases to ~7.2% (5% premium over Thailand 10y government bond yield). Current FCFF yield is ~6.0%.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in THBEV, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.