Sido Muncul: 11% FCF yield. But 49% of revenue from related parties?

[Shortlist] PT Industri Jamu dan Farmasi Sido Muncul Tbk (SIDO IJ)

Summary

I shortlisted SIDO, one of the top makers of herbal medicine in Indonesia.

Investors may be under-estimating its growth potential, particularly in international markets.

SIDO seems to be a good business. It is reinvesting capital at higher rates of return, as evidenced by its superior and growing return on assets (ROA).

Recent revenue decline seems to be a temporary headwind, driven by management’s decision to reduce channel inventory rather than a structural problem.

On that basis, SIDO’s 11% free cash flow yield seems sustainable and attractive.

That said, now may not be the best time to invest. Working capital trends suggest consensus remains too optimistic over near-term demand.

Although related parties contributed to only 29% of group revenue in Q1’26, it has averaged ~50% historically. I will need to investigate why, and whether this risk is too big.

I am not too concerned over macroeconomic risks. These can be managed through diversification or shorting of an Indonesia index ETF.

About (15 Jun 2026)

Share price: IDR 380

Market capitalisation: IDR 11,185 bn (USD 632 mn)

Enterprise value (EV): IDR 10,417 bn (USD 588 mn)

Average daily volume (ADV): IDR 8.7 bn (USD 0.5 mn)

NTM P/E: 9x

Time spent: ~1 day

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Shortlist

Background

Are investors wrong about Indonesia’s top herbal medicine?

PT Industri Jamu Dan Farmasi Sido Muncul Tbk (SIDO IJ) makes Tolak Angin, Indonesia’s most popular herbal medicine with ~72% market share.

At first glance, Sido Muncul is a lousy business. Revenue declined -19% in Q1’26. Its share price has fallen -30% in 2026.

However, investors are likely under-estimating the company’s growth potential.

Its headwinds are likely temporary.

Furthermore, the company also offers double digit free cash flow yield.

Business model

SIDO is an Indonesian company that manufactures and sells herbal supplements, food and beverages and pharmaceutical products.

Breakdown of 2025 revenue (IDR 4,080 bn; +4% YoY):

61% Herbal Medicine & Supplements (+0% YoY)

36% Food & Beverages (+12% YoY)

3% Pharmaceutical (+1% YoY)

The Herbal Medicine & Supplements segment manufactures health products such as Tolak Angin, Indonesia’s most popular jamu. Jamu is a traditional herbal medicine made from turmeric, ginger and other herbs used to boost immunity and relieve inflammation.

The Food & Beverages segment manufactures ginger coffee, ginger tea, energy drinks, etc. Brands include Kuku Bima Ener‑G and Alang Sari Cool.

The Pharmaceutical segment focuses on the production and distribution of various health products under the Berlico brand. These products include Anacetine, Berlosid, Anabion, Minyak Telon Cap Tiga Anak, and a variety of other products.

Most herbs and spices appear to be sourced from farmers across Indonesia, which implies a fragmented base of small and mid‑size agricultural suppliers.

Main customers are distributors across Indonesia. There are no individual customers that contributed > 10% of revenue in 2025.

SIDO earns 91% of its revenue from Indonesia. The remaining ~9% comes from international markets like Malaysia, Philippines and Nigeria.

According to management, Tolak Angin holds ~72% market share. The next closest competitors hold ~23% and 5%.

The most relevant public comparable is PT Kalbe Farma Tbk. (KLBF IJ).

Both SIDO and KLBF sell herbal medicine and supplements in Indonesia, but KLBF is a far larger, diversified pharma‑healthcare conglomerate while SIDO remains a focused herbal and FMCG player.

My reasons

Under-recognised growth?

Exports are growing fast. Since disclosure started in 2022, international revenue has grown 33% p.a. and reached 9% of overall revenue in 2025. During the same period, overall revenue increased by only 2% p.a.

Malaysia and Nigeria contributed 2% and 4% to overall revenue respectively.

There are precedents for Indonesian products to penetrate these markets. For example, Indonesia’s Indomie has captured ~74% of the market in Nigeria.1 Like Indonesia, both markets have significant Muslim population.

Good business, temporary headwinds?

Revenue declined in Q1’26. When SIDO released earnings on 8 May 2026, its share price started collapsing faster than the broader market.

SIDO’s revenue declined -19% YoY in Q1’26. This was unexpected, given management’s target of 5% to 8% revenue growth for 2026.

Headwind likely temporary. Management explained they deliberately restricted sales after discovering that channel inventory had accumulated to as much as two to three months’ supply.2

SIDO is targeting inventory levels of ~ 14 days for distributors in Java and ~ 21 days for areas outside Java.

Despite that, management reports consumer demand has not weakened. They believe sell-in remains healthy.

That’s why even though it no longer believes 5% to 8% revenue growth is achievable, SIDO is still targeting stable revenue in 2026.

Good business. Despite the headwinds, SIDO appears to be a good business.

Its flagship product, Tolak Angin, is priced at ~20% to 50% premium over competitors. Despite that, it still holds 72% market share in Indonesia.3

SIDO is reinvesting incremental capital to earn higher returns. Between 2016 and 2025, it improved its ROA from 13% to 25%. SIDO’s 25% ROA is significantly higher than the 10% earned by its domestic peer, KLBF.

Capital returns?

SIDO is generating cash. SIDO generated ~ IDR 1,177 bn of free cash flow to firm (FCFF) in the last twelve months (LTM).

Against today’s enterprise value (EV), SIDO is offering ~11% FCFF yield. This is a decent 4 percentage points (ppt) premium over Indonesia 10y government bond.

And returning cash to shareholders. Management demonstrated a good track record of returning excess capital to shareholders and not hoarding cash.

In 2016, cash was ~39% of revenue. By 2025, management had reduced it to a more reasonable 11% of revenue.

This was achieved mainly through a high dividend payout ratio. Management also started significant share buybacks in 2025, resulting in ~ IDR 1,600 bn capital return to shareholders in that year alone.

Catalysts

Potential sale. In Jan 2026, Bloomberg reported that the Hidayat family, SIDO’s controlling shareholders and management are open to bringing in a strategic investor to take the business “to a higher level”.

The family is in talks with banks. A transaction could value SIDO at ~ USD 1 bn, +70% higher than the current enterprise value.4

Factors to focus on

Timing of channel destocking. Even though SIDO looks like a great business, now may not be the best time to invest. The consensus still seems too optimistic.

According to Tikr, the consensus is expecting ~+2% revenue growth in 2026. This is more or less in line with management’s guidance of stable revenue.

If SIDO is to achieve this, it must grow revenue by +7% YoY in the remaining 3 quarters of 2026.

This seems too optimistic. Working capital trend suggests demand from distributors has not bottomed out.

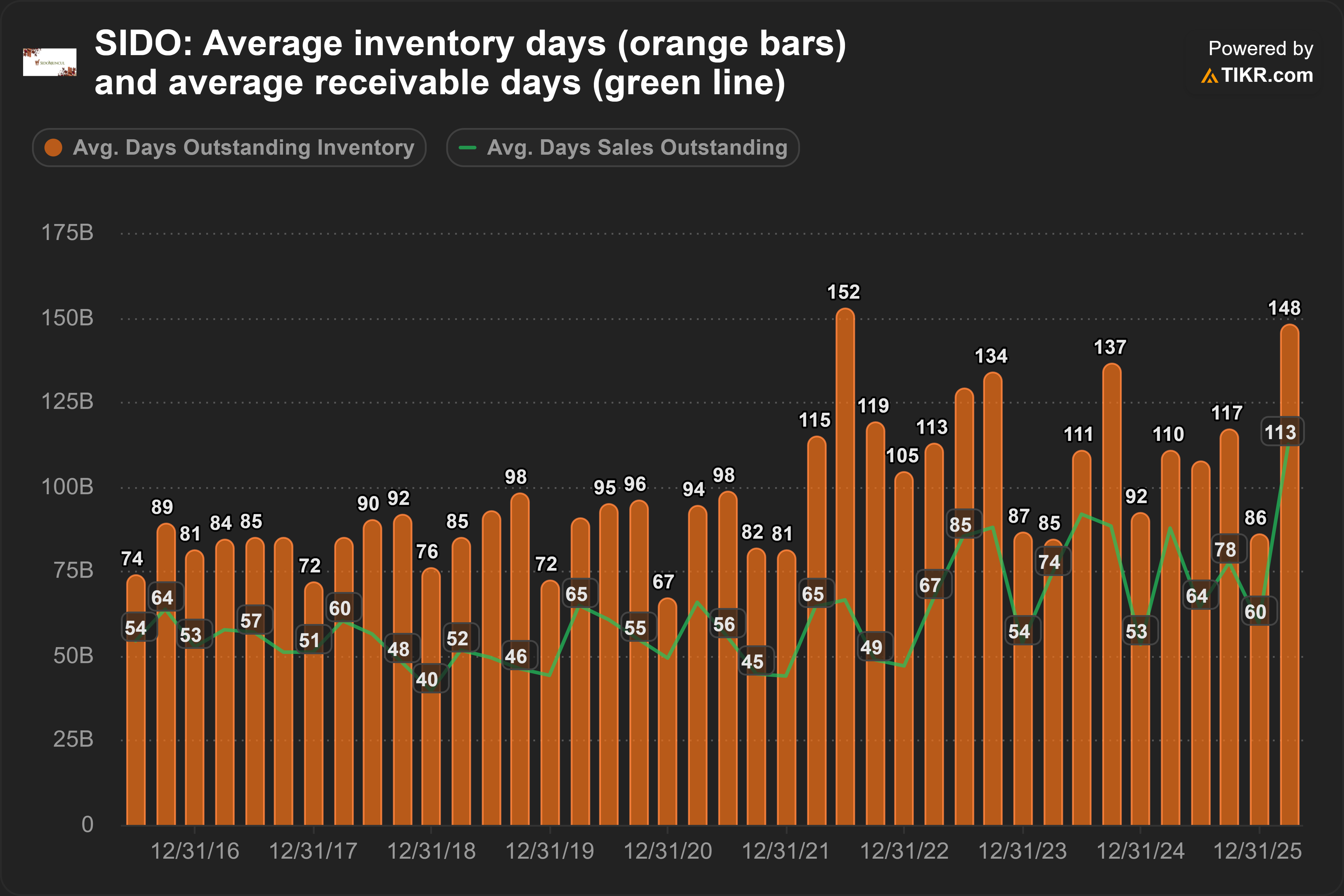

In Q1’26, receivable and inventory days reached new highs and are not showing signs of peaking yet:

Furthermore, the % of current receivables declined from 64% in Q1’25 to 50% in Q1’26.

Despite revenue falling in Q1’26, inventory increased +17% YoY, with most of the increase concentrated on finished goods and work-in-progress.

With customers delaying payments and inventory piling up, near-term demand looks likely to be much weaker than consensus expects.

I will be monitoring the working capital trends over the next few quarters. When there are signs of inventory and receivable days peaking, that may be a better time to invest.

Significant related party transactions. In Q1’26, sales to related parties declined -43% YoY, significantly contributing to the -19% YoY decline in overall revenue.

During the quarter, sales to related parties contributed to 29% of revenue, down from 42% in Q1’25 and 49% in 2025.

The major related parties appear to be distributors owned by the Hidayat family, SIDO’s controlling shareholders and management.

Is such high concentration of related party transactions normal in Indonesia? What is the business rationale?

Are the transactions conducted on an arms-length basis?

Given such high % of sales from related parties, why didn’t SIDO foresee the -19% revenue decline in Q1’26?

Macroeconomic volatility. The Jakarta Composite Index (JCI), an index of Indonesian stocks, fell -28% in 2026. The IDR has depreciated -6% against the USD.

Such volatility is mainly driven by concerns over increasingly populist and interventionist government policies.5

It is difficult to predict the direction of government policies.

In any case, I don’t have to bet on macroeconomic factors. If SIDO is indeed attractive, I can manage the macroeconomic risks through diversification or shorting the JCI.

Coming up next

PayPal Holdings, Inc. (PYPL US) has fallen -85% from its peak in Jul 2021.

It is now trading at only 7.8x NTM P/E, an all-time low. Historical average was ~ 27x.

Since Feb 2026, Stripe is said to be interested in acquiring PYPL 0.00%↑ .

Is there an opportunity?

I will explore this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in SIDO, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.