lululemon: A quality compounder on sale?

[First Take] lululemon athletica inc. (LULU US)

Summary

I decided to pass because international growth looks more fragile than expected.

Near-term demand still looks weak.

Corporate governance is unstable, making any turnaround look unlikely.

About (18 May 2026)

Share price: USD 120.26

Market capitalisation: USD 13,710 mn

Enterprise value (EV): USD 13,701 mn

Average daily volume (ADV): USD 346 mn

NTM P/E: 10x

Time spent: ~2 days

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Pass

Background

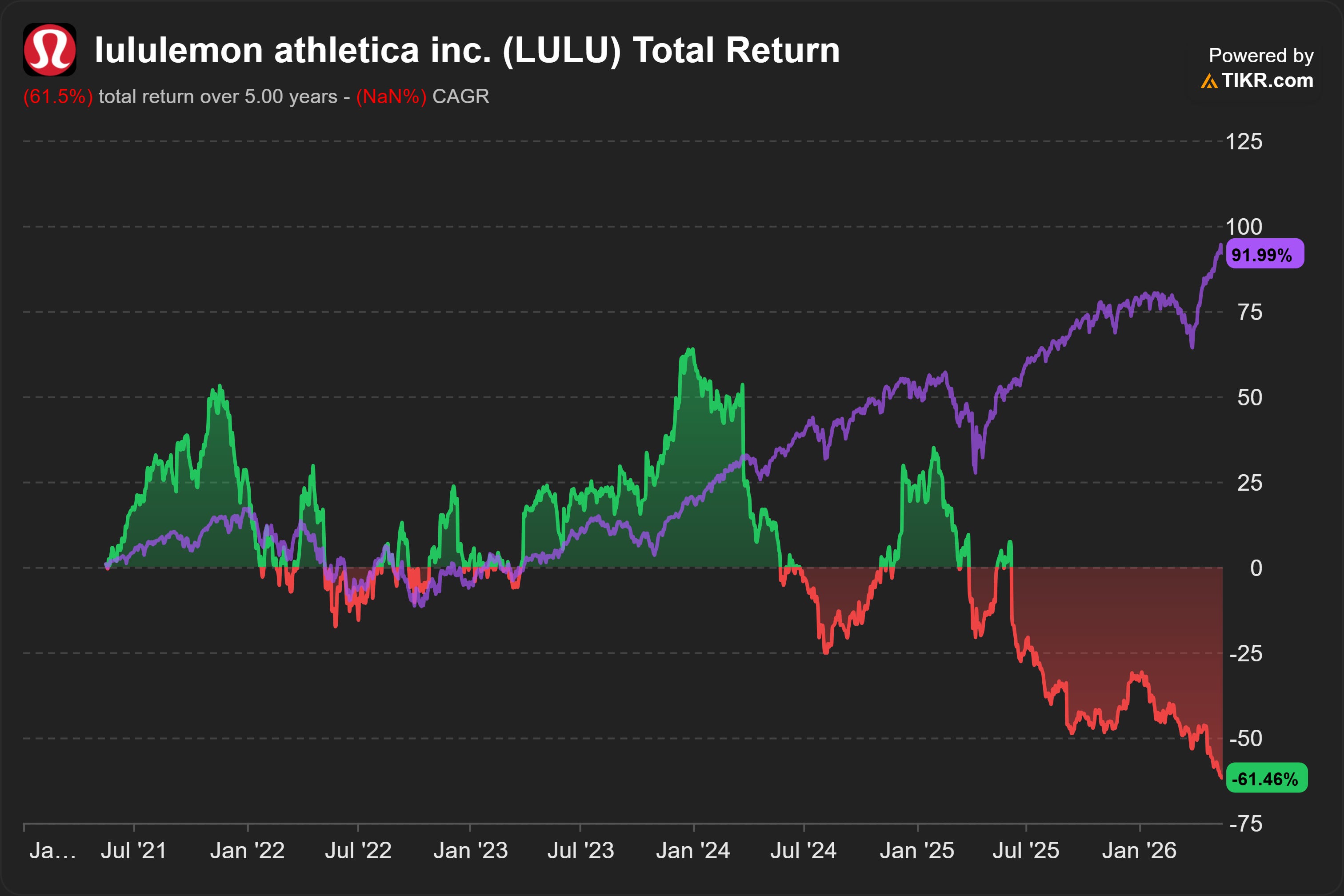

lululemon: A quality compounder on sale?

lululemon was a ‘quality compounder’.

Since 2013, it has always traded around 20x NTM P/E. At its peak during COVID-19 lockdowns, its NTM P/E breached 80x.

Today, lululemon athletica inc. (LULU US) is selling for only 9x NTM P/E. This is despite its +29% revenue growth and 40% operating profit margin in mainland China.

Could this be the bargain of our lifetime?

Green/red: LULU; Purple: SPY (SPDR S&P 500 ETF Trust)

Business model

LULU’s financial year ends on the Sunday closest to January 31 of the following year. Unless stated otherwise, all time references will follow the company’s financial year. For example, FY2025 refers to the year ending on 1 Feb 2026.

Breakdown of FY2025 revenue (USD 11 bn; +5% YoY):

63% Women’s apparel (+5% YoY)

24% Men’s apparel (+4% YoY)

13% Accessories and others (+8% YoY)

LULU sells pants, shorts, tops, and jackets designed for a healthy lifestyle including athletic activities such as yoga, running, and training.

In FY2025, 71% of revenue comes from the Americas, 16% from Mainland China and 14% from the rest of the world.

Mainland China is the fastest growing region, with +29% YoY growth, followed by the rest of the world (+16% YoY). Revenue from the Americas shrank -1% YoY.

There is some supplier concentration. In FY2025, 48% of fabrics were produced by LULU’s top five fabric suppliers, with the largest manufacturer producing 20%. During 2025, 34% of the company’s fabrics originated from Taiwan.

Public comparables include Nike, Inc. (NKE) and adidas AG (ADS).

My reasons

International growth at risk

The Americas shrinking, mainland China growing. In FY2025, revenue from the Americas declined 1% YoY, driven by -3% decline in comparable sales. Operating profit margin (OPM) declined from 38% in FY2023 to 33% in FY2025.

Sales in mainland China grew +29% YoY, driven by +20% growth in comparable sales. OPM improved from 35% in FY2023 to 40% in FY2025.

The bulls argue that even though the Americas is shrinking, LULU is still undervalued because its international segment, especially mainland China, shows tremendous growth potential.

Profits attracting competition. However, I am less optimistic. It is no secret that mainland China is an extremely competitive market. You have probably heard of 内卷 (involution), a self-defeating cycle of excessive competition where companies invest more effort and resources for diminishing returns.1

40% OPM is very high in the industry. It is bound to attract competition.

Vuori, LULU’s fierce competitor in the US, entered China in 2024 and is expanding its store network to compete with LULU. Another competitor, Alo, is planning flagship stores in Beijing and Shanghai, slated for the second half of calendar 2026.2 ANTA Sports Products Limited (2020 HK) is repositioning Maia Active in 2026 as a more direct domestic challenger to LULU.3

Limited patents. It is not clear to me that LULU can fend off these challengers.

In its latest 10-K, LULU warns that “The intellectual property rights in the technology, fabrics, and processes used to manufacture our products generally are owned or controlled by our suppliers and are generally not unique to us.”

LULU adds, “We hold limited patents and exclusive intellectual property rights in the technology, fabrics or processes underlying our products. As a result, our current and future competitors are able to manufacture and sell products with performance characteristics, fabrics and styling similar to our products.”

Eclat Textile Co., Ltd. (1476 TT) is a top supplier. It helped LULU develop its signature Luon fabric, as well as newer materials. In 2017, Bloomberg reported Eclat is helping Amazon.com, Inc. (AMZN US) to make a new line of private-label athletic wear.4 Chip Wilson, LULU’s founder, reportedly regretted not buying Eclat back in 2011.5

These competitive pressures will likely only show up in the long-term. In the near-term, however, demand still looks weaker than expected.

Near-term demand still looks weaker than expected

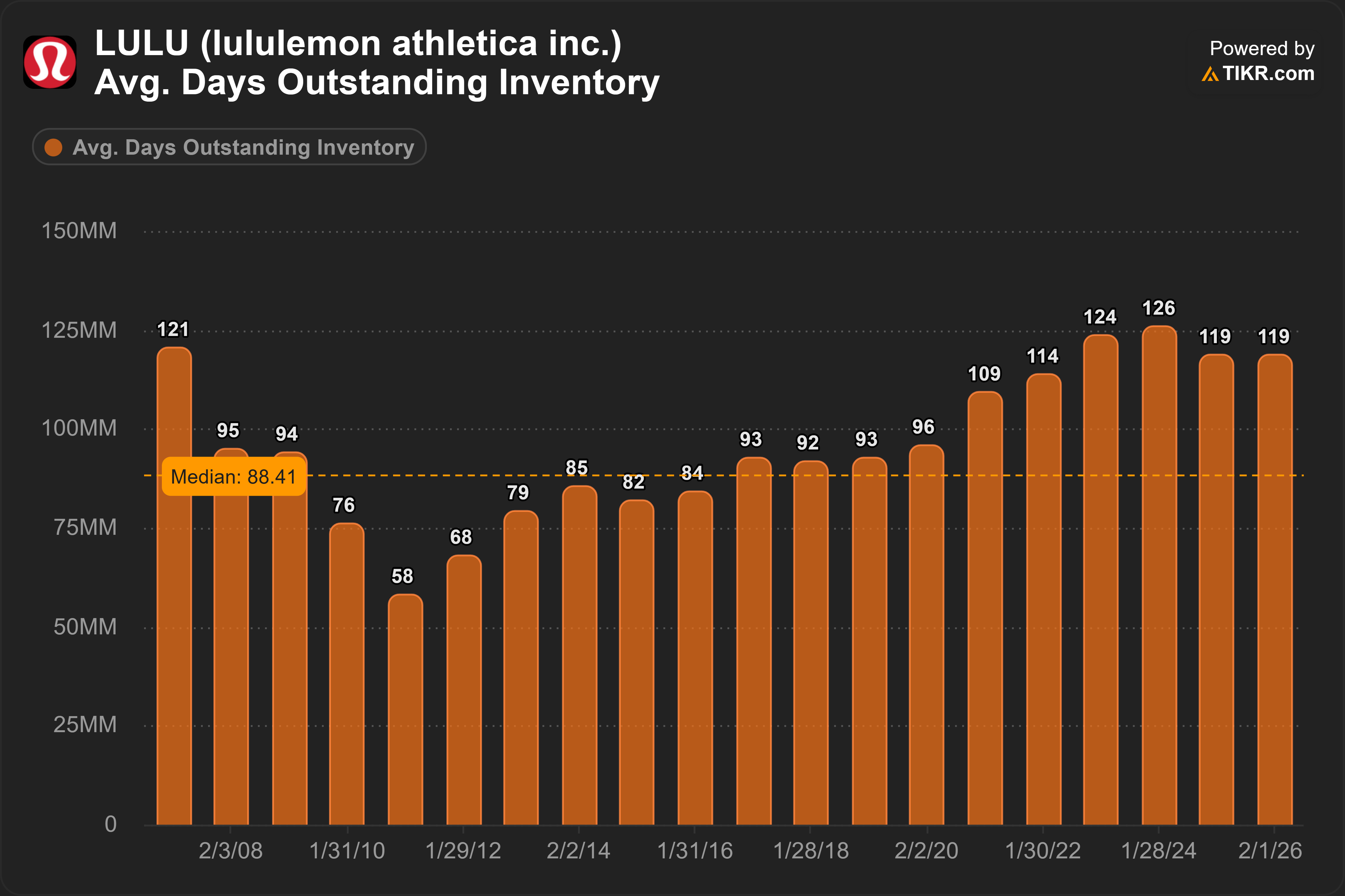

Inventory days stabilized. At first glance, near-term demand seems to have steadied. Average inventory days appear to have stabilized at around 119 days.

But driven by heavier discounting and advertising. LULU increased its advertising expense from 4.5% of revenue in FY2023 to 5.6% in FY2025.

LULU reported credit card affiliate programs, a form of discount for credit card users, helped drive higher e-commerce traffic in the Americas. FY2025 seems to be the first year LULU used such programs.

The heavier discounts and advertisements contributed to overall OPM declining from 23% in FY2023 to 20% in FY2025.

It seems to me the stabilization of inventory days was driven by heavier discounts and advertisements rather than significant improvement in demand.

Absent a demand recovery, LULU faces steeper-than-expected margin compression to complete normalising its inventory levels.

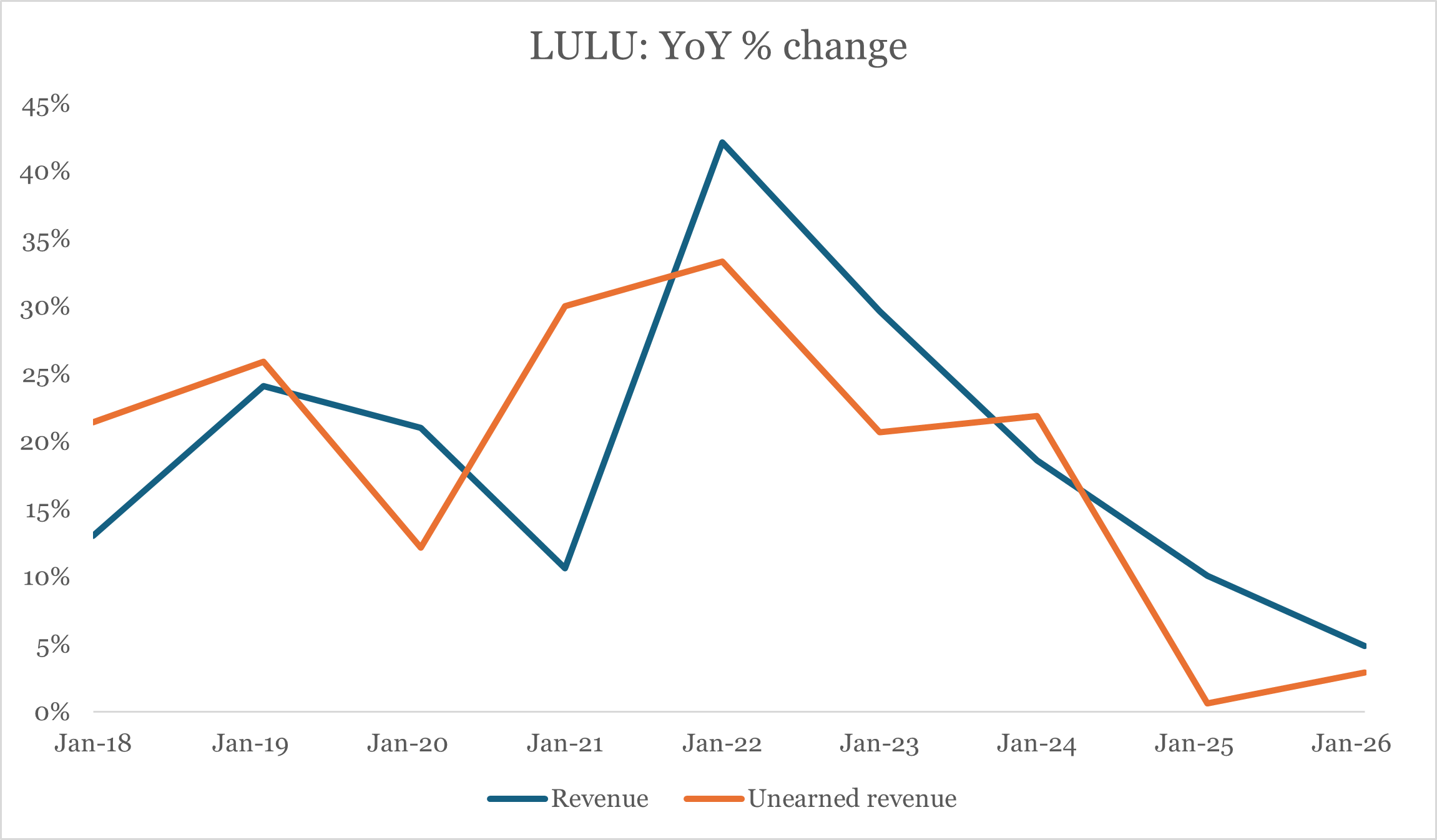

No strong inflection in contract liabilities. LULU’s contract liabilities mainly consist of unredeemed gift cards. Historically, the YoY % change has been a leading indicator of revenue growth:

Source: Angsana Anderson’s estimates using Tikr

In FY2025, unredeemed gift cards grew +3%, up from +1% during the prior year.

However, the cash inflow from unredeemed gift cards declined -3% in FY2025, suggesting the underlying demand remains weak. The +3% increase in unredeemed gift cards was likely due to timing effects (e.g. customers delaying the redemption of their gift cards).

Corporate governance looks unstable

Board needs more suitable experience. Out of the 11 board members, only 4 have direct operational experience in apparel or fashion.

In FY2020, LULU acquired Mirror, a maker of in-home fitness equipment.6 LULU paid USD 500 mn, about 71% of the prior year’s operating income. By FY2022, LULU had written down the value of its investment by USD 443 mn.7

Out of the 10 board members that oversaw LULU at the time of the acquisition, 5 remained on the board of directors today.

I suspect this is one of the reasons why Chip Wilson, LULU’s founder, is fighting a public proxy battle to install new board members.

New CEO is unproven. After CEO Calvin McDonald stepped down in Jan 2026, the board appointed Heidi O’Neill as the new CEO.

According to Piper Sandler, an investment bank, “Investors likely remember O’Neill most as the key part of John Donahoe’s tenure (2020-2024) that was marked by a push towards DTC as well as declining innovation, strained retail partnerships and a falling share price”8

I am surprised the board did not appoint a CEO with proven track record in turnarounds.

Activist investor Elliott Investment Management suggested Jane Nielsen, the former CFO and COO of Ralph Lauren. Nielsen built her reputation when she helped turn around Ralph Lauren Corporation (RL US).9

Difficult turnaround. Retail is a tough business, especially fashion retail. It’s hard to gain any sustainable structural advantage. If you are doing well, competitors can walk into your stores and copy your innovation. That’s an oversimplification, but you get my idea: management is very important.

With LULU’s founder fighting a high-profile proxy battle and an aggressive activist investor at the gates, management may struggle to find enough time and resources to turnaround the business.

Factors that could lead to a re-assessment of my decision

Strong evidence of durable competitive advantage (e.g. patented fabric)

Early indicators of recovery in demand

Improved corporate governance (e.g. management with proven track record in turnarounds)

Favourable resolution of the proxy battles

Coming up next

Topsports International Holdings Limited (6110 HK) looks like a bargain.

9.6% dividend yield. 9x NTM P/E.

It is one of the largest distributors and retailers of Adidas and Nike sportswear products in mainland China, with revenue market share of ~17%.

Why is a business like this selling so cheaply?

In my next post, I will share my analysis.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in LULU, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.

growing in China and European countries

It's interesting to see that Michael Burry bought 100k shares in LULU. Not sure what he sees in this stock but I agree with you that LULU doesn't seem to be a good buying opportunity.