PayPal: Undervalued at 7.8x P/E?

[Shortlist] PayPal Holdings, Inc. (PYPL US)

Summary

I shortlisted PYPL.

At 7.8x NTM P/E, PYPL is priced like a terminally declining business.

However, investors seem to be underestimating its growth potential in buy now, pay later (BNPL), Venmo and advertising.

Despite tremendous growth in recent years, BNPL value per active user remains significantly below industry average.

BNPL offers higher take-rates and increases transaction value. Unlike traditional lenders, PYPL sells most of its BNPL receivables. This allows it to grow without being constrained by BNPL’s capital intensity.

PYPL has significant room to monetise Venmo. Compared to peers like Revolut, Venmo’s product offerings are still limited.

UBER’s advertising unit is already generating USD 2 bn annual revenue. PYPL has more active users and deeper data, but its advertising revenue appears to be immaterial.

This is changing. In 2024, PYPL hired a senior executive from UBER’s advertising unit. In 2025, PYPL’s advertising unit started launching major products.

Catalyst: potential takeover by Stripe.

About (18 Jun 2026)

Share price: USD 42.51

Market capitalisation: USD 37,498 mn

Enterprise value (EV): USD 39,826 mn

Average daily volume (ADV): USD 665 mn

NTM P/E: 8x

Time spent: ~1 day

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Shortlist

Background

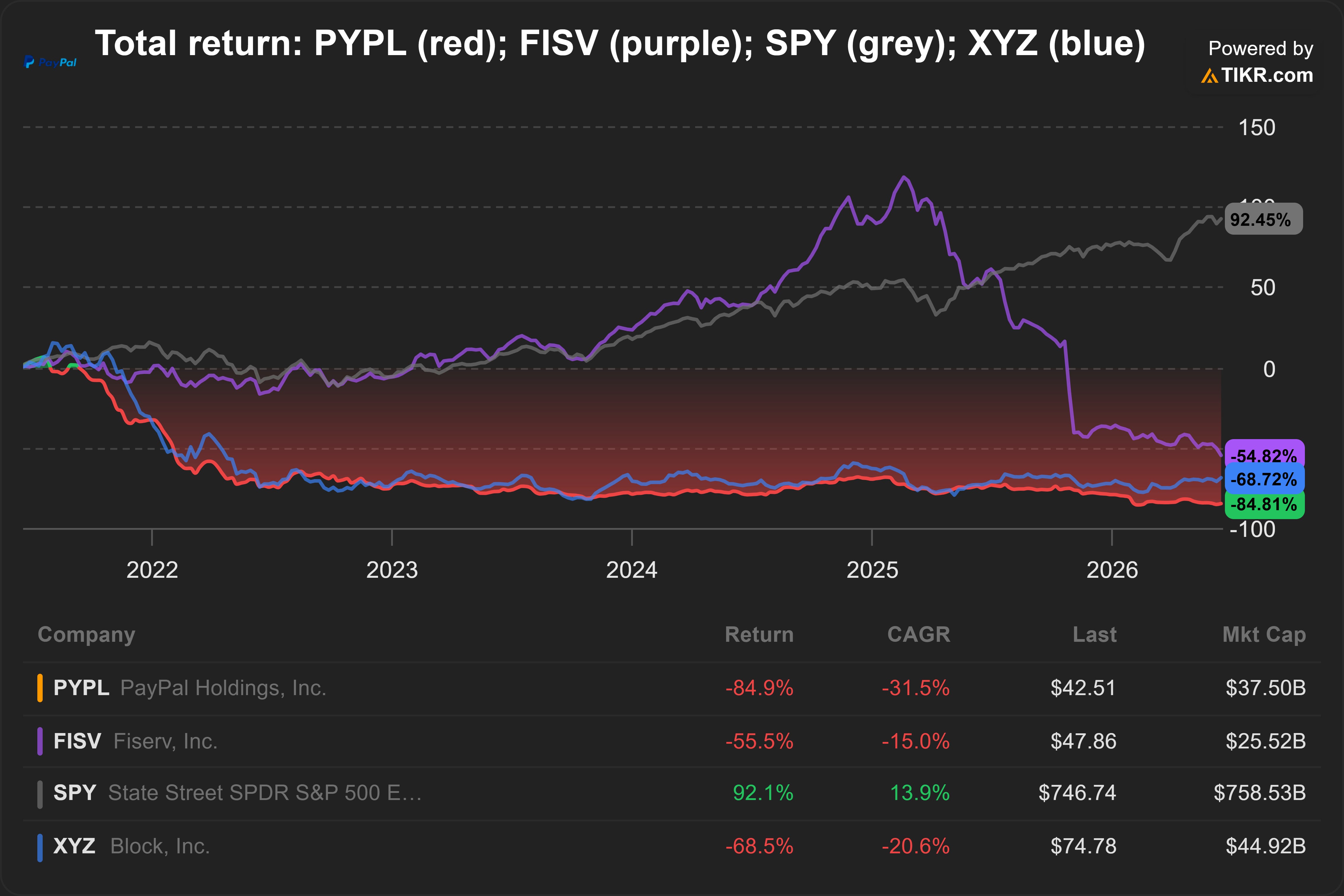

PayPal Holdings, Inc. (PYPL US) has fallen -85% from its peak in Jul 2021.

It is now trading at only 7.8x NTM P/E, an all-time low. Historical average was ~ 27x.

Since Feb 2026, Stripe is said to be interested in acquiring PYPL.

Is there an opportunity?

Business model

Breakdown of 2025 revenue (USD 33,172 mn; +4% YoY):

90% Transaction Revenue (+3% YoY)

10% Other Value-Added Services (OVAS) Revenue (+14% YoY)

Transaction revenue consists mainly of net transaction fees charged to merchants and consumers for transactions completed on PYPL’s payments platform.

OVAS revenue consists of interest and fees from consumer and merchant loans, revenue-sharing partnerships for branded credit cards, subscription fees, and the interest earned on underlying customer account balances.

Main customers consist of everyday consumers who use its digital wallets to shop and manage money, and merchants who rely on its payment processing tools to drive sales and run their businesses.

In 2025, no customers accounted for more than 10% of revenue or net loans receivable.

Main suppliers include payment card networks, partner banks and payment processors.

In 2025, two payment processors accounted for 56% of transaction expense. These are likely Mastercard Incorporated (MA 0.00%↑ US) and Visa Inc. (V 0.00%↑ US).

PYPL earns 57% of its revenue from US (+3% YoY) and 43% from the rest of the world (+6% YoY).

Block, Inc. (XYZ 0.00%↑ US) is the most relevant public comparable.

It owns Cash App, which directly competes with PYPL’s Venmo for P2P transfers, direct deposits, etc. In 2022, XYZ acquired Afterpay to integrate BNPL into its ecosystem.

Some analysts compare PYPL to payment processors like Fiserv, Inc. (FISV 0.00%↑ US). However, the total return chart above suggests legacy payment processors are driven by other factors. XYZ seems to be the best comparable.

For a detailed explanation of PYPL’s business model, I recommend Bob’s Payment Stock Substack’s PayPal: Past, Present and Future.

My reasons

Under-recognised growth?

BNPL is under-penetrated. In 2025, PYPL generated ~ USD 40 bn in BNPL transaction volume1 across its 227 mn monthly active accounts (MAUs)2.

Blended across its entire active user base, this equates to ~ USD 176 in BNPL volume per MAU. For context, the US industry average sits significantly higher at USD 848 per active BNPL user.3

This comparison is not perfect because PYPL’s denominator includes customers for whom BNPL may never be suitable.

That said, the sheer magnitude of this gap strongly suggests under-penetration of BNPL among PYPL’s user base.

BNPL increases take-rate and transaction value. PYPL’s take-rate for an ordinary payment is only 2.6%, on average. If the customer completes the transaction using BNPL, PYPL’s take-rate increases to 4.5%.

BNPL also increases transaction value. When customers pay using BNPL, their average order value is on average more than 80% higher.4

BNPL is capital-light. Lending money is capital intensive. That’s why MoneyMax Financial Services Ltd. (5WJ; MMFS SP), Singapore’s leading pawnbroker, issued more shares recently.5 Without the infusion of new capital, growth will probably stall.

PYPL does not face the same problem because it has forward flow arrangements under which it sells most of its BNPL receivables to third‑party investors such as KKR & Co. Inc. (KKR US).6

Venmo is under-monetised. Venmo is PYPL’s US digital wallet and mobile app. It is popular among younger, mobile‑first consumers, especially Millennials and Gen Z. In 2025, Venmo accounted for ~ 19% of PYPL’s total payment volume (TPV).7

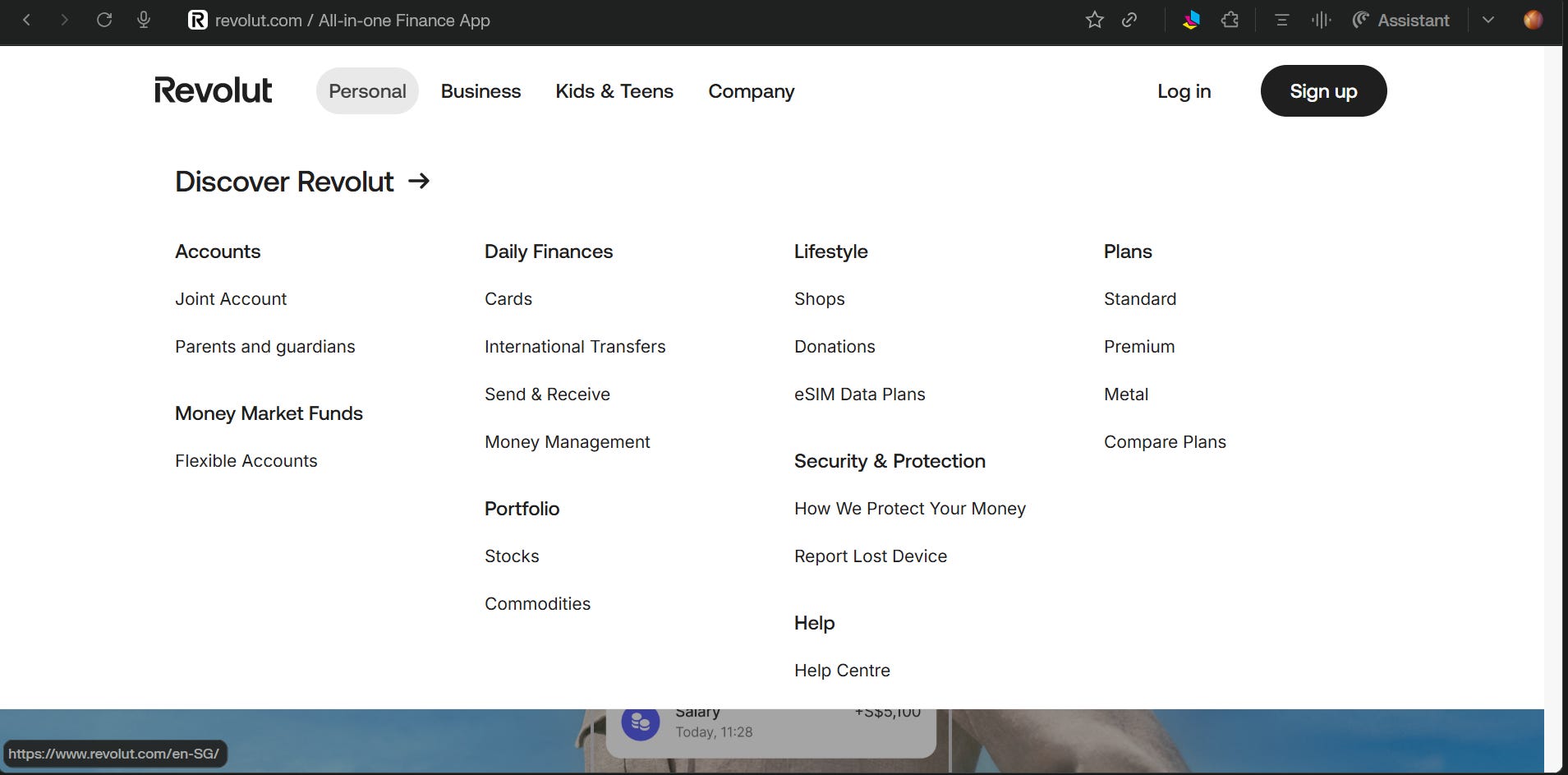

To show how under-monetised Venmo is, I’ve compared its product offerings against Revolut.

Revolut started in 2015 as a digital wallet. Today, it has evolved into a fully licensed digital bank and financial super-app.

Revolut monetises its users by charging subscription fees for premium perks like personalised cards, discounted airport lounge access, etc. It also distributes money market funds and offers stocks and commodities trading.

Source: Revolut (2026)

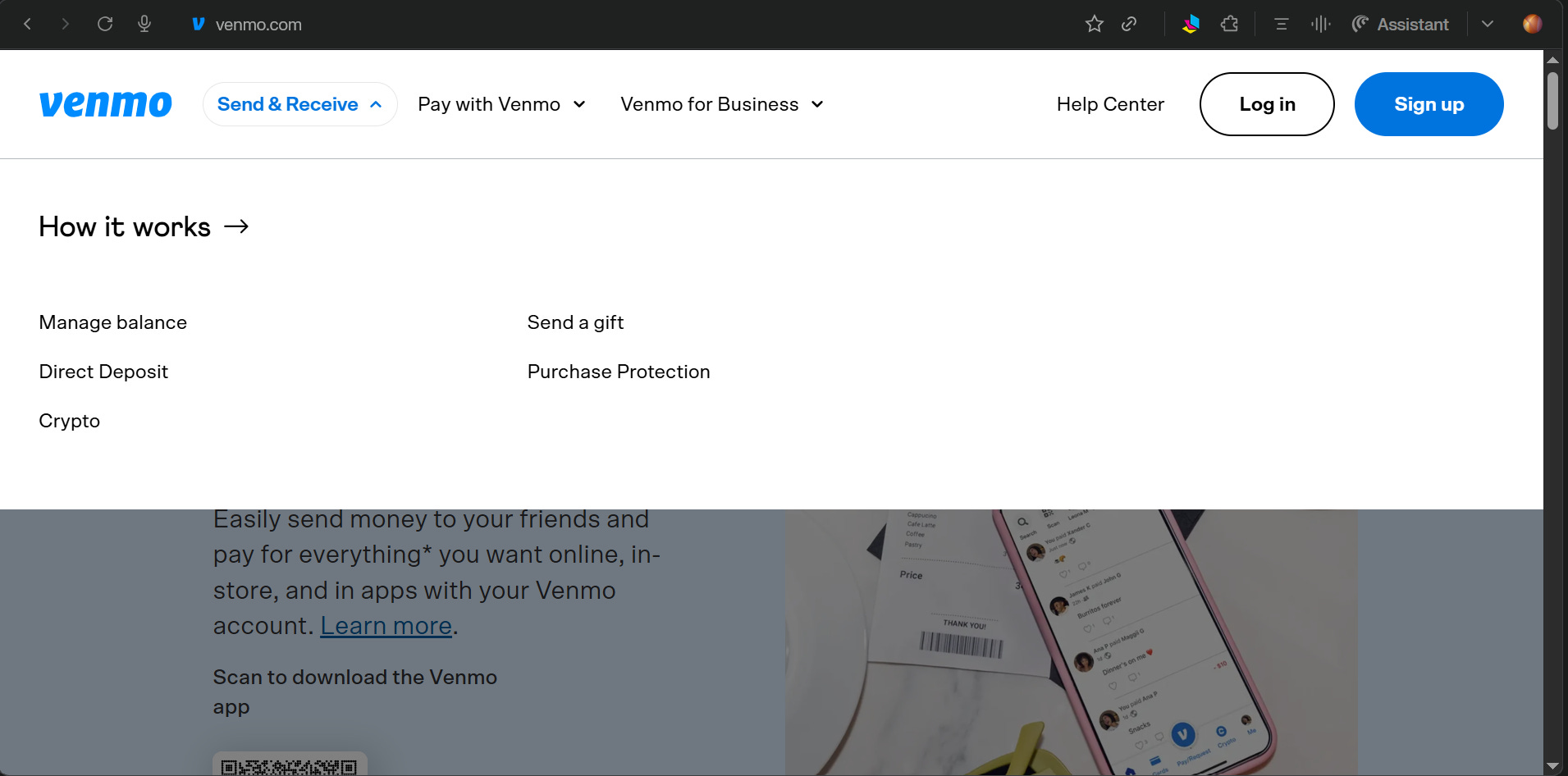

On the other hand, Venmo’s product offerings are sparse. It seems like Venmo does not even offer trading in stocks and ETFs.

Source: Venmo (2026)

Although Venmo is currently under-monetised, it also means growth opportunities.

Venmo already has more than 95 mn active accounts.8 It should not be too difficult to expand its product offerings and increase monetisation.

USD 2bn revenue from advertising? In 2022, Uber Technologies, Inc. (UBER 0.00%↑ US) launched its advertising business. By 2025, Uber Advertising brought in more than USD 2 bn of annual revenue.9

Despite being immaterial now, PYPL’s advertising revenue has the potential to match or even exceed USD 2 bn. PYPL’s 227 mn MAUs exceed UBER’s 202 mn. PYPL has deeper data on its users’ spending habits.

In 2024, PYPL hired Mark Grether, who formerly led UBER’s advertising business, to lead its newly created PayPal Ads division.10

PYPL’s advertising division seems to be gathering momentum. In 2025, PYPL launched PayPal Ads Manager, a zero-cost tool that enables merchants to monetize store traffic by displaying relevant advertisements on their websites.11

Capital returns?

Attractive capital return. In the last twelve months, PYPL returned USD 6,545 mn to shareholders, mainly through share buybacks. This represents ~17% of its market capitalisation today.

I estimate PYPL generates ~ USD 4,500 mn of free cash flow to firm (FCFF).

If capital returns normalise to FCFF, this will still represent ~12% yield on today’s market capitalisation. The 8% premium over United States 10y government bond looks attractive.

PYPL can likely sustain returning ~100% of its FCFF to shareholders because it is a capital-light business. Working capital requirements are not significant because PYPL sells most of its loan receivables upon origination.

Catalysts

Potential sale. In Feb 2026, Bloomberg reported that Stripe Inc., a payment processor, is considering an acquisition of all or parts of PYPL.12

The probability of a sale is high, in my view. PYPL is trading at an all-time low NTM PE of 7.8x, despite significant growth opportunities in BNPL, Venmo and advertising.

In Apr 2026, new CEO Lores simplified PYPL’s organisation into 3 segments: Checkout Solutions & PayPal, Consumer Financial Services & Venmo, and Payment Services & Crypto.13 This cleaner structure makes it easier for acquirers to buy part or all of PYPL.

Factors to focus on

Growth potential. My initial estimates suggest PYPL can generate an incremental annual revenue of at least USD 2 bn just from raising BNPL penetration.

I expect another USD 2 bn incremental annual revenue from its advertising division.

How much incremental revenue can Venmo generate?

How reasonable are my initial estimates? How successful will the new CEO be in realizing these growth opportunities?

Sustainability of transaction margin. Transaction margin refers to the portion of net revenues left after paying transaction expense and transaction and credit losses.

Despite the growth opportunities in BNPL, Venmo and advertising, traditional transaction fees remain the bulk contributor to revenue and profits.

PYPL’s sell-off on 3 Feb 2026 was partly driven by its guidance for a slight decline in transaction margin during 2026. This was unexpected.

Beyond 2026, will transaction margin continue declining?

Coming up next

In the past 10 years, shareholders of iFAST Corporation Ltd. (AIY; IFAST SP) enjoyed 27% return per year.

This is despite the saturation of the market by new players like Futu Holdings Limited (FUTU 0.00%↑ US).

What’s the secret behind AIY’s success?

Is there still an opportunity for investors?

I will explore this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in PYPL, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.

informative

Nice & Interesting write up - while the option value is apparent, what would be a worthwhile exercise is to understand the levers within its core transaction business. An underappreciated fact is that they own deposit licenses in many geographies which ensures they earn returns on customer float - in a falling rate environment that becomes a drag but can work the other way if rates rise.