Springer Nature: Not an AI-loser

[Update] Springer Nature AG & Co. KGaA (SPG GR)

Summary

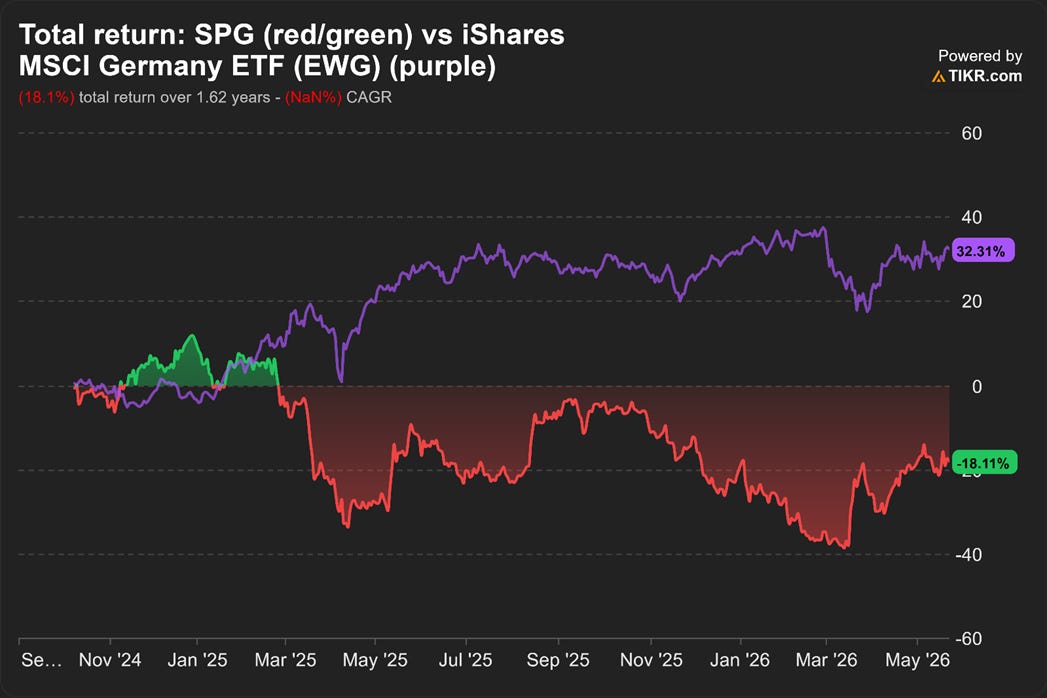

In early 2026, Springer Nature (SPG GR) was caught in the software sell-off, driven by AI disruption fears.

However, SPG faces low AI-disruption risk. SPG is in the business of supporting the creation, verification and dissemination of new knowledge. In fact, AI helps accelerate the research and publication process, improves the dissemination of research and maintains research integrity.

By and large, the transition to open access is beneficial not only to publishers but also to researchers and readers. The transition will likely remain gradual, thereby mitigating risk of sudden disruptions.

While dividends and organic investments will remain core uses of free cash flow, SPG is also open to mergers and acquisitions. Share buybacks are also possible, but they are constrained by the relatively low free float.

If BC Partners, the private equity firm and also the second largest shareholder, continues to exit, share buybacks can become a more practical and significant way to return capital to shareholders.

About (22 May 2026)

Share price: EUR 19.94

Market capitalisation: EUR 3,966 mn (USD 4,603 mn)

Enterprise value (EV): EUR 5,208 mn (USD 6,045 mn)

Average daily volume (ADV): EUR 1.4 mn (USD 1.6 mn)

NTM P/E: 12x

Background

How is generative artificial intelligence (AI) impacting the scientific publishing industry? Why are more and more researchers publishing their papers for free? What do investors usually misunderstand about Springer Nature?

On 5 May 2026, Springer Nature AG & Co. KGaA (SPG GR) released its Q1’26 earnings. The results were good.

I met Tom Waldron, the new Head of Investor Relations. He joined SPG in Sep 2025. Tom brings a wealth of experience from the buy-side and sell-side, and most recently served as Head of Investor Relations at WPP plc, one of the world’s largest advertising agencies.

In this post, I summarise the main takeaways from our conversation.

I would like to thank Tom for his time. He has reviewed this post for factual accuracy. I retained full editorial independence.

Our conversation

How will generative AI impact you?

SPG caught in the software sell-off. In early 2026, investors sold off software stocks because of AI disruption fears. SPG was caught in the sell-off.

Low disruption risk. Although there is some software element in SPG’s business, the company’s core value proposition is creating trust.

Large language models (LLM) are useful in mining old knowledge. However, SPG’s business is about the creation and verification of new knowledge.

Accelerate the research and publication process. Historically, the volume of research increases ~5% p.a. Generative AI has the potential to increase this growth by accelerating the research and publication process.

The most obvious example is translation. Researchers who are non-native English users now find it easier to publish in English and reach a wider audience.

With higher volume of research, the scientific community will need help. AI can help.

SPG has incorporated AI into their proprietary publishing platform (SNAPP). For example, SNAPP uses AI to scan the research paper’s content to suggest suitable peer reviewers.

SNAPP currently covers ~50% of their journals. Processes in academia evolve gradually. But the advantages of SNAPP and its AI tools are real, so the coverage and application of its AI tools will continue increasing. This is the first area to apply AI.

Dissemination of information. The second application of AI is around the dissemination of new knowledge.

Nature Research Assistant is Springer Nature’s AI‑powered tool that helps researchers discover, read, and write papers more efficiently.

It can generate structured summaries of articles and lets the users “chat with” a paper. The tool also surfaces related and foundational literature around a topic to speed up building a mental map of the field.

Another opportunity is licensing its huge catalogue of proprietary data and knowledge to corporate clients like R&D departments and LLM developers.

On 7 May 2026, SPG announced it is integrating directly into Claude to give institutional subscribers access to its proprietary drug development and clinical trial data. This integration is powered by a secure Model Context Protocol (MCP) server.1

The MCP server allows Claude to retrieve and ground its responses in real-time, licensed content from SPG. At the same time, it prevents the LLM from ‘ingesting’ the data. SPG maintains control over its proprietary knowledge.

There is potential for licensing deals like this to form a part of SPG’s revenue streams. People have become much more sensitive to the sources used by LLM because of their tendency to hallucinate.

However, we have not published how significant this revenue potential will be. We are taking a careful approach to licensing revenue because we want to maintain control over our proprietary data.

Maintain research integrity. The third AI application is maintaining research integrity.

After a researcher submits a paper, SNAPP uses tools and checks to help editors spot genuine errors, deliberate misconduct (including the illegitimate use of AI) and fraudulent papers created by “paper-mills”.

SNAPP runs AI-assisted integrity checks to detect manipulated images and hallucinated citations. These allow SPG to flag potential paper-mill or fabricated content early before the papers even reach human editors and peer reviewers.

There is an element of an arms race. Just as SPG is adopting advanced AI tools, the paper mills are also becoming more sophisticated.

Peer review is the final firewall that protects the scientific record, the communities of scientists involved and the reputation of SPG’s brands. In the vast majority of cases, human peer reviewers will spot fabricated papers from paper mills. Their feedback improves SPG’s AI screening process.

Because of all these mitigating factors, the level of retraction across SPG’s portfolio of journals is very low.

In 2025, SPG received over 3.1 mn submissions, of which only 539,000 articles were published. During the same year, 1,462 retractions took place. 57% (833 articles) of retractions were for papers published before Jan 2024.

Some level of retraction is natural because of genuine mistakes. Scientific methodology improves continuously. What used to be acceptable may no longer be reliable. Other times, articles can get retracted due to technicalities, such as authors making unintentional copyright errors.

How will open access impact you?

From pay-to-read to pay-to-publish. Historically, publishers were paid through journal subscriptions. As distribution became digital, access widened, but the model remained fundamentally pay-to-read.

Around 25 years ago, the industry began shifting toward pay-to-publish. In this model, articles are free for readers, while authors or their institutions pay an article processing charge (APC). This is also known as open access (OA).

The APC covers services such as peer-review coordination, editorial support and dissemination. That shift is the foundation of the open-access transition.

Open access works. Open access benefits researchers and funders because it allows research to reach the widest possible audience. It also works well for publishers because payment is tied more directly to the services they provide, such as managing peer review and dissemination rather than to limiting access behind a paywall.

Furthermore, funding increasingly comes from the broader research budget rather than narrower library budget. Research budgets have generally grown by 3% to 4% p.a., versus 1% to 2% p.a. for library budgets.

Transformative agreements are accelerating the shift. Pure open access is transactional, but transformative agreements (TAs) have become a key mechanism for accelerating adoption. SPG signed its first transformative agreement in 2015 with the explicit goal of driving open access.

Under these agreements, university consortia pay in advance for APCs, making the process more predictable and scalable. SPG now has more than 85 transformative agreements covering around 4,000 institutions.

SPG leads the open access transition partly because its subscription portfolio has long offered strong value for money. On a per article basis, SPG’s subscription fees are relatively low. That made the shift easier while still allowing SPG to be paid appropriately for the services it provides.

Revenue visibility remains strong. SPG still retains good revenue visibility during the transition. Around 60% of research revenue is contracted in advance, while roughly 40% comes from transactional sources such as APCs.

Even for transactional revenue, the roughly 200-day period between article submission and publication provides good visibility.

The transition will likely be gradual. Last year, SPG published around 53% of its articles under open access. SPG also owns two of the most cited open-access journals, Nature Communications and Scientific Reports.

In 2025, the company launched 48 new open-access journals and signed 19 new TAs. The transition is continuing, but it remains gradual rather than disruptive.

Europe is already heavily oriented towards TAs, while the US has moved more slowly.

Some large scholarly societies still earn relatively high subscription revenue per article and therefore have less incentive to change quickly to OA.

Incentives also differ across universities: research-intensive institutions may still prefer subscriptions, while less research-intensive universities may favour open access.

What are your shareholders’ plans?

Free float likely to continue increasing. The Holtzbrinck family owns ~50% of SPG. The family will likely remain a long-term shareholder.

BC Partners, a private equity (PE) firm, owned just under 50% before SPG’s IPO. The PE firm partially exited at the IPO and created the current free float.

The market expects BC Partners to continue exiting over time. If that happens, the free float should increase, which could improve liquidity and broaden the shareholder base.

How do you plan to use your free cash flow?

Free cash flow likely to continue growing in 2026. For the full year 2026, SPG expects free cash flow (FCF) to grow broadly in line with, or slightly faster than, adjusted operating profit (AOP).

In Q1’26, FCF was better than expected. This was mainly because of timing benefits from promissory notes and investments.

Deleveraging still matters. The EUR 165 mn dividend payment in Q2’26 will likely increase financial leverage slightly.

Management still sees value in reducing leverage. Lower debt supports lower interest costs and should help ahead of upcoming refinancing.

Organic investments. As discussed earlier, SPG continues to see attractive opportunities to invest in AI tools and launch new journals.

SPG also considers mergers and acquisitions (M&A). Management is also open to acquisitions, especially assets that strengthen SPG’s technological capabilities or further the company’s strategies.

Dividends remain a core use of cash. The company intends to maintain a strong balance sheet and a progressive dividend. Management has committed to paying out 50% of its adjusted net income, which should allow the dividend to grow over time. This makes the current 4% dividend yield even more attractive.

Buybacks are possible, but not yet ideal. At the upcoming annual general meeting (AGM), SPG is requesting approval to repurchase up to 10% of its shares. That said, the current free float limits what it can realistically buy back.

In the medium term, if BC Partners continues to exit and the free float rises, buybacks could become a more practical and significant way to return excess cash.

Why is CFO departing?

Orderly handover. On 1 Apr 2026, SPG announced Alexandra Dambeck has decided to step down from her role as the Chief Financial Officer (CFO) of SPG.2

The departure is amicable. The CFO is leaving to pursue a new external opportunity in a larger role. Alexandra played an important role through SPG’s IPO and has built a strong finance team to support a smooth transition.

Search is underway. The company is already looking for a successor. SPG is an attractive business, and management is confident of getting strong candidates.

The CFO plans to leave in Q4’26 and remains involved in key projects, which should give the company time to manage a stable handover.

What do investors typically misunderstand?

SPG is more AI-resistant than many assume. SPG’s core value proposition is in assisting the creation, verification and dissemination of new knowledge. Many analysts and shareholders already know this.

However, investors who are new to SPG may view the business like any other software or media businesses. Indeed, some peers may be more exposed, especially when their products rely on publicly available content.

Unless AI reaches the same level of intellect as Nobel Prize winners, it’s hard to imagine the business being disrupted by AI. If disruption happens, it will mean computers have become more sentient and intelligent than humans. There won’t be any investors left at that point.

Anyone who looks closely at SPG’s business will struggle to make a strong AI-disruption thesis. (Angsana Anderson’s note: I agree. That’s essentially why I became a shareholder.)

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I am a shareholder of SPG. I may change my views, predictions, or personal portfolio positioning at any time without notice.