MegaStudyEdu: Why South Korea's top private educator can be a 3x

[Thesis] MegaStudyEdu Co. Ltd (215200 KS)

Summary

I bought shares in MegaStudyEdu Co. Ltd (215200 KS).

At 4x P/E and 8% dividend yield, South Korea’s top private educator is priced like a dying business. It’s not.

Despite declining student population, the industry is still growing. More parents are enrolling their children in private education, and they are also spending more per child.

South Korea’s expenditure on private education has grown steadily over the past 10 years. In 2025, it declined for the first time.

That -6% decline was concentrated among lower-income households, which supports my view that the weakness is cyclical rather than structural.

Since 2024, the government’s Neulbom School program has provided competing services. However, in Mar 2026, the program stopped expanding.

The trends in advance payments from customers, a leading indicator, suggests revenue has likely bottomed out.

MegaStudyEdu’s dividends and share buybacks in 2025 represented ~12% of its current market capitalisation. This is an attractive 7 percentage points (ppt) premium over South Korea’s 10-year government bond yield. It also appears sustainable.

Catalysts: activist investor and potential sale to private equity.

About (11 Jun 2026)

Share price: KRW 38,900

Market capitalisation: KRW 403 bn (USD 265 mn)

Enterprise value (EV): KRW 321 bn (USD 211 mn)

Average daily volume (ADV): KRW 2 bn (USD 1.3 mn)

NTM P/E: 4x

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

I bought my shares at KRW 37,700. Within 3 to 5 years, I expected to sell my shares for at least KRW 125,000.

Over 3 years, I expected to earn ~57% p.a. (49% capital gains; 8% dividend yield). Over 5 years, I expected to earn ~35% p.a. (27% capital gains; 8% dividend yield).

Background

A month ago, I shortlisted MegaStudyEdu Co. Ltd (215200 KS). Since then, its share price has fallen almost -17%.

Investors seem to believe the business will shrink indefinitely.

However, recent earnings showed MegaStudyEdu maintained revenue, while increasing net profit after tax by 8% YoY in Q1’26.

The indicators I monitor suggest MegaStudyEdu has reached a bottom.

Business model

Please see my prior post: MegaStudyEdu: Why is South Korea’s top online school trading at only 5x P/E?

My reasons

Under-recognised growth

Priced like a dying business. At 4x NTM P/E, the market seems to be pencilling in a significant decline in MegaStudyEdu’s profits.

“Don’t you know South Korea’s population is declining?”

Indeed, the number of elementary, middle and high school students has been declining in the past 10 years:

Source: Ministry of Data and Statistics (2026)

But the industry is growing. Despite declining student population, South Korea’s total private education expenditures increased 4% p.a. in the past 10 years.

Source: Ministry of Data and Statistics (2026)

More students are using private education. In 2016, 68% of all students used private education. By 2025, the participation rate has increased to 76%.

Source: Ministry of Data and Statistics (2026)

More students use private education, and spending per student has also been rising steadily.

Source: Ministry of Data and Statistics (2026)

Fewer kids, more investment per kid. At first glance, MegaStudyEdu seems to be operating in a dying industry. South Korea’s student population is declining.

However, I believe the market is underestimating MegaStudyEdu’s growth potential. The industry has been growing ~4% p.a. in the past 10 years.

South Korean couples are having fewer children, but more parents are enrolling their children in private education, and they are spending more per child.

Good business, temporary headwinds

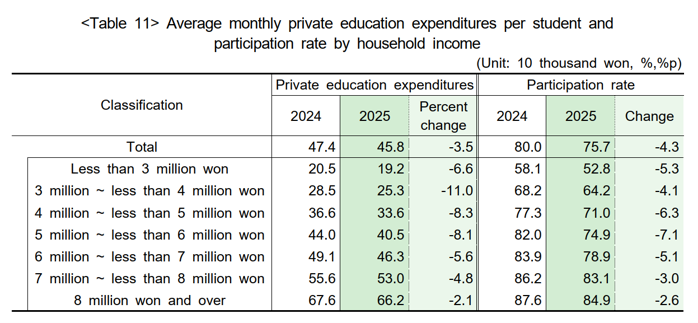

Private education expenditure declined -6% in 2025. This was driven by -7% decline in the number of participating students, partially offset by +2% increase in spending per participating student.

Temporary economic weakness. I believe the -6% decline in 2025 reflects a temporary headwind, rather than a structural decline.

Maeil Business News Korea reported “[In 2025], real consumption expenditure for all households also declined by 0.7 percent, indicating that rising prices weakened purchasing power, leading families to cut education expenses.”1

Indeed, private education expenditure declined the most among lower-income households:

Source: Ministry of Data and Statistics (2026)

Government has halted the expansion of Neulbom Schools. MegaStudyEdu’s early childhood and elementary segment suffered the steepest revenue decline in 2025.

Peers like Digital Daesung Co., Ltd. (A068930) are reporting similar trend. I suspect Neulbom Schools.

In 2024, the Ministry of Education introduced Neulbom Schools. This program aims to provide after-school care for all elementary school students.

Instead of online lectures and studying at MegaStudyEdu’s academies (‘hagwon’), the children will participate in after-school activities and daycare for free or at low costs.

As of Mar 2026, 552,000 first and second graders in elementary school were using the service. The plan was to expand it to all elementary school grades starting 2027.2

However, I believe Neulbom Schools is no longer a significant headwind.

In Mar 2026, the new government led by Lee Jae Myung halted the expansion of his predecessor’s Neulbom School initiative.3

The program will be maintained only for first and second graders. Third graders will instead be provided with a voucher for after-school programs annually.

Effectively, the government has admitted that it is difficult to replace the services provided by MegaStudyEdu and its peers.

“There is a tendency for third graders and above to prefer after-school programs focused on subjects like English and Math over Neulbom School”.

Furthermore, the government is struggling to cope with the increased workload on school staff if more students participated in the program.

Favourable working capital trends. MegastudyEdu’s advance payment from customers (unearned revenue) has stabilised in Q1’26.

This suggests that these headwinds are indeed temporary, and that revenue has likely bottomed out.

Source: Tikr

Capital returns

Capital return represents ~12% of market capitalisation. In Apr 2025, MegaStudyEdu announced its corporate value-up program.4 It targets to return 60% of net income via dividends and share buybacks.

For 2025, MegaStudyEdu returned KRW 51 bn of capital to shareholders, representing 65% of net income. This is ~12% yield on market capitalisation, an attractive 7 ppt premium over South Korea’s 10-year government bond yield.

Attractive capital returns likely sustainable. For the reasons, I discussed above, I believe MegaStudyEdu’s 12% yield is sustainable.

MegaStudyEdu is also cash generative.

The company benefits from favorable working-capital dynamics. It collects fees in advance from students and pays its instructors later.

Besides some physical academies, there are no significant capital expenditure requirements. Most lectures are streamed online.

Valuation

On 11 Jan 2026, MegaStudyEdu was trading around KRW 37,700 per share.

At that price, I believed MegaStudyEdu was very attractive. 4x NTM P/E and 12% capital return yield on a business that is likely to maintain revenue and profits.

To take advantage of the share price decline, I bought my shares before completing my discounted cash flow (DCF) valuation.

My initial estimates suggest MegaStudyEdu is worth at least KRW 125,000 per share. At this price, it would trade around 15x NTM P/E and 3.6% capital return yield. This is more consistent with a stable business.

For context, the iShares MSCI South Korea ETF, which tracks an index of South Korean equities, trades at 17x LTM P/E.5

Historically, MegaStudyEdu has traded around 7x NTM P/E. The market misunderstood it as a business inside a structurally declining industry.

For such a quality business, it should trade much higher than 7x NTM P/E. Its corporate value-up program, which we just discussed, and interests from activist and private equity (PE) investors will help catalyse its value.

Catalysts

Activist investor. On 16 Apr 2024, Dalton Investments, an activist investor, disclosed it had been investing in MegaStudyEdu since 2020.

The investor commended the company’s responsiveness to their recommendations for higher capital returns. “We are now truly delighted to see management making such a full commitment [to capital returns].”

Although I could not find Dalton Investments in MegaStudyEdu’s shareholder registry, both current and historical, I believe the investor is probably still a shareholder. Dalton Investments describe their investment horizon as between 5 to 10 years.6

Having a prominent activist investor on its shareholder registry will likely incentivise MegaStudyEdu to create more value for minority shareholders.

Potential sale. On 4 Feb 2026, Maeil Business reported that the management (and major shareholders) are looking to sell 32% of the company to private equity. The sale price would value the entire company at around KRW 925 bn.7

The company denied this report on 5 Feb 2026.8

Despite that, I believe there is a good chance of an eventual sale.

The major shareholders (and management) are near retirement age. The company has not publicly identified a clear next-generation successor.

In 2022, the major shareholders were negotiating a sale to MBK Partners, one of North Asia’s largest private equity (PE) firms.9 The negotiation eventually broke down. Apparently, they disagreed on price.

Risks

Substitution risks. The Ministry of Education (MOE) provides free online CSAT lectures via Educational Broadcasting System internet (EBSi). The purpose is to help curb private education costs.

The MOE explicitly targets a ~50% linkage rate between EBSi materials and the actual CSAT exams. As a result, MegaStudyEdu faces substitution risks.

However, EBSi acts as a price and share ceiling at the low end of the market but has not displaced premium private CSAT prep providers like MegaStudyEdu. The company continues to differentiate on content quality, teacher reputation, and data-driven services.

EBSi has been free since it launched in 2004. In contrast, a MegaPass costs around KRW 600,000 (~ USD 400) per season. A MegaPass is the company’s all-access online subscription service providing unlimited access to lectures.

Despite the price difference, I estimate MegaStudyEdu grew its revenue by 4.4% p.a. since 2004. A cursory browse through DC Insider, the Reddit-equivalent in South Korea, reveals students still perceive the company’s star lecturers as superior.

Regulatory risks. On Jul 2021, the government in mainland China banned for‑profit K‑12 after‑school tutoring.

The share price of tutoring companies collapsed. New Oriental Education & Technology Group Inc. (EDU US) fell almost -92% from its peak.

There are two reasons why I believe EDU is not a good precedent for MegaStudyEdu.

First, mainland China is governed by one party. South Korea is governed through a democratic process. Drastic laws like an overnight ban of for-profit tutoring will be much more difficult.

Second, before the ban, EDU was trading at ~20x NTM P/E. Such high valuation meant there was little margin of safety for investors.

Whereas today MegaStudyEdu is trading at only 4x NTM P/E. If a ban wipes out 50% of its earnings, the company will still trade at an undemanding 8x NTM P/E.

AI disruption. I believe this risk is low.

The lecturers on MegaStudyEdu are not just teachers. They are celebrities.

According to Korea JoongAng Daily, “The relationship between students and star lecturers is similar to the one between fans and K-pop stars. Students even buy merchandise that includes bags, mugs and stickers.”10

The teachers not only teach, but they motivate, entertain, console and even admonish.

Factors that could lead me to increase investment

MegaStudyEdu grows its revenue more than mid-single digit per year (e.g. strong inflection in the growth of advance payment from customers).

Indicators of a potential sale of the business (e.g. higher legal and consulting fees).

Share price falls > 30% without significant deterioration in business fundamentals.

Factors that could lead me to decrease investment

Unfavourable regulatory developments (e.g. lawmakers proposing new laws to ban private education)

Substitutes gaining traction (e.g. government reviving Neulbom Schools and expanding its coverage)

Upcoming events

Tue 11 Aug 2026: Q2’26 earnings release (expected)

Valuation model

Subscribers may request a free copy of my valuation model by emailing me at angsana.anderson@gmail.com.

I will send out my model by the end of Sun 14 Jun 2026.

Coming up next

The IDX Composite, an index of all stocks listed on the Indonesia Stock Exchange, has fallen -31% year-to-date. This is in response to seemingly erratic policymaking in the country.

Despite the chaos, could there be opportunities in Indonesia?

I will explore this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I hold shares in 215200. I may change my views, predictions, or personal portfolio positioning at any time without notice.

Very interesting, I like it! Great case of the market dismissing a stock without looking at the details - that it's actually growing.

One point here is the Korean withholding tax on dividends, it's 22% I believe and reduced to 15% by double taxation agreements for some countries (but not for me). For a stock where the dividend is a significant part of the return, paying 22% tax does makes a big difference over the longer term.

In Singapore and Malaysia (and actually also the UK) the withholding tax is zero making these markets more attractive. Yet, could be worth it investing in a high dividend payer in Korea if the investment thesis is good enough, which might be the case here.