Micro-Mechanics: After a +97% rally, is it too late to buy?

[Thesis & Update] Micro-Mechanics (Holdings) Ltd. (5DD; MMH SP)

On 28 Jan 2026, I bought 5DD shares and wrote the first version of this thesis.

I have reproduced the thesis here, with corrections and edits for brevity and clarity. The core thesis is unchanged.

Under the ‘Subsequent events’ section, I added updates from the most recent earnings, as well as my latest assessment and decision.

About (28 Jan 2026)

Share price: SGD 1.61

Market capitalisation: SGD 224 mn (USD 177 mn)

Enterprise value (EV): SGD 198 mn (USD 156 mn)

Average daily volume (ADV): SGD 0.2 mn (USD 0.2 mn)

LTM P/E: 17x; LTM P/B: 4.2x

My decision (28 Jan 2026)

I bought my shares at SGD 1.62. Within 3 to 5 years, I expected to sell my shares for at least SGD 3.20.

Over 3 years, I expected to earn ~29% p.a. (26% capital gains; 3% dividend yield). Over 5 years, I expected to earn ~18% p.a. (15% capital gains; 3% dividend yield).

Background

Micro-Mechanics: After a +97% rally, is it too late to buy?

At the start of the year, Micro-Mechanics was an unloved orphan. The consensus? “A lousy cyclical business with no liquidity.”

Today, the narrative has flipped. After surging +97% year-to-date, there is palpable excitement surrounding the shares.

In this post, I’ll break down why I bought shares in 5DD on 28 Jan 2026. I will also try to make sense of the sudden rally that even surprised me.

Finally, I will tackle the most important question: Is it too late to buy?

Business model

5DD’s financial year ends in Jun every year. Unless stated otherwise, all time references will follow 5DD’s financial year. For example, Q2’26 refers to Oct 2025 – Dec 2025.

Breakdown of FY2025 revenue (SGD 65 mn, +13% YoY):

77% consumable tools (+6% YoY)

23% wafer fabrication equipment (WFE) parts (+46% YoY)

The consumable tools segment focuses on the design and manufacturing of miniature consumable tools used in the assembly and testing of semiconductors.

The main consumable tools are die attach tools, wire-bonding tools and encapsulation tools. These tools are used to package bare (‘naked’) chips into finished products. Elastomer (rubber) products represent ~30% of group revenue.1 For details, please see Micro-Mechanics’ product catalog.

The WFE parts segment focuses on making metal components and precision parts such as wafer‑handling parts and precision mounts for semiconductor wafer fabrication equipment. It is largely carried out by its US subsidiary (MMUS).

5DD has > 600 customers worldwide. Historically, major customers include leading outsourced assembly and testing (OSAT) companies like Amkor. In FY2025, 1 customer of the wafer fabrication equipment parts segment represented 10% of group revenue.

31% of revenue comes from China, 22% from USA, 18% from Malaysia and the remaining 29% from the rest of the world.

The largest expense is cost of sales (51% of revenue). This mainly consists of cost of inventories sold.

5DD operates in a niche, fragmented industry. 5DD is much larger than most consumable tooling competitors, but smaller than its WFE parts competitors.

In its consumable tooling segment, its direct competitors are mostly private. These include SPT Roth Ltd (SPT) and Micro Point Pro Ltd (MPP).

SPT seems like the largest competitor. It has 6 locations around the world. LinkedIn shows 156 employees. 5DD’s LinkedIn shows 144 employees and 5 locations.

5DD’s competitors in its WFE parts segment include Frencken Group Limited (E28; FRKN SP) and UMS Integration Limited (558; UMSH1 SP). That said, these competitors are not directly comparable because they have other segments like contract assembly and contract manufacturing.

Founder Christopher Borch and his family control over 43% of 5DD. Former COO Low Ming Wah owns another 5%. Yeo Seng Chong, the founder of Yeoman Capital, owns 0.5% in his personal capacity.

Institutions remain a small presence. No private equity or activists on the shareholder registry.

For a more in-depth introduction to 5DD’s business, check out:

· MONEY FM 89.3’s Chua Tian Tian interviews Micro-Mechanics CEO Kyle Borch

· NUS Professor Mak Yuen Teen’s case study on Micro-Mechanics (page 54). It is one of the few companies that has made the mark on Prof. Mak’s books.

· The Fifth Person interviews CEO Borch

My reasons

Cyclical inflection

Customers report higher demand. The semiconductor industry is notoriously cyclical.

A quick scan of the earnings call of major semiconductor companies suggests an inflection point is near. In their latest earnings call, direct customers such as Amkor Technology, Inc. AMKR 0.00%↑ and ASE Technology Holding Co., Ltd. (3711 TT) provided positive outlooks.

On 28 Jan 2026, Texas Instruments TXN 0.00%↑, a leading analog chipmaker and probably an important customer of 5DD, reported better-than-expected outlook. This prompted a +10% share price jump in just one day.

Customers’ inventory is low. The higher demand reported by customers will likely flow quickly to 5DD because customers’ inventory is low.

Although inventory days remain above average across analog names like TXN, analog integrated device manufacturers (IDMs) like TXN are only a part of 5DD’s customer base.

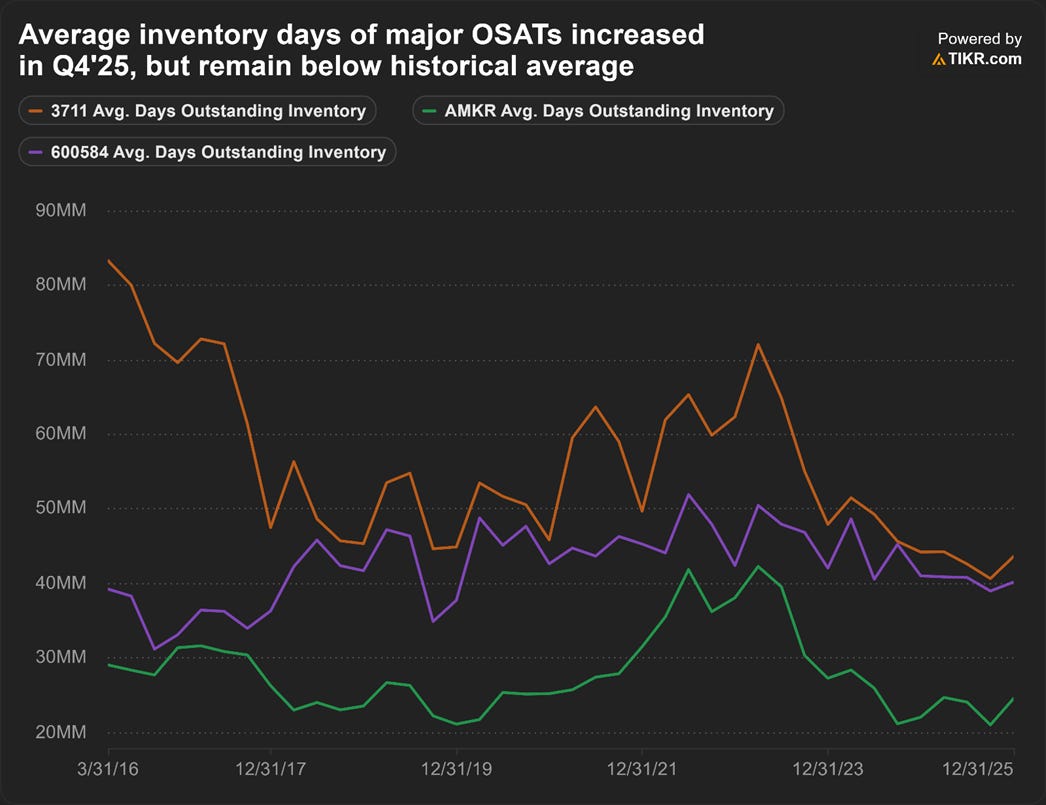

Inventory days at major OSATs (5DD’s other major customer group) like Amkor, ASE, JCET have largely trended below average and are near all-time low.

5DD reaching an inflection point. After 2 consecutive years of revenue decline, revenue finally grew +13% in FY2025.

Inventory days are near all-time low ~38 days in Q2’26. The 10-year average is ~53 days.

Good business, temporary headwinds

5DD is a high-quality business. Since 2006, 5DD’s return on asset (ROA) averaged ~14%. Such high ROA is rare in the industry and signals a high-quality business.

I believe 5DD achieves high ROA because its products are low-ticket, yet mission critical, thereby creating high switching costs for its customers.

5DD’s largest product category is probably its rubber tips. After cutting (‘dicing’) completed silicon wafers into individual chips (‘dies’), semiconductor manufacturers use these rubber tips to pick up the dies and package them.

These rubber tips are mission critical. If the tips are poor quality or worn out, they will contaminate the dies. The dies may need to be discarded.

Despite their importance, these rubber tips are low-ticket. A rubber tip can retail for less than USD 1.00 per unit.2 Wholesale prices should be lower.

In contrast, a completed silicon wafer costs from USD 3,000 for a mature node to USD 30,000 for the most advanced nodes.3

If 5DD’s rubber tips work, why switch to an unproven new supplier and risk spoiling expensive wafers just to save a few cents?

But the market has not fully recognised 5DD’s quality. Between Oct 2025 and Dec 2025, 5DD’s share price sold off after it faced headwinds. 5DD reported +3% YoY quarterly revenue growth, down from +12% in the previous quarter.

The headwinds are likely temporary. The headline +3% is masking the business quality and its true growth potential.

Revenue at consumable tools segment actually grew +8% YoY. WFE parts revenue fell -15% YoY because of delays in materials and shortages.

However, order book increased +20% QoQ. Revenue growth will likely accelerate in future quarters as 5DD resolves the materials shortage.

Indeed, by mid-Nov 2025, the CEO said the material shortage in the WFE parts segment had been resolved.4

Reading between the lines, this implies pushing of revenue from Q1’26 (Jul 2025 to Sep 2025) to Q2’26.

Valuation

At the share price of SGD 1.61 on 28 Jan 2026, 5DD offered 9% free cash flow yield on EV. This yield is likely sustainable because I believed 5DD is at the bottom of the semiconductor cycle.

9% is an attractive 6.8 percentage points (ppt) premium over Singapore’s 10-year government bond yield of 2.2%.

I estimated intrinsic value at SGD 3.20 per share based on a discounted cash flow valuation.

This implies ~50% margin of safety and ~98% upside. This looked very attractive to me.

Catalysts

Capital return when the cycle turns. The semiconductor cycle will eventually turn. When it inflects, 5DD has always returned the excess profits to shareholders. Dividend payout ratio averaged 85% in the past 10 years.

Singapore EQDP. Singapore has injected SGD 4 bn into the local stock market, with plans to inject another SGD 1 bn in 2026.

The total SGD 5 bn will be placed with fund managers to invest in Singapore equities, especially small and mid-caps.

This has driven price discovery among Singapore mid-caps, but not yet for small-caps like 5DD.

As the fund managers build up their research capabilities, small-caps like 5DD will likely appear on their radar.

Risks

What if the semiconductor cycle fails to turn?

In an unexpected downturn, 5DD’s downside is protected by 2 factors: (a) recurring revenue from low-ticket, mission critical consumable tools and (b) no debt (cash > 10% of market cap.).

Previously, we discussed how 5DD’s high-quality business stems from selling low-ticket, mission critical tools.

The other advantage that we have not talked about is that these tools create recurring revenue because they are consumables. These tools will wear out, some need to be replaced within hours.

Replacement cannot be delayed. Otherwise, the production line will stop. In any case, it does not make sense for customers to delay buying replacements from 5DD. These are low-ticket items.

That’s why, during downturns, 5DD is more resilient.

In the most recent downturn during FY2023, 5DD’s revenue declined only -19% compared to -27% for SK hynix Inc. (000660 KS) and -50% for Micron Technology, Inc. MU 0.00%↑.

Factors that could lead me to increase investment in 5DD

Evidence that the current upcycle will be much stronger than historical cycles.

Share price falls > 30% without significant deterioration in business fundamentals.

Factors that could lead me to decrease investment in 5DD

Strong evidence that we are approaching the peak of the semiconductor cycle, and other investors are extrapolating the peak earnings and overpaying for 5DD shares.

Subsequent events

Q2’26 earnings

On 29 Jan 2026, 5DD released their earnings, followed by an earnings call the next day.

My thesis seems to be playing out.

Good business, temporary headwinds

Headwinds temporary. As I expected, revenue growth accelerated to +15% YoY in Q2’26, up from +3% YoY in Q1’26.

WFE parts segment recovered from material delays and shortage. Revenue increased +6% YoY in Q2’26, up from -15% YoY in Q1’26.

Revenue growth from consumable tools accelerated to +17% YoY in Q2’26, up from +8% YoY in Q1’26.

Cyclical inflection

Customers placing more rush orders. Demand is strong and improving.

CEO Kyle Borch reported WFE parts customers placing more advance orders.

Consumable tools customers are placing more rush orders and are increasingly concerned whether they can get their consumable tools fast enough to support their own customers.

Working capital trends signal cyclical inflection. Although 5DD does not provide guidance, working capital trends suggest the cycle has likely bottomed out and outlook is better than expected.

After multiple quarters of destocking, inventory finally increased slightly by +2% YoY in Q2’26. Coupled with the acceleration of revenue growth to +15% YoY in Q2’26, this suggests 5DD likely sees strong demand and is stocking up to meet that demand.

VP Finance Wendy Tan explained that the inventory increase in Q2’26 was concentrated on raw materials.

This supports my hypothesis. Demand likely grew stronger than expected because 5DD is finally restocking inventory after multiple quarters of destocking.

Low risk of irrational capacity expansion over the next year. I asked, “What are the risks of your competitors irrationally expanding capacity?”

CEO Kyle Borch believes this risk is low over the next year or so. “There is certainly a lot of demand… real demand…”

Catalysts

Singapore EQDP. Besides engaging the funds that received the SGD 5 bn EQDP allocation, CEO Kyle Borch did not offer more details on how they plan to benefit from Singapore’s EQDP. Reading between the lines, it seems like this is not their priority.

On the positive side, they noted multiple new faces during this earnings call, including myself.

Besides boutique fund managers and sell-side, I noticed analysts from at least 2 funds that received SGD 5 bn EQDP allocation.

In my thesis, when commenting on catalysts, I said ‘As the fund managers build up their research capabilities, small-caps like 5DD will likely appear on their radar.’ The participation of these analysts supports this.

5DD will likely increase capital returns only after multiple quarters of good performance. The negative point is that 5DD kept interim dividend unchanged at 3 cents.

In FY2024, 5DD cut their interim dividend in half. I believe management wants to see multiple quarters of good performance before increasing dividends again.

My decision (24 Apr 2026)

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

In less than 3 months, 5DD’s share price has climbed to SGD 3.24. I do not expect every stock I buy to perform like this. Furthermore, performance should be assessed across the entire portfolio, not based on a single winning call.

I have made my share of mistakes, including Haw Par Corporation Limited (H02; HPAR SP).

I will certainly make more. What’s important is that, over a full market cycle, my portfolio outperforms.

I have been in this business long enough to know that skill matters, but luck and emotional discipline matter just as much, if not more.

Peter Lim, a Singaporean billionaire investor reportedly said: “When you are holding stocks, if it goes up, don’t be too happy; when it goes down, don’t be too sad. Otherwise, how? Your life will also be fluctuating, and you’ll die of a heart attack.”5

I decided to hold. I believe 5DD is not overvalued, despite the near +100% rally this year. At the current share price of SGD 3.24, I believe it is only trading around its intrinsic value.

Looking to redeploy. That said, I am leaning towards redeploying a portion of the capital to other more attractive opportunities when they arise.

Upside not obviously greater than downside. My leading indicators signal that we could be approaching the peak of the memory cycle.

Even though I estimate 5DD has more exposure to analog chips than memory chips, the memory cycle is important because it leads the analog cycle.

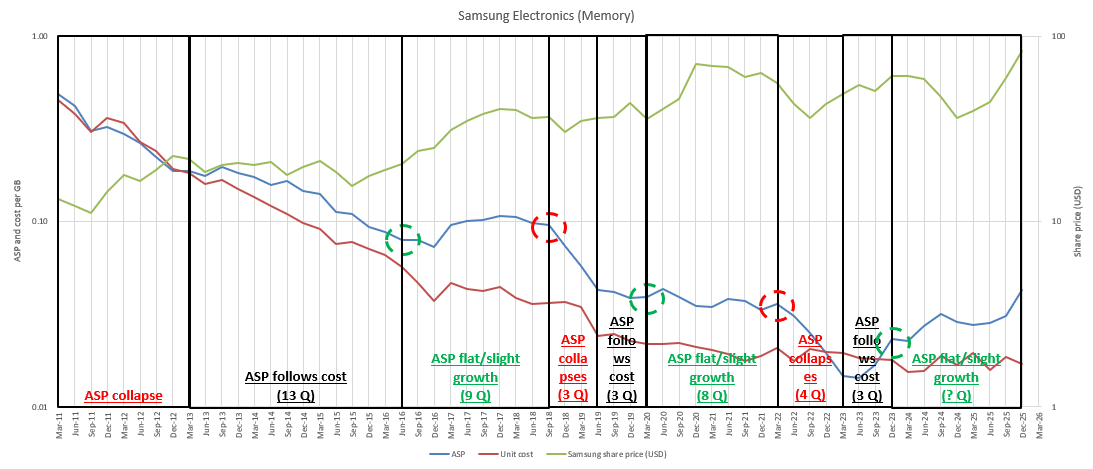

Margins on memory chips at unprecedented highs. The gap between the average selling price of memory chips (ASP) and unit cost is the widest it has ever been since 2011.

Is it possible that the margins continue to exceed expectations and widen further? Yes.

Is it probable? I believe not.

But capex growth peaking. Capex growth at major memory chip makers like SK Hynix has peaked around Jun 2025.

Historical precedents show that ASP typically collapses within a few quarters of capex growth peak. The opening of new fabs floods the market with more memory chips. This pushes down ASP.

In summary, I am maintaining my position in 5DD for now. However, with the risk/reward profile becoming less attractive, I am actively looking to rotate this capital once a more compelling opportunity presents itself.

Risk looks low in the near-term. My decision to hold through the near term is driven by a low probability of a major disappointment in the upcoming earnings call on Tue 28 Apr 2026.

Positive industry read-throughs. On 22 Apr 2026, TXN reported a better-than-expected outlook, prompting a nearly +20% share price jump in just one day.

Healthy channel dynamics. Average inventory days for major OSATs ticked up slightly in calendar Q4’25 but remain comfortably below historical averages.

Upcoming events

Tue 28 Apr 2026: Q3’26 earnings release

Wed 29 Apr 2026: Q3’26 earnings call

Valuation model

Subscribers may request a free copy of my valuation model by emailing me at angsana.anderson@gmail.com.

I will send out my model by the end of Sun 26 Apr 2026.

Coming up next

Where are we in the semiconductor cycle?

When I was a junior semiconductor analyst, I hung onto every word of the CEOs of major semiconductor companies.

After multiple quarters of “seeing the bottom pushed out”, I realised that even industry leaders have limited visibility into the cycle’s timing, or their public guidance is inherently constrained by corporate policies.

I was lost in the wilderness. That is, until I found this framework:

Source: Samsung Electronics Co., Ltd. (005930 KS); Angsana Anderson

In my next post, I will explain why the semiconductor industry is so notoriously cyclical, and why, despite the recent tremendous growth, it will likely remain cyclical.

I will also demonstrate this framework.

How do I use it to understand where we are in the cycle, and what likely lies ahead of us now?

Subscribe for free to get my next analysis when I publish it.

Subscribe for 2 to 3 analyses of global SMID equities every week. Discover overlooked ideas and rethink familiar names. Published by Andrew Wong, ACA, CFA

Disclaimer

This is a record of my investment decisions, not financial advice. I may change my decisions without notice. Use this only for education and entertainment. All analysis and opinions expressed are solely my own, and 5DD has not reviewed or endorsed this post. Do not rely on this for your investment decisions. I hold shares in 5DD.

This sounds compelling. Is there somewhere to register for the analyst call?