Kaspi: Pennies in front a steamroller?

[First Take] Joint Stock Company Kaspi.kz (KSPI; KSPI US)

Disclaimer: This is a record of my investment decisions and not financial advice. I may change my decisions at any time without notice. Use this only for educational and entertainment purposes. All analysis and opinions are my own and based solely on public information. KSPI has not reviewed or endorsed this post. Do not rely on this for your investment decisions. I do not hold any positions, long or short, in KSPI.

About

Share price: USD 72.89

Market capitalisation: USD 13,738 mn

Enterprise value (EV): USD 12,828 mn

Average daily volume (ADV): USD 39 mn

NTM P/E: 6x

My Decision

Pass

Background

Kaspi: Pennies in front a steamroller?

Nov 2021. You’re in a stock pitch conference.

After almost two years of COVID-19 lockdowns, you are glad to be back.

After a few pitches, your excitement gradually fades into boredom.

A new speaker takes the stage. “Buy this high-quality, cash-generative compounder! EPS grew +60% but it only trades at 22x NTM P/E!”

You snap to attention. Before the pitch is even over, you have booked the first flight to Kazakhstan. You need to see Kaspi for yourself.

After enduring a PCR test and some interrogation by customs officials, you were finally released into the bustling streets of Almaty.

Kaspi is everywhere. You watch people paying with Kaspi QR codes, then you buy an apple with Kaspi Pay yourself. It feels seamless.

The apple tastes heavenly. In this apple city, have you just found the forbidden fruit: high growth at a low multiple?

Back at the hotel, your conviction is sky‑high. You recall the Buffett disciples saying, “When it rains gold, put out the bucket, not the thimble!”

You call your broker: “I’m all-in!”

Today, you are down -50%. KSPI 0.00%↑ is trading at an unbelievable NTM P/E of only 6x, despite EPS growing 26% p.a. since 2021. What happened?

In this Substack post, I discuss:

Why 22x NTM P/E was never cheap, and that even at 6x, KSPI is not obviously attractive

Why I think the market is still under-pricing key regulatory risks

Why the chairman’s personal purchase of another bank creates a serious conflict of interest

Business model

Breakdown of 2025 revenue (KZT 4,043 bn, +59% YoY):

16% Payments (+12% YoY revenue)

47% Marketplace (+164% YoY revenue)

37% Fintech (+20% YoY revenue)

Payments revenue includes payments fee revenue (12% of group revenue) and interest revenue (4%).

Payments fee revenue includes transaction revenue and membership revenue.

KSPI earns transaction revenue when it processes payments for purchases both online and in-store and transactions by SMEs and corporate customers.

KSPI recognises membership revenue, which includes annual fees paid by individual customers, SMEs and corporate customers for the use of KSPI’s products and services.

Marketplace revenue includes marketplace fee revenue (24% of group revenue), retail revenue (21%) and others (3%).

Marketplace fee revenue includes seller fees paid by merchants from KSPI’s 3P marketplace business, Kaspi Travel, advertising and delivery transactions.

Retail revenue includes revenue from e-Grocery transactions and related delivery fees. Since 2023, retail revenue also includes revenue from KSPI’s car e-commerce transactions and since 2025 it also includes revenue from 1P business of Hepsiburada in Türkiye.

Fintech revenue includes interest revenue (33% of group revenue) and fintech fee revenue (4%).

KSPI earns interest revenue mainly by lending to customers. It charges interest when customers borrow money directly through KSPI’s app or use credit to buy items on KSPI’s marketplace and other websites.

In 2025, buy-now-pay-later (BNPL) loans make up 41% of the total value of loans issued. 36% of loans are issued for general purposes and 18% of loans are issued for merchant and micro business finance.

Fintech fee revenue mainly includes banking service fees and commissions, which are paid by customers monthly.

KSPI did not provide loans which individually exceeded 10% of the Group’s equity.

The closest public comparable is Halyk Bank of Kazakhstan JSC (HSBK KZ).

My reasons

High interest rates. The bull case: KSPI is a high-growth, cash generative super-app dominant in Kazakhstan. Yet, it trades at only 6x NTM P/E and 7% NTM dividend yield.

However, I believe the consensus is overestimating the attractiveness of KSPI’s valuation.

6x NTM P/E means 17% earnings yield. With Kazakhstan 10y government bond yield at 15%, KSPI now looks expensive.

Why invest in KSPI and earn 17% when you can just invest in Kazakhstan 10y government bond and earn 15%? You are only compensated an extra 2 percentage points for taking on significantly higher risk.

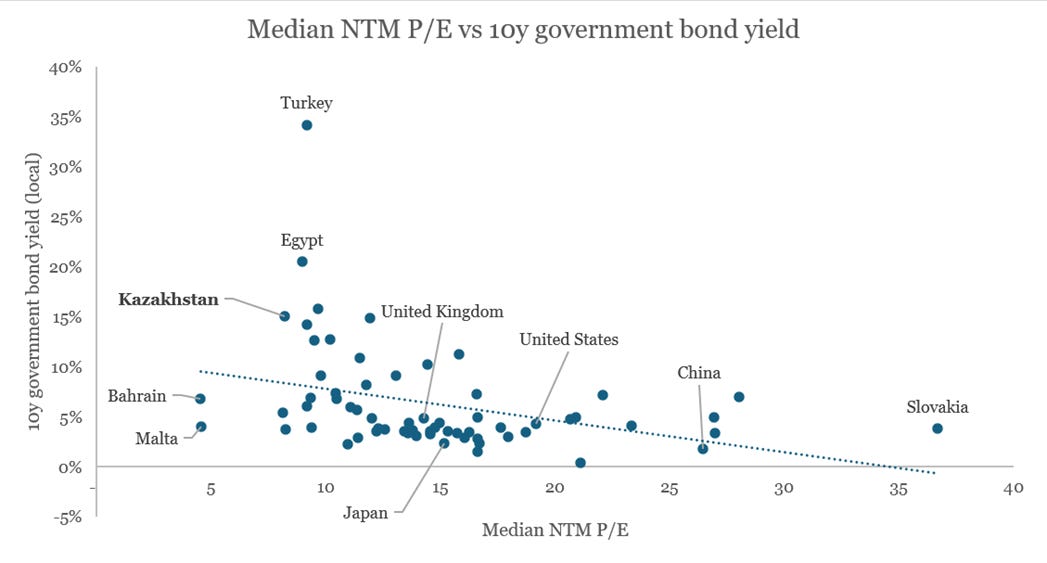

I want to reinforce my point that if government bond yield is high, NTM P/E will naturally be lower. In the graph below, I plotted the median NTM P/E of major economies against their 10y government bond yield.

Source: Aswath Damodaran (2026); World Government Bonds (2026)

With a few exceptions, companies operating in economies with high bond yield will trade at lower levels of NTM P/E. This makes sense. If an investor can get 15% just from government bonds, to attract her to invest in companies, earnings yield will need to be much higher. That means a much lower NTM P/E.

So, in KSPI’s situation, its NTM P/E of 6x is actually not low because Kazakhstan 10y government bond yield is currently 15%.

The bulls will counter-argue that NTM P/E of 6x is attractive because of KSPI’s tremendous growth potential. This brings me to my next point: regulatory risks to growth.

Regulatory risks. The bulls argue that KSPI dominates the payment system in Kazakhstan, handling ~70% of consumer non‑cash payment transactions nationwide. The closest competitor, HSBK KZ processes only ~8%. KSPI’s monopoly supposedly gives it unrivalled data, customer engagement, and pricing power that competitors struggle to match.

I believe the market underestimates the regulatory risks that are threatening KSPI’s growth. KSPI’s monopoly has become its Achilles’ heel.

In Apr 2024, Bloomberg reported that The National Bank of Kazakhstan (NBK), Kazakhstan’s central bank, is looking to break KSPI’s monopoly over payments. Without calling out KSPI specifically, the NBK governor said “That project may lead to less earnings for some banks”1.

By Sep 2025, the NBK has launched a unified QR code system that allows customers to pay with a single QR, regardless of which bank or app they use2.

As of Mar 2026, 15 banks have signed participation agreements, although only 6 have completed technical integration with the system. KSPI has signed the agreement but has not integrated with the system3.

The delay seems to have drawn the ire of the President of Kazakhstan: “The requirement for all banks to connect to this infrastructure is enshrined in law, but the largest banks are delaying compliance”

By law, the remaining banks like KSPI must connect to the unified system by 18 July 2026.

Separately, in 2025, the National Bank of Kazakhstan (NBK) raised reserve requirements on liabilities denominated in KZT to 3.5% (from 0%–2% previously), and on foreign currency liabilities to 10% (from 1%–3%).

As a result, KSPI must hold more reserve assets with the NBK. The NBK does not pay interest on these reserve assets. I estimate this change reduced KSPI’s interest income by ~ KZT 46 bn in 2025.

Separately, the Kazakhstani government introduced a 10% tax on revenue from government securities, leading to an additional KZT 14 bn in tax expenses.

Taken together, shareholders have lost ~ KZT 60 bn from unfavourable regulation and taxation.

Although KZT 60 bn is only ~6% of 2025 net profit after tax, this highlights the underappreciated risk of investing in frontier markets like Kazakhstan. The governments are more inclined to see banks as piggy banks.

What’s more, from Apr 2026 the NBK is set to raise reserve requirements further. By Sep 2026, reserve requirements are expected to reach up to 5.0% (from 3.5% currently) for liabilities denominated in KZT and up to 15.0% (from 10.0% currently) for liabilities denominated in foreign currency.

I suspect this is why, despite having so much cash, KSPI chose to finance its acquisition of Hepsiburada through a combination of debt and dividend cuts.

Conflict of interest. In Jul 2025, Chairman Kim acquired Alatau City Bank in his personal capacity4. Alatau City Bank, formerly Jusan Bank, is the sixth largest bank by assets in Kazakhstan.

Chairman Kim announced he plans to transform the bank into a “fundamentally new financial institution” in Kazakhstan, with a focus on the introduction of the state-of-the-art IT solutions5.

According to people familiar with the matter, Alatau City Bank’s strategy will be tailored to limit competition with Kaspi.kz in the future by concentrating on extending loans to businesses and collateralized lending to individuals, such as mortgages, instead of retail banking6.

I did not find any formal contracts to mitigate this conflict of interest. In any case, even if there are contracts, I am not confident of their enforceability. If foreign shareholders are fleeced, there is little recourse. The US and Kazakhstan have no extradition treaty nor any deal to enforce each other’s civil or commercial court judgments.

Factors that could lead to a change in my decision

1. Significant decline in Kazakhstan 10y government bond yield or decline in KSPI’s valuation without significant deterioration of business fundamentals

2. Evidence that the regulatory environment has become more friendly to shareholders

3. Enforceable formal contracts that reduce conflicts of interest

Subscribe for 2 to 3 analyses of global equities every week. Discover overlooked ideas and rethink familiar names. Published by Andrew Wong, ACA, CFA

I will preface that Kaspi is my biggest holding. You raise several good points. Here are my thoughts:

Kaspi already yields 2% more than the bond yield, as you mentioned, without accounting for any future growth…I will take that optionality. Kaspi has compounded earnings for many years despite different interest rate cycles.

Reserve requirements: These changes will negatively impact Kaspi's banking unit for 2026. However, there could be a benefit as well. Banking risk is reduced, and the rule may curb inflation (which is the stated goal by the government). Lower inflation would mean lower rates, which is a bigger headwind for the company.

Altau Bank is owned by a key Kaspi shareholder and chairman. Altau is a development bank for a planned city, offering real estate loans. Kaspi is a consumer bank offering small personal loans. They don't overlap. The majority of the chairman's net worth is tied up in Kaspi, why would they harm it? In fact, history has shown the opposite. Big owners have sold pieces of their personal businesses to Kaspi (like Magnum groceries), at attractive prices. The “conflict of interest” has been value-added in the past.

The national QR payment system still allows payment processors to set their own prices and have their own interface. It just allows interoperability on payment terminals. I don't think the impact will be that great, since Kaspi’s strength is it's focus on customer experience. They have the best tech and ecosystem.

Conclusion: Kaspi yields 10% dividends which are secured by a strong moat. It offers significant growth upside in Turkey if their superapp model can be replicated.

Very useful devil’s advocate, thanks. One thought: even absent further growth, the govt bond yield is nominal whereas Kaspi’s earnings yield is real (inflation-linked). In the long term I’d say equities are safer than govt bonds - certainly was the case in Argentina! I take your point, though.