No, I don’t believe SK hynix’s forecast of shortage beyond 2030

Inventory trends show shortage will likely end sooner than expected

Last week, SK hynix’s CEO forecasted the memory chip shortage will last beyond 2030.1

I am not sure.

We’ve talked before about the current shortage. In April 2026, I showed how we can use the price and cost of memory chips to forecast the semiconductor cycle.

John Kenneth Galbraith famously declared that “There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.”

I am reluctant to make a forecast.

But just for fun, if you put a gun to my head, I dare say we are probably closer to the peak than most expect.

In April 2026, I ventured:

“I don’t provide financial advice or recommendations. But like any other private investor, I can always share my forecasts and how I am positioning my personal portfolio.

I estimate the shortage will end around Q1’27. Capex growth peaked around Q4’25. Historically, ASP starts to collapse 2 to 4 quarters after the peak in capex growth.

Because of forward guidance, investors will start reacting one or maybe two quarters before Q1’27. This means the rally in SOXX will probably end around Q4’26.”

Why does this puny analyst think the shortage will end before 2030?

Let me support my estimates with working capital trends. Specifically, inventory.

Don’t look at what they say, look at inventories

When demand is strong, inventory draws down. When demand is weak, inventory piles up.

That’s the basic principle.

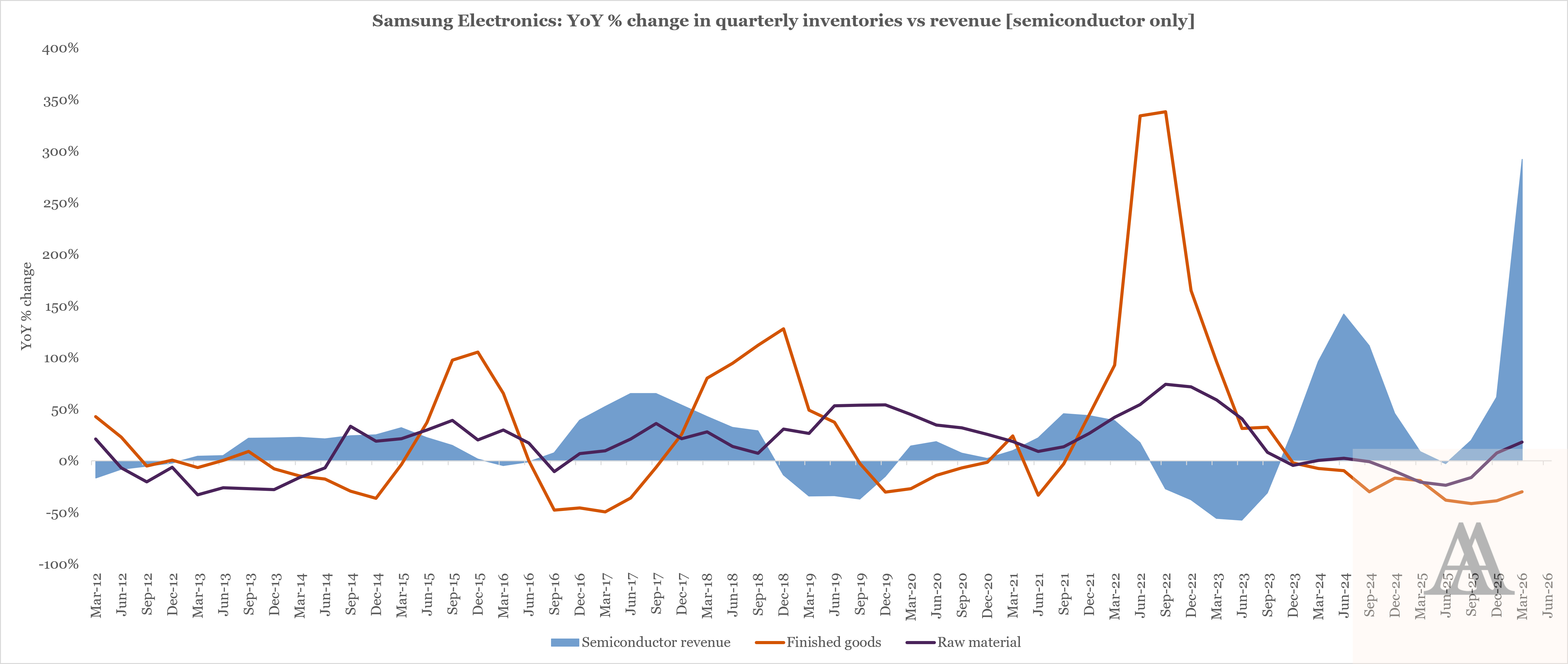

We can add more sophistication by analysing the breakdown of inventory. Almost all companies will break down their inventory into 3 components:

Raw materials

Work in progress

Finished goods

When demand recovers and customers start ordering, the chipmakers will draw down their finished goods. Finished goods start decreasing. The chipmakers start ordering raw materials to replenish their finished goods. Raw materials start increasing.

In other words, when demand is strong, raw materials grow faster than finished goods.

You can see this in the chart below.2

When raw materials start growing faster than finished goods, this signals revenue growth will start accelerating soon after.

Source: Samsung Electronics Co Ltd (005930 KS); Angsana Anderson estimates

The reverse applies too. When finished goods start growing faster than raw materials, this is a leading indicator that revenue growth will start declining.

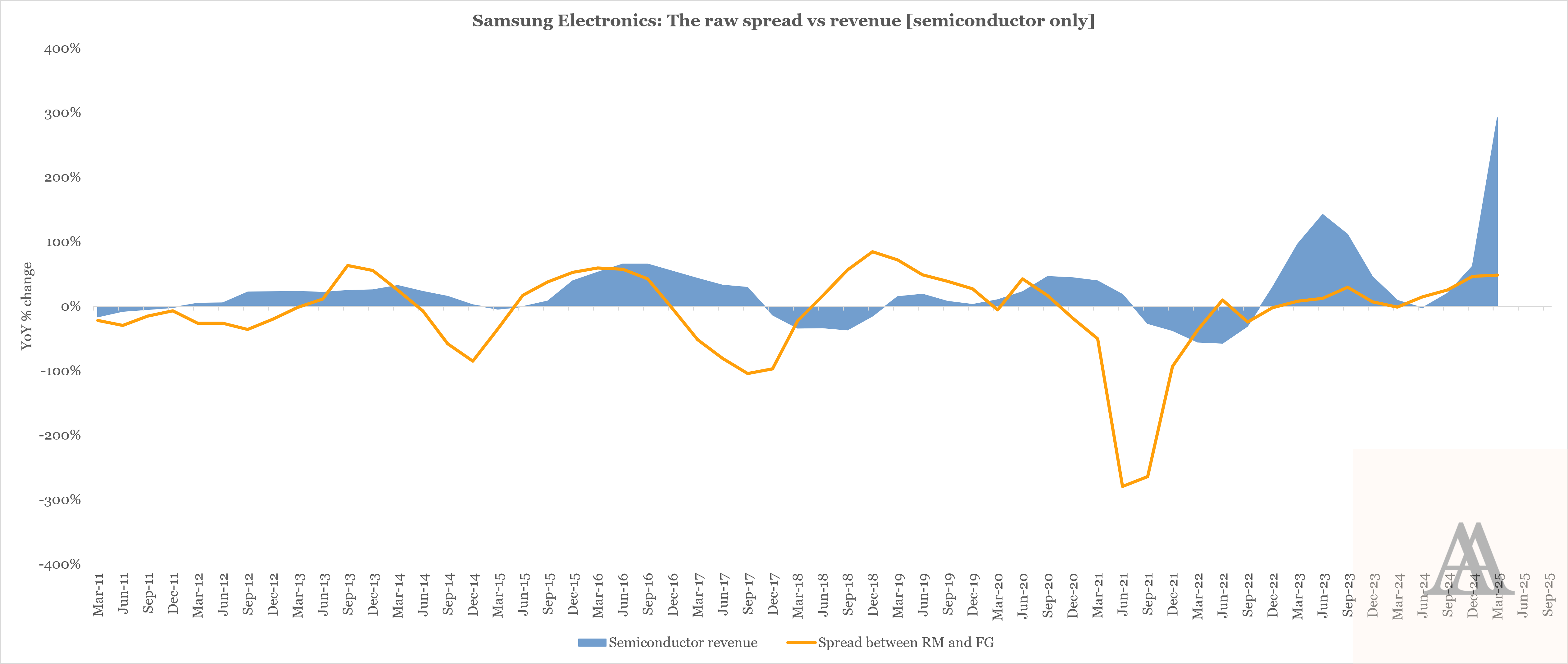

The raw spread

To spare our eyes, let’s combine this into just 1 indicator: raw materials growth – finished goods growth.

Because “the spread between raw materials growth and finished goods growth” is quite a mouthful, I will just call this “the raw spread”.

When the raw spread is positive, it means raw materials are growing faster than finished goods.

Source: Samsung Electronics Co Ltd (005930 KS); Angsana Anderson estimates

The raw spread leads revenue growth.

In Q1’24, the raw spread bottomed out and started growing. Revenue growth followed just one quarter later.

Today, the raw spread is still positive, but it has slowed down. A peak looks nearby.

This brings me back to my point

We are probably closer to a peak in the semiconductor cycle than the consensus and industry insiders believe.

If the shortage lasts beyond 2030, I would be very surprised.

But don’t bet the farm on forecasts. Remember, there are only two kinds of forecasters in the world!

Thanks for reading! If you found this helpful, hit the “like” button.

If you’re not already a subscriber, sign up for weekly analysis on global SMID equities, including semiconductors.

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in 000660 KS, 005930 KS, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.

References & Notes

I use Samsung Electronics because their data is the most readily available to me. If I plot the same chart for SK hynix, it should look the same. Memory chips are commodities.