[Shortlist] Springer Nature AG & Co. KGaA (SPG; SPG GR)

I shortlisted SPG because of (a) under-recognised growth and (b) a high probability of higher dividends

Disclaimer: This is a record of my investment decisions, not financial advice. I may change my decisions without notice. Use this only for education and entertainment. All analysis and opinions expressed are solely my own, and SPG has not reviewed or endorsed this post. Do not rely on this for your investment decisions.

About

Share price: EUR 15.06

Market capitalisation: EUR 2,995 mn (USD 3,460 mn)

Enterprise value (EV): EUR 4,346 mn (USD 5,021 mn)

Average daily volume (ADV): EUR 600 k (USD 692 k)

NTM P/E: 10x

Time spent: ~5 hours

My decision

Shortlist

Background

Springer Nature is not software.

Springer Nature AG & Co. KGaA (SPG; SPG GR) sold off -24% year-to-date amind the ‘SaaSpocalypse’. However, the market is probably wrong.

SPG is not software. SPG is a brand. It owns Nature, one of the most prestigious scientific journals in the world. Nature is to science what Hermès is to fashion.

I shortlisted SPG because of (a) under-recognised growth and (b) a high probability of higher dividends.

In this Substack post, I walk through these 2 factors in detail. I also discuss what I will focus on as I investigate further.

To receive updates, click on the link below and subscribe to my Substack.

Business model

Breakdown of 2024 revenue (EUR 1,847 mn, -0.3% YoY):

77% from Research (+3.1% YoY)

10% from Health (-0.3% YoY)

13% from Education & Professional (-3.4% YoY)

Research revenue mainly comes from long‑term institutional subscriptions and transformative agreements for journals and eBooks, complemented by open‑access publishing fees and a smaller share from books and research‑support services.

The Health segment earns revenue from clinical publishing, pharma marketing services, and medical education for healthcare professionals.

Education earns revenue mostly from selling school and language-learning materials while Professional earns revenue from specialist publications, digital tools and industry events for European professionals.

SPG earns ~40% of its revenue from Europe, Middle East and Africa (EMEA), 32% of its revenue from Americas and the remaining 27% from Asia Pacific.

Most of its Research revenue is under contract like subscriptions (62%). The remaining 38% Research revenue is transactional.

SPG is diversified, with no single customer dominant. In the Research segment, the top 50 customers account for only about 56% of subscription revenue, and overall revenue is spread across thousands of institutions worldwide.

The largest expense is personnel costs (36% of revenue). This mainly consists of wages and salaries for its 9,200 employees across editorial, technology/product, sales and marketing, and corporate/operations roles.

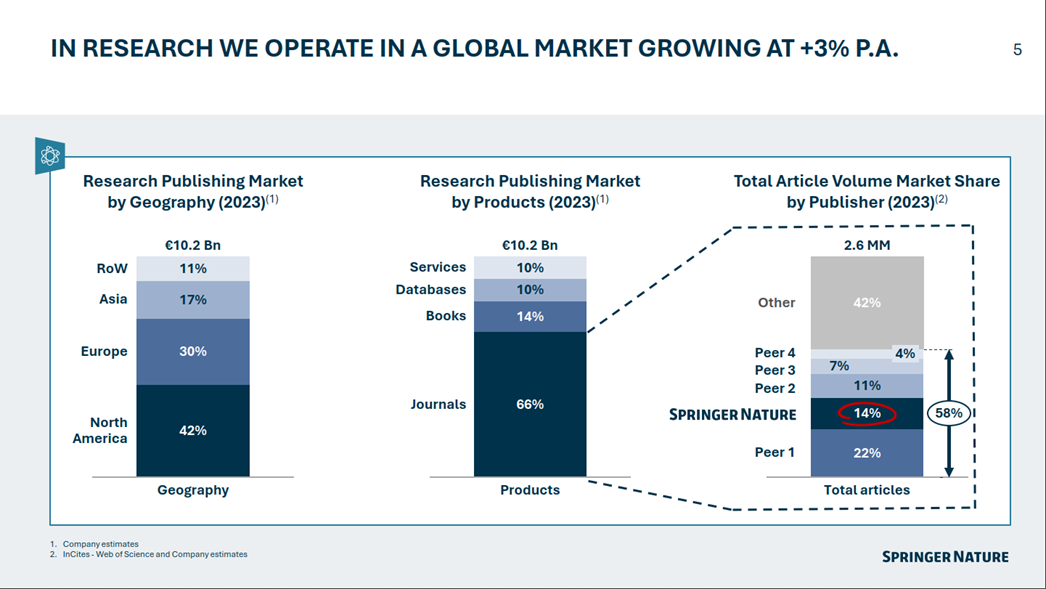

In 2023, SPG estimated it holds ~14% market share by article volume in the Research journal publishing market. This makes SPG the second largest publisher in the world.

Source: Springer Nature (2025)

According to Scilit, an online index of research publications, SPG remains the second largest publisher in the world so far in 2026. SPG has even supplanted Elsevier as the largest publisher of open access articles.

Source: Scilit Rankings (2026)

Relevant public comparables include RELX PLC (REL; REL LN), John Wiley & Sons, Inc. (WLY; WLY US), Informa plc (INF; INF LN) and Wolters Kluwer N.V. (WKL; WKL NA).

REL owns Elsevier, WLY owns Wiley, INF owns Taylor & Francis while WKL owns Wolters Kluwer Health.

My reasons

Under-recognised growth? The market seems to be trading SPG like it is a software company.

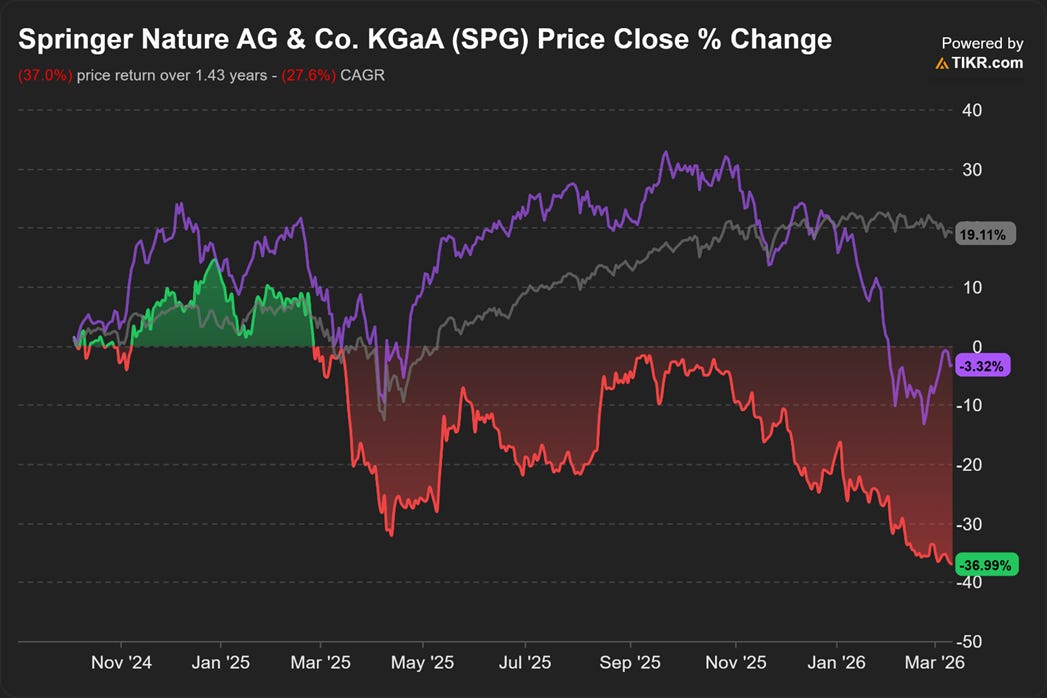

In figure 1 below, I plot the % change in the price of SPG (green) against the price of IGV (purple). IGV is one of the largest ETF tracking North American software stocks. I also provided SPY, an ETF tracking the S&P 500 index, as a baseline (grey).

Source: Tikr

SPG and IGV are generally correlated. Since Jan 2026, “SaaSpocalypse” sparked a sharp sell-off of software stocks. SPG sold off sharply too.

SPG delivers ~88% of its research digitally and 62% of its Research revenue is derived from contracts like subscriptions. However, this is where the similarities with software companies end.

SPG is not a software company. SPG is a brand.

Customers (such as academic libraries) choose SPG because of the quality and prestige of its journals. SPG’s flagship journal is Nature, which publishes many important breakthroughs and has featured work by more than half of Nobel laureates in medicine, physics, and chemistry. It is also among the most cited journals worldwide.

For this reason, researchers choose SPG. For them to be fully recognised as experts in their fields, publication in many of SPG’s journals is often seen as a prerequisite. At some universities, having articles in SPG journals is considered almost essential for achieving tenure over the long run.

Generative artificial intelligence (gen. AI) can help researchers produce better research. Given that gen. AI is trained on historical data, I doubt it can replace researchers in pushing the frontier of knowledge. Even if this happens, it won’t change the fact that SPG’s value lies in its branding and reputation, not software capabilities.

Yet the market is not fully recognising SPG’s ability to sustain or even accelerate its growth. The market seems to be pricing SPG like a software company facing existential threat from gen. AI. SPG currently trades at 10.4x NTM consensus EPS. On my initial estimate of sustainable free cash flow to firm, SPG is trading at ~8% yield on enterprise value. This is an attractive 5% premium over Germany 10y government bond yield.

Capital returns? I believe there is a very good chance that SPG will increase dividends.

For 2024, SPG declared and paid a cash dividend of EUR 0.13 per share. The yield on current share price is ~0.9%. It looks very low.

In its 2024 IPO prospectus, SPG stated it intends to pay an annual dividend in an amount of ~50% of its adjusted net income1. Adjusted net income refers to SPG’s net result for the period before gains/losses from the acquisition/disposal of business/investments, amortization/depreciation and impairment on acquisition related assets and exceptional items.

Fitch expects dividends of EUR 25 mn in 2025 (~0.8% dividend yield), increasing to EUR 175 mn in 2026 (~5.8% yield) and reaching EUR 213 mn in 2027 (7.1% yield)2. If these estimates are realised, then by 2027, SPG’s dividends will be offering an attractive 4% premium over Germany 10y government bond.

I believe the probability of this happening is more likely than not. In 2024, SPG reached its leverage target. By Oct 2025, SPG has received an investment grade rating from Fitch. The business is very capital light. Beyond offices, not much capex is required. Working capital is a source of cash because customers pay in advance for subscriptions.

Factors to focus on

How will the shift towards open access impact SPG? Traditionally, libraries and institutions pay publishers for access to journals. Academia is shifting towards open access publication. In this model, the journals are free to read online. The publisher is instead paid upfront by the author’s funder or institution. This is typically via an article processing charge, or APC.

At first glance, this shift is slightly positive or neutral for SPG. Volume should grow faster because more papers can be published. However, it could also mean more volatile revenue as SPG becomes more exposed to research funding cycles. ~27% of SPG’s Research revenue is derived from open access articles.

I would like to gather more data to get a deeper understanding of the shift and its implications.

Private equity ownership. BC Partners, a European private equity (PE) firm is the second largest shareholder (~35% shareholding). There is a risk of prolonged undervaluation as the market anticipates discounted block selldowns. How significant is the risk of PE overhang?

Risk from paper mills. In 2024, WLY suffered major reputational damage, journal closures, and USD 35 to 40 mn of lost revenue after paper mills infiltrated its Hindawi open‑access journals3. What is the risk of a similar incident at SPG?

To receive updates on SPG, subscribe to my Substack

Update: I became a shareholder of Springer Nature AG & Co. KGaA (SPG; SPG GR) because of (a) under-recognised growth and (b) attractive capital returns.

For details, check out my thesis here: https://angsanaanderson.substack.com/p/thesis-springer-nature-ag-and-co?utm_campaign=post-expanded-share&utm_medium=web