[First Take] Jiayin Group Inc. (JFIN; JFIN US)

I decided to pass because of (a) hidden exposure to credit risks; (b) significant regulatory risks; (c) unusually large purchase of headquarters...

Disclaimer: This is a record of my investment decisions, not financial advice. I may change my decisions without notice. Use this only for education and entertainment. Do not rely on this for your investment decisions.

About

Share price: USD 6.55

Market capitalisation: USD 350 mn

Enterprise value (EV): USD 337 mn

Average daily volume (ADV): USD 971 k

NTM P/E: 4x; LTM P/B: 0.6x

Time spent: ~3 hours

My Decision

Pass

Background

Jiayin Group Inc. ($JFIN; JFIN US) looks like a bargain.

The share price is down ~65% from its peak in 2025. Valuation metrics looks attractive: 4x NTM P/E, 0.6x LTM P/B. Since 2016, revenue grew 14% p.a and EPS grew 9% p.a. JFIN achieved ~14% return on asset. JFIN looks like a ‘quality compounder’ selling at a bargain.

I decided to pass because (a) it has hidden exposure to credit risks; (b) significant regulatory risks; (c) unusually large purchase of headquarters; (d) continued increase in receivable days from an already elevated level and (e) auditor with a chequered history.

In my Substack post, I walk through these factors in detail. I also explain what metrics and analytical techniques helped me realise the risks hidden in JFIN.

For more analysis like this, click on the link below and subscribe to my Substack.

Business model

Breakdown of 2024 revenue (RMB 5.8 bn, +6% YoY):

69% from loan facilitation services (+15% YoY)

23% from the release of guarantee liabilities (-3% YoY)

8% from others (-26% YoY)

Revenue from loan facilitation services is earned through facilitating loan transactions between borrowers and institutional funding partners. JFIN’s service mainly consist of performing credit assessment on the borrowers, referring qualified borrowers to the institutional funding partners, and facilitating the execution of loan agreements between the parties.

According to JFIN, “The stand-ready guarantee liabilities are released into guarantee revenue over the term of the guarantee”. To be honest, I still could not understand this completely. More on this later, when I discuss JFIN’s hidden exposure to credit risks.

Other revenues primarily include service fees charged to the third-party financial service providers for the referral service of borrowers, and interest income generated from loan services to overseas individuals. It also includes referral services in respect of investment products offered by third-party financial service providers on Youdao wealth platform, a proprietary platform operated by JFIN.

As of 2024, one customer accounted for 28% of accounts receivable and contract assets.

Relevant public comparables include Qfin Holdings, Inc. (QFIN; QFIN US) and X Financial (XYF; XYF US).

My reasons

Hidden exposure to credit risks. JFIN bulls usually argue that JFIN is a superior business because it operates an asset-light business model. Rather than deploying its own capital, it operates as a matchmaker between ‘underserved’ borrowers with institutional lenders.

This is no longer true. Note 2 (k) of JFIN’s 2024 20-F disclosed that “Starting from the fourth quarter of year 2022, the Group provides guarantee services… the Group effectively takes on all of the credit risk of the borrowers…”1

Furthermore, the guarantee services are complex. I’ve read note 2 (k) several times, but I still don’t fully understand what’s going on. It seems like when JFIN facilitates a loan, a third-party licensed financing guarantee company will provide a guarantee on the loan to the institutional lender. JFIN will then provide a back-to-back guarantee to the third-party guarantor. Next, JFIN will also engage another third-party company to provide back-to-back guarantee service to JFIN. In total, there can be up to 3 back-to-back guarantors for 1 loan. This appears unnecessarily complex to me.

Significant regulatory risks. According to the Economist, unsecured lenders rely on very aggressive collection tactics and usury2. JFIN is no exception. A Chinese media outlet alleged JFIN continued to charge fees that far exceed new regulatory limits3. A Chinese forum showed widespread complaints over JFIN, focusing on three major issues: (a) usury; (b) aggressive debt collection tactics and (c) hidden fees4.

Unusually large purchase of headquarters. In Dec 2024, JFIN announced it purchased a commercial property in Shanghai for RMB 1.4 bn (~25% of revenue)5. The property is ~43,500 sqm. JFIN said this will be “used as the Company’s new headquarters to meet the demand arising from the continuing growth of the Company’s businesses.”

If each employee occupies 10 sqm (the average in Shanghai), 43,5000 sqm can fit ~4,350 employees. JFIN only has ~1,000 employees now.

Why does JFIN need such a large headquarter? During its Q3’25 earnings call in Nov 2025, JFIN reported ‘industry contraction and tightening liquidity…’. Is it realistic to expect 4x increase in employee headcount when the industry is contracting?

Elevated receivable days continues to increase. Average receivable days increased from 97 days in 2017 to 195 days in the last twelve months (LTM). Why did average receivable days increase so much? Why is JFIN taking >6 months to collect from its customers?

Auditor with chequered history. Marcum Asia CPAs LLP (Marcum Asia) served as JFIN’s auditor from 2021 to 2023. Marcum Asia was a joint venture between Marcum LLP and Bernstein & Pinchuk LLP. In 2023, the U.S. Securities and Exchange Commission (SEC) charged Marcum LLP for widespread quality control deficiencies. According to the SEC, “Marcum’s deficiencies were not limited to SPAC clients, but they reflected systemic quality control failures throughout the firm.”6

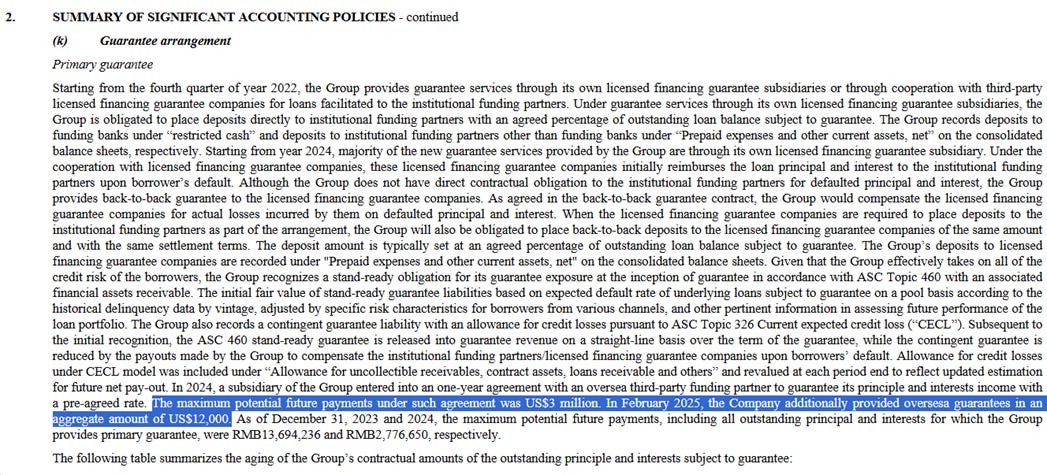

You could argue this is no longer a risk because in 2024, JFIN appointed Deloitte, a Big 4 audit firm to replace Marcum Asia. However, there are subtle signs that the audit work was rushed. I found typos like ‘oversesa’, inconsistent reporting currencies (switching between RMB and USD) and mismatched units like US$3 million vs US$ 12,000. This happened in the ‘Summary of significant accounting policies’, a section where you would normally expect a high level of rigour.

Source: 2024 JFIN 20-F

For more analysis like this, subscribe to my Substack

嘉银科技荣获“最具投资价值中概股”奖

消费者报道

2023-12-12 14:53

https://m.sohu.com/a/743434135_100661/?pvid=000115_3w_a

QFIN has employee 3000+.

.

It makes sense for JFIN to acquire larger office if the future high growth expansion prospect is foreseen by the management.

.

Finger crossed.