SISB: Why I see an opportunity in Thailand’s largest international school

[Thesis] SISB Public Company Limited (SISB TB)

About (18 Apr 2026)

Share price: THB 10.40

Market capitalisation: THB 9,776 mn (USD 307 mn)

Enterprise value (EV): THB 8,257 mn (USD 259 mn)

Average daily volume (ADV): THB 43 mn (USD 1.4 mn)

NTM P/E: 11x

My Decision

I decided to become a shareholder of SISB.

I plan to buy my shares at around THB 10.40. Within 3 to 5 years, I expect to sell my shares for at least THB 20.00.

Over 3 years, I expect to earn ~29% p.a. (24% capital gains; 5% dividend yield). Over 5 years, I expect to earn ~19% p.a. (14% capital gains; 5% dividend yield).

Background

In 1992, a young Singaporean engineer moved to Thailand for work. He later took over the management of a fledgling school. By 2018, that school IPO’d on the Thai stock market. Within six years, the stock was up almost 10x.

The school is the Singapore International School of Bangkok (SISB), and that Singaporean is Kelvin Koh.

Today, it’s almost as if all that progress never happened. The stock is down more than 70% from its peak.

What happened? More importantly, is this an opportunity or a trap?

In this Substack post, I discuss why I see an opportunity in SISB now.

I will also argue why I believe the consensus has not fully recognised SISB’s growth prospects and the potential for higher capital returns.

Business model

SISB operates 6 international schools in Thailand. In 2025, it earned ~ THB 2,582 mn in revenue (+8% YoY). SISB earns most of its revenue from tuition fees in Thailand. Curriculum offered ranges from nursery/kindergarten to Grade 12.

Most customers are students aged between 2 and 18 years from high-income families. In Q4’25, there are 4,594 students enrolled in SISB (-1% YoY). 71% of students are local. Of the 29% of students that are foreigners, 72% are Chinese.

The largest expense is cost of education (35% of revenue). This consists mainly of remuneration for teaching staff.

SISB is the largest operator of international schools in Thailand. In Q4’25, SISB holds ~5.5% market share by number of students. The second player is Nord Anglia with 5.3% market share. It operates 3 premium British-style schools in Thailand. The third and fourth players are Shrewsbury (2.7%) and ISP (2.4%).

Most direct competitors like Nord Anglia and Shrewsbury are private. There are few public comparables of similar size. The relevant public comparables of similar size include China Education Group Holdings Limited (839 HK) and MegaStudyEdu Co. Ltd (215200 KS).

International school enrolments in Thailand are rising because more Thai and expatriate families want English‑medium, globally recognised curricula and university pathways. Average revenue per student (ARPS) outpaces inflation. International schools tend to enjoy strong pricing power, supported by high switching costs and the perception of superior educational quality.

SISB is controlled by its Singapore‑Thai co‑founders, CEO Kelvin Koh and deputy CEO Wilawan Kaewkanokvijit. Together, they hold more than 50% of SISB.

Institutions remain a small presence and the general public holds most of the free float.

My reasons

Under-recognised growth.

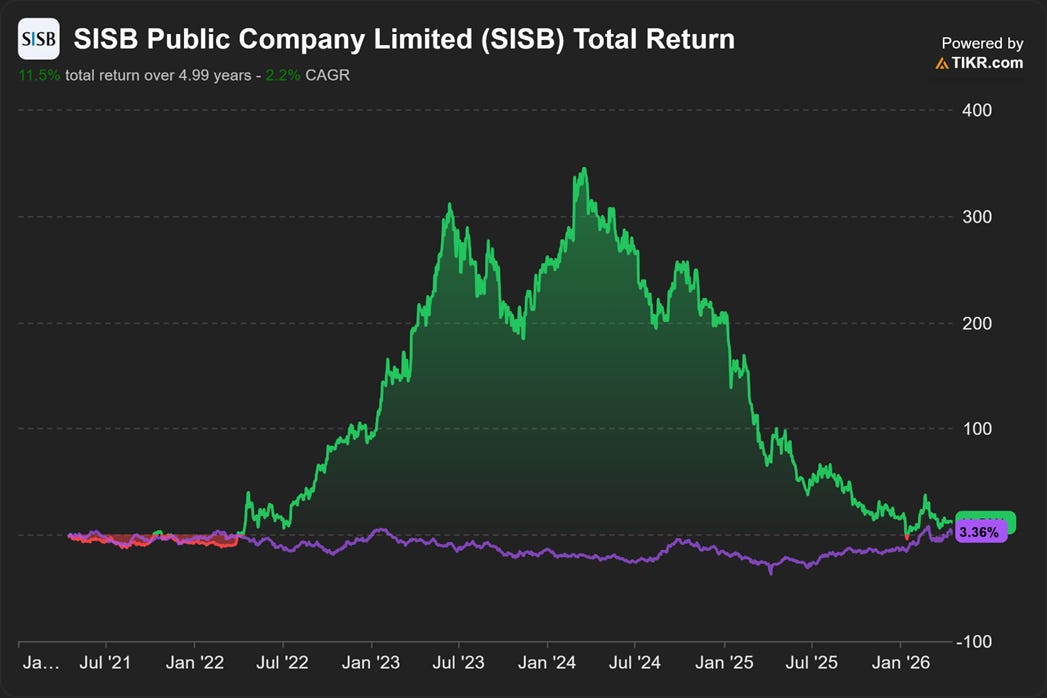

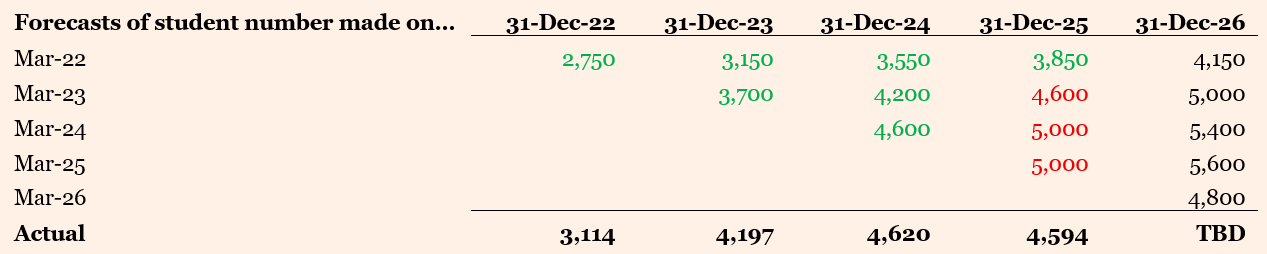

Share price driven by expectations over student numbers. SISB's share price today is roughly where it was five years ago, as though the intervening rally and collapse never occurred.

The rally started around Mar 2022 after SISB forecasted huge growth in student numbers. The rally continued through mid-2024 as student numbers exceeded expectations and SISB upgraded its forecasts.

Source: SISB

From mid-2024, the rally fizzled and collapsed. Even though SISB maintained its forecasts for 2025 and even upgraded its 2026 forecasts, this was not enough in the face of sky-high expectations.

The collapse intensified around Q1’25 as SISB disclosed actual student numbers in 2024 barely met forecasts. SISB’s share price continued sliding as actual student numbers in 2025 missed forecasts and SISB started downgrading forecasts for 2026.

At its peak, SISB was trading at 49x NTM P/E. Today, it is trading at only 11x, near an all-time low.

SISB currently trades at an FCFF yield of ~10% on enterprise value (EV), implying an attractive premium of ~8 ppt over Thailand 10y government bond yield.

The consensus seems to be expecting flat or declining student numbers. Student enrolment declined by -1% in 2025. The consensus seems to be extrapolating this decline and is expecting another decline, or at best, flat student numbers in 2026. After all, Thailand’s fertility rate is declining and the population has been shrinking since 2021.

Is the consensus’ expectation appropriate?

I believe the answer is no.

Fewer children, more spending. Declining fertility rate is actually good for SISB. Thai parents have less children, but they are spending more on education per child. This reflects the trends seen in other Asian countries like South Korea.1

In the past 10 years, private school student numbers (excluding international school) declined -1% p.a.2 I estimate public school student numbers likely declined low-single-digit p.a. over the same period too. In contrast, student numbers in international schools grew +6% p.a. YoY.

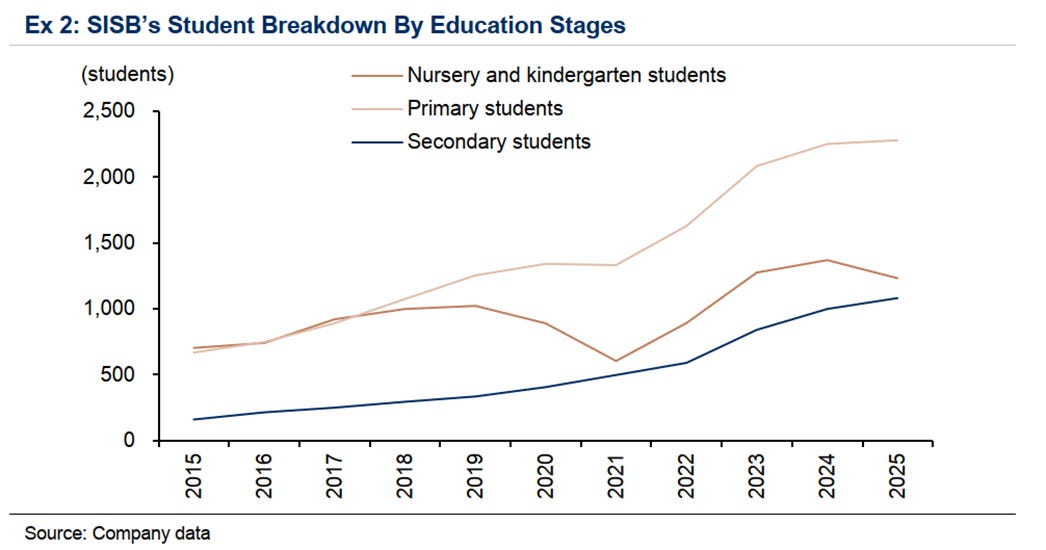

SISB’s student numbers reflect this tailwind. Despite the economic headwinds, the total primary and secondary student numbers grew +3% YoY in 2025. The headline student number declined -1% because nursery and kindergarten enrolment declined -10%.

As the graph below shows, this segment is more sensitive to economic fluctuations because it is non-compulsory early childhood education.

Source: ttb wealth securities (2026)

By focusing on the short-term deceleration in headline student numbers, the consensus is likely underestimating SISB’s growth potential.

International school is growing in Thailand, but it remains underpenetrated. Rising income and desire for better education doubled the penetration rate of international schools from ~0.4% in 2014 to ~0.8% by 2025.

Despite strong growth, Thailand’s penetration rate of 0.8% is still far below Malaysia at ~2.0%. I estimate the penetration rate of international schools in Malaysia increased from ~1.0% ten years ago to ~2.0% today.

It is reasonable to expect Thailand to follow Malaysia’s path because the markets are similar. Both are driven by local demand for higher quality and international education. Locals make up ~67% of students in Malaysia’s international schools. In Thailand, this is ~50%.

To capture more growth, SISB is expanding. SISB will open its 7th campus at Rangsit in Aug 2027. SISB is targeting an initial enrollment of 200 to 250 students for the campus’s first academic year, which aligns with the school’s breakeven point. This is projected to double to 400 students by the 2028 academic year.

The growth from SISB’s new Rangsit campus carries higher certainty because it is embedded in a residential development by Supalai, one of Thailand’s largest residential developers. This allows SISB to tap into the roughly 600 families that will live there, rather than relying on a standalone greenfield location.

ARPS uplift as student base matures. Besides volume growth, I also see higher average revenue per student (ARPS) contributing to revenue growth.

Most SISB students are currently in primary school (especially Primary 1–4), where annual tuition is about THB 500k–600k. In contrast, secondary school fees range from roughly THB 700k to THB 900k per year.

As SISB anticipates most of these primary students will continue into its secondary school, ARPS should rise even without any explicit price increases, simply from the cohort mix shifting into higher‑fee grades.

Capital returns

SISB will likely increase capital returns as capex declines. Historically, capital returns were constrained because SISB was building out multiple new campuses within a short time. Cash capex peaked at THB 698 mn in 2023.

In 2025, cash capex has fallen to ~ THB 335 mn. SISB’s campus development plan suggests the rapid and intense build-up phase is likely over. Reflecting this, dividends nearly doubled in 2024, with the payout ratio rising from 23% in 2023 to 33% in 2024.

SISB increased its dividends again in 2025. Dividends rose by +36%, corresponding to a higher dividend payout ratio of 41%.

With lower capex needs ahead, there is a strong likelihood that SISB will return more capital to shareholders.

Favourable working capital structure supports higher dividend payout ratio. SISB targets an annual dividend payout ratio of at least 40%. I believe SISB can increase this payout ratio because of its negative working capital.

In 2025, SISB enjoyed a cash inflow of THB 84 mn (~10% of free cash flow to firm). Students pay their tuition fee in advance, usually one or two months before each school term. They also pay a deposit when they enrol.

Cash pile. SISB can return more capital to shareholders. As of 31 Dec 2025, it holds cash and cash equivalents that are ~ 81% of revenue.

Without more capital returns, the cash will continue to pile up. This will be an area I will focus on when I meet investor relations.

Valuation

I estimate intrinsic value at THB 20.00 per share based on a discounted cash flow valuation.

The current share price of THB 10.40 implies 48% margin of safety and 93% upside. This looks very attractive to me.

On a near‑term earnings basis, SISB trades at 11x NTM P/E on consensus forecasts and 9x on my estimates.

At my intrinsic value estimate, SISB would trade at 18x NTM P/E.

Since its IPO, SISB has traded at an average NTM P/E of 35x. Given the higher penetration of international schools in Thailand now, and the weaker investor sentiment, I do not believe SISB can trade at such elevated levels again.

That said, I believe SISB should trade above 15x, the average P/E ratio in Thailand, because of its under-recognised growth, potential for higher returns and high free cash flow conversion.

That’s why I see 18x NTM P/E as reasonable.

Catalysts

Student numbers return to growth in the next 3 to 5 years, driven by

Increasing penetration rate of international schools in Thailand

The opening of SISB’s new Rangsit campus in Aug 2027

Higher capital returns

Risks

What if student number continues to fall?

This risk seems low. My analysis of working capital trends suggest short-term demand looks stable and better than consensus’ expectation.

Advance tuition fee collected for term 2 increased +1% in 2025. Term 2 runs from Jan 2026 to Apr 2026.

As of 31 Dec 2025, SISB collected 10% more deposits from students. Deposits are collected when SISB offers a place to a new student.

Exposure to foreign Chinese students?

In my shortlist of SISB, I explained there is a perception that SISB is overly reliant on foreign Chinese students3, particularly those who enrolled mainly to leave China rather than out of a strong preference for the school. This creates a risk that many could withdraw if their families leave Thailand.

However, this risk currently appears limited.

Foreign Chinese students make up only ~21% of all students in 2025. For the past 3 years, this percentage has been stable at around low-20%. In Q4’25, the number of foreign Chinese students increased +1.2% QoQ.

What if the government removes tax exemption for private schools?

SISB pays almost no corporate tax because Thai law grants a corporate tax exemption on profits from operating licensed private schools-

While Thailand could amend or revoke the tax exemption relatively easily, this would represent a clear reversal of long-standing policy to promote private education through tax incentives. It would directly raise costs for a visible sector, likely triggering pushbacks from concerned parents and operators.

When SISB IPO’d in 2018, various politicians including the-then Minister for Education proposed that SISB should no longer enjoy the tax exemption.4

However, the proposal failed to get enough support among important players like the Ministry of Finance, Securities and Exchange Commission (SEC) and the Stock Exchange of Thailand (SET).5 The controversy has since died down.

Poor reputation among employees?

SISB attracted numerous negative online reviews, apparently by former and current employees.

For example, this Reddit post urges teachers to avoid SISB.6 The poster expressed serious dissatisfaction with management styles and workload.

However, there are also positive reviews. This post by a current SISB teacher expresses surprise over the school’s bad reputation online because their own experience has been very positive.7

In the comments, many users speculate online reviews skew negative because unhappy teachers are more likely to post, and experiences can vary widely by campus, immediate leadership, timing, and a teacher’s previous school.

Employee turnover at SISB declined from 12% in 2023 to 10% in 2025. 10% looks healthy and contrary to the negative reviews online. The average turnover rate in the industry seems to be between 10% to 20%.8

Factors that could lead me to increase investment in SISB

Evidence that revenue growth can be sustained above high-single digit for the foreseeable future (e.g. demand for SISB’s new campus at Rangsit is higher than expected)

Share price falls > 20% without significant deterioration in business fundamentals

Factors that could lead me to decrease investment in SISB

Student numbers decline materially versus expectations without a credible explanation

Adverse regulation against private schools in Thailand

Upcoming events

Wed 13 May 2026: Q1’26 earnings release (expected)

Valuation model

Subscribers may request a free copy of my valuation model by emailing me at angsana.anderson@gmail.com.

Coming up next

In Q4’25, Chagee CHA 0.00%↑ slipped into operating losses.

My next post digs into what changed since my first-take on Chagee and what the latest numbers are really telling us.

I will highlight the warning signs brewing behind the headlines.

I will also spill the tea on the insights I gathered from visiting the Chagee store in Orchard, Singapore’s busiest shopping district.

Subscribers get it first. Free to join.

Subscribe for 2 to 3 analyses of global equities every week. Discover overlooked ideas and rethink familiar names. Published by Andrew Wong, ACA, CFA

Disclaimer

This is a record of my investment decisions, not financial advice. I may change my decisions without notice. Use this only for education and entertainment. All analysis and opinions expressed are solely my own, and SISB has not reviewed or endorsed this post. Do not rely on this for your investment decisions. I plan to buy shares in SISB.

Well written - clearly articulated with risk clarified. One of the issues which is a key for the long term for them is the ability to move their students from Primay to Secondary/Tertiary - there is too much churn as parents move kids to British/Western oriented private schools after a strong foundation in Singapore education.

Thanks for introducing this business. I do like the set up. Through which brokerage did you invest? I have IBKR and it doesn't allow Thai stocks