MegaStudyEdu: Why is South Korea’s top online school trading at only 5x P/E?

[Shortlist] MegaStudyEdu Co. Ltd (215200 KS)

About (05 May 2026)

Share price: KRW 46,800

Market capitalisation: KRW 485 bn (USD 328 mn)

Enterprise value (EV): KRW 450 bn (USD 305 mn)

Average daily volume (ADV): KRW 2 bn (USD 1.3 mn)

LTM P/E: 5x

Time spent: ~1 day

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Shortlist

Background

“Every year in November, Suneung brings the whole country to a standstill.

Silence descends across the capital Seoul as shops are shut, banks close, even the stock market opens late. Most construction work halts, planes are grounded and military training ceases.

Occasionally the stillness is broken by distant sirens - police motorbikes racing to deliver students running late to their exam.”

That’s how the BBC described CSAT (Suneung).

CSAT is South Korea’s most important exam. A one-day exam will decide your university, your career, your social standing and even who you date.

With such high stakes, many turn to private educators. MegaStudyEdu is one of the top 3 CSAT prep providers in the country.

It boasts a deep bench of star tutors like Stanford-educated Hyun Woo-jin. He reportedly earns up to USD 20 mn a year.1

Yet, MegaStudyEdu’s shares present a puzzling disconnect. Its dividends and share buybacks amount to ~12% of its market capitalisation. It looks likely to sustain its revenue in 2026.

But it trades at only 5x P/E.

Could MegaStudyEdu be an opportunity?

In my latest Substack post, I’ll explain why I shortlisted the company for further investigation.

Business model

MegaStudyEdu is South Korea’s educational ‘Netflix’.

It is one of the country’s largest “online cram school”. Students can watch lectures from famous star teachers, do practice questions, and get data-based advice on their chances of getting into certain universities.

The company was one of the first to focus mainly on online lessons.

It grew by hiring very popular teachers, recording their lectures once, and then selling those videos to many students at a lower price than traditional offline classes.

Today, 67% of its revenue comes from lectures, mostly online. Students pay their fees in advance. MegaStudyEdu recognises revenue over time as it provides access to the lectures.

The remaining 33% comes from selling textbooks, mock exams, study rooms, etc.

Breakdown of 2025 revenue (KRW 885 bn, -6.1% YoY):

63% from High school (-4.4% YoY)

24% from Early childhood, elementary and middle school (-5.3% YoY)

9% from University (-1.2% YoY)

4% from Employment (-34.2% YoY)

High school revenue mainly comes from selling lectures to high school students, especially those sitting for the College Scholastic Ability Test (CSAT).

According to MegaStudyEdu, it holds ~ 74% market share, up to 3x higher than the next closest competitor.2

Early childhood, elementary and middle school revenue comes from selling lectures to toddlers, elementary and middle school students.

These students are relatively younger, making it difficult for them to sustain self-directed online learning. Consequently, they tend to prefer offline academy classes where there is relatively more interaction between teachers and students.

The University segment earns revenue from providing lectures to students seeking university transfers.

MegaStudyEdu earns almost 100% of its revenue in South Korea.

The largest expense is instructor fees (21% of revenue), followed by employee salaries (16%).

The closest public comparable is Digital Daesung Co., Ltd. (068930 KS). They operate the Daesung MyMac online learning platform and physical cram schools, competing directly for high school students preparing for the CSAT.

My reasons

Under-recognised growth?

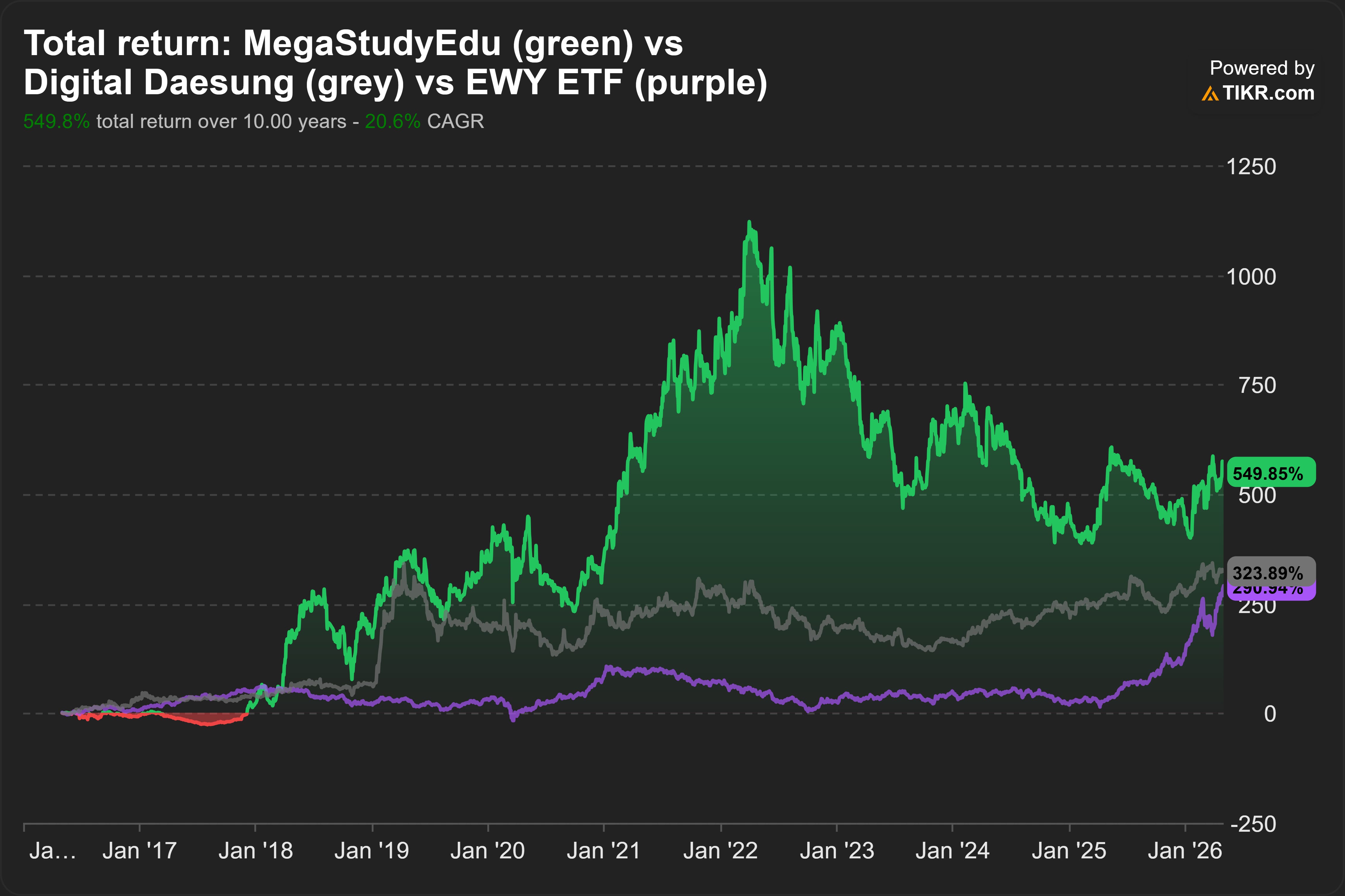

The market appears to be pricing in an indefinite revenue decline. I plotted the 10-year total return of MegaStudyEdu against Digital Daesung. As a baseline, I included EWY, an ETF tracking the MSCI Korea 25/50 Index.

Source: Tikr

MegaStudyEdu and Digital Daesung are generally uncorrelated with EWY.

Both companies rallied in 2021. COVID-19 lockdowns drove higher enrolment in online cram schools. In just one year, MegaStudyEdu more than tripled its earnings per share (EPS) while Digital Daesung grew its EPS by +52%.

The consensus extrapolated the tremendous growth and paid up for MegaStudyEdu and Digital Daesung. In 2021, LTM P/E peaked at 34x and 19x respectively.

The tremendous growth could not be sustained after the lockdowns ended. Revenue growth at MegaStudyEdu decelerated and eventually turned -6.1% in 2025. LTM P/E compressed.

Today, at 5x LTM P/E, MegaStudyEdu is priced like a terminally declining business.

However, there are reasons to be skeptical. First, the headline is overstating the decline. MegaStudyEdu disposed a loss-making subsidiary (Next Study Co., Ltd.) in 2024. If not for this disposal, the revenue decline in 2025 would be -3% instead of the headline -6%.

Second, there are signs that MegaStudyEdu is near the trough in revenue.

In 2025, prepayments from customers (contract liabilities) remained essentially flat, an improvement from -15% in 2024. This suggests revenue will likely remain flat or even grow slightly in 2026.

Capital returns?

Capital return represents ~12% of market capitalisation. In Apr 2025, MegaStudyEdu announced its corporate value-up program. It targets to return 60% of net income via dividends and share buybacks.

For 2025, MegaStudyEdu returned KRW 51 bn of capital to shareholders, representing 65% of net income. This is ~12% yield on market capitalisation.

If earnings remain stable and the company continues this policy, this will imply a recurring 11% yield on market capitalisation. This is an attractive 7% premium over South Korea’s 10-year government bond yield.

Attractive capital returns likely sustainable. I believe there is a very good chance that MegaStudyEdu can maintain such attractive capital returns.

For the reasons I discussed above, revenue looks near a trough.

MegaStudyEdu is cash generative.

The company operates with favourable working capital. It collects fees in advance from students and pays its instructors later.

Besides some physical academies, there are no significant capital expenditure requirements. Most of the lectures are streamed online.

Catalysts

On 4 Feb 2026, Maeil Business reported that the management (and major shareholders) are looking to sell 32% of the company to private equity. The sale price would value the entire company at around KRW 925 bn.3

The company denied this report on 5 Feb 2026.4

On a side note, Perplexity did not catch this company announcement. I guess generative AI still can’t completely replace me rolling up my sleeves and combing through the regulatory filings. Or maybe I should buy a more powerful model?

That said, I believe there is a good chance of an eventual sale.

In 2022, the major shareholders were negotiating a sale to MBK Partners, one of North Asia’s largest private equity (PE) firms. The negotiation eventually broke down. Apparently, they disagreed on price.

The major shareholders (and management) are near retirement age. The company has not publicly identified a clear next-generation successor.

Factors to focus on

Revenue deceleration? Is post-lockdown normalisation the complete explanation behind the recent years of revenue deceleration?

In 2025, management also attributed the -4% decline in High School revenue to ‘the trend of top-tier students preferring self-study for retaking the college entrance exam persists’.

Digital Daesung, its direct competitor, also experienced similar deceleration. However, in recent quarters, it managed to maintain low positive revenue growth while MegaStudyEdu experienced low single-digit decline. Why?

Substitution risks? The Ministry of Education (MOE) provides free online CSAT lectures via Educational Broadcasting System internet (EBSi). The purpose is to help curb private education costs.

The MOE explicitly targets a ~50% linkage rate between EBSi materials and the actual CSAT exams. As a result, MegaStudyEdu faces substitution risks.

However, EBSi acts as a price and share ceiling at the low end of the market but has not displaced premium private CSAT prep providers like MegaStudyEdu. The company continues to differentiate on content quality, teacher reputation, and data-driven services.

EBSi has been free since it launched in 2004. In contrast, a MegaPass costs around KRW 600,000 (~ USD 400) per season. A MegaPass is the company’s all-access online subscription service providing unlimited access to lectures.

Despite the price difference, I estimate MegaStudyEdu grew its revenue by 4.4% p.a. since 2004.

A cursory browse through DC Insider, the Reddit-equivalent in South Korea, reveals students still perceive the company’s star lecturers as superior.

AI disruption? I believe this risk is low.

The lecturers on MegaStudyEdu are not just lecturers. They are celebrities.

According to Korea JoongAng Daily, “The relationship between students and star lecturers is similar to the one between fans and K-pop stars. Students even buy merchandise that includes bags, mugs and stickers.”5

The lecturers not only teach, but they motivate, entertain, console and even admonish.

Upcoming events

Fri 15 May 2026: Q1’26 earnings release (expected)

Coming up next

Is Duolingo AI-resistant?

OpenAI released ChatGPT in Nov 2022.

Chegg, Inc. (CHGG US), a popular edutech company, has been on the decline ever since. Revenue first declined -1% in 2022, then -7% in 2023 before collapsing -39% in 2025. The share price is down almost -95%.

In contrast, Duolingo, Inc. (DUOL US) is going from strength to strength. Revenue continued growing. +47% in 2022, +44% in 2023 and +39% in 2025.

Why?

I will explore this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in 215200, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.