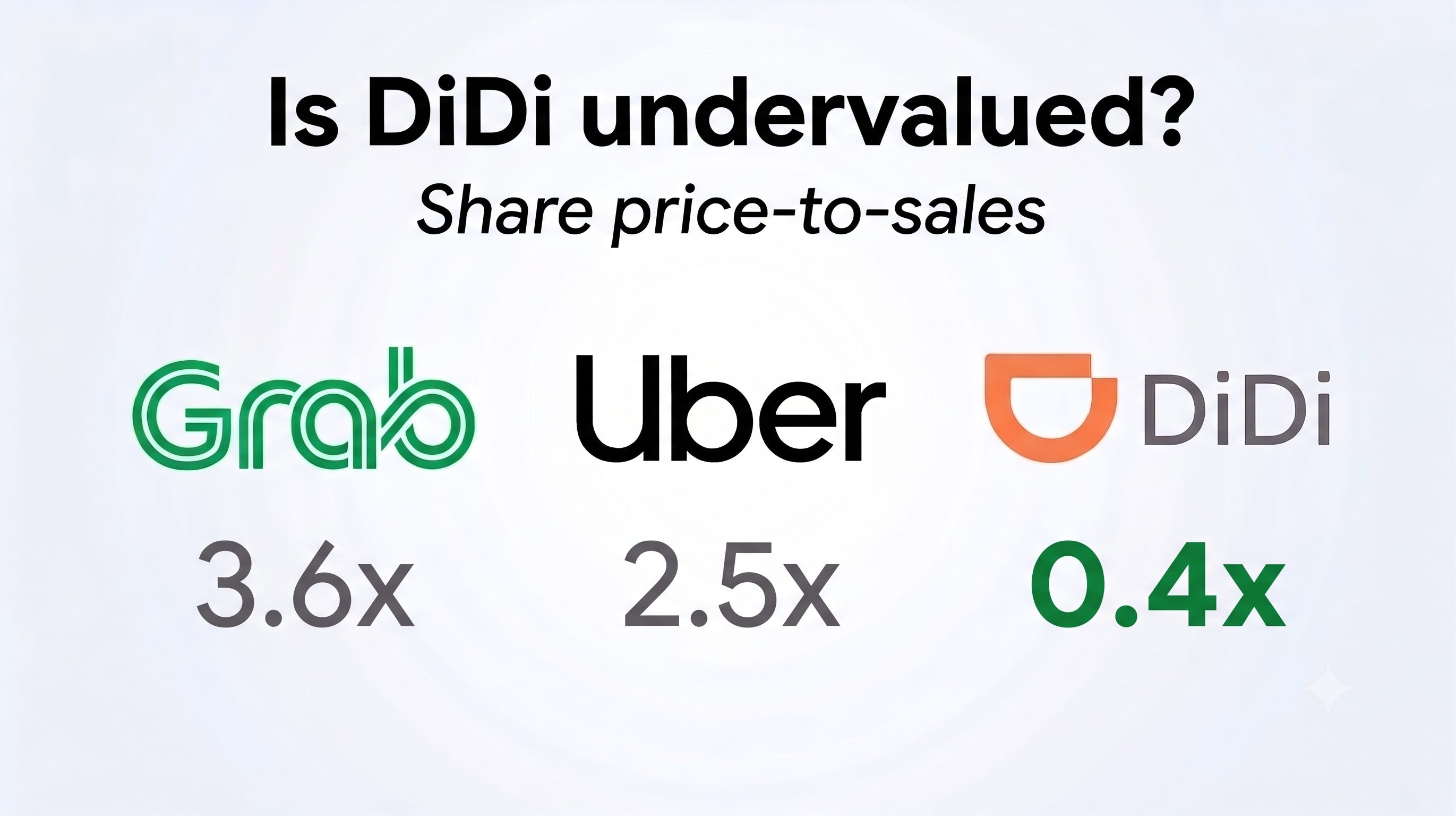

Is DiDi dirt cheap at 0.4x price-to-sales?

GRAB and UBER trade at 3.6x and 2.5x

Listen, Angsana. I’ve got a stock tip for you.

DiDi!

That’s the largest ride-hailing app in mainland China, isn’t it?

I’ve already loaded up my portfolio on this.

Why would you do that?

DiDi is so cheap.

It trades at only 0.4x price-to-sales, so cheap.

Grab and Uber are trading at 3.6x and 2.5x. DiDi is undervalued by at least 6 times, so cheap!

You cannot compare their sales like that. But never mind…

You remind me of someone. Once he starts chirping like a bird, there’s nothing on earth you can do to change his mind.

Come on! Tell me about it. I am open-minded.

Imagine you are a real estate agent. You sold a house for $1,000,000. You earned $50,000 commission. What is your revenue?

$50,000, obviously.

Why not $1,000,000?

Don’t be ridiculous. The agent does not own the house. She is merely in charge of selling it. Recognising the entire $1,000,000 is clearly overstating the size of her business.

Exactly.

The accounting standards make this clear. If you control the house, you recognise the $1,000,000. If you are only in charge of arranging the sale of the house, you recognise only your $50,000 commission.

What are the key indicators of control?

First, who has the primary responsibility for fulfilling the promise? If the windows are broken, who will be responsible for repairing them before the buyer takes the keys?

Second, who has inventory risk? If the house burns down today, who will suffer the loss?

Finally, who decides the price?

The answer is clearly the houseowner. The agent can advise on the market price, but it is the houseowner who ultimately decides what price she wants to sell.

What does this have to do with DiDi?

Ride-hailing apps face the same issue.

Let’s say your ride costs $100. $30 goes to the app and the remaining $70 goes to the driver.

How much revenue should the app recognise? $100 or $30?

Obviously, $30. That’s their commission.

Yes and no.

In most of their markets, Grab and Uber recognise their commission, $30.

Grab and Uber do not control the delivery of the rides. That’s the responsibility of the drivers. Grab and Uber see the drivers as independent contractors, not employees. Their apps merely connect these contractors with riders.12

Even though Grab and Uber facilitate price-setting, the drivers ultimately decide whether to accept or decline the price.

How about DiDi?

This is where it gets interesting.

DiDi takes a different approach from GRAB 0.00%↑ and UBER 0.00%↑.

In mainland China, DiDi recognises the entire $100 as revenue and records the driver’s share ($70) as cost of sales.

Why?

DiDi says the regulations in mainland China require online ride hailing platforms to take full responsibility for the ride services.3

As a result, DiDi controls the services provided to riders.

For example, if a driver cannot complete the ride, DiDi is responsible and will direct other drivers to complete it.

So, Grab and Uber mostly recognise revenue after deducting drivers’ fees, while DiDi recognises revenue before deductions.

That’s right.

In accounting parlance, we say DiDi is a principal. It controls the goods and services. It recognises gross revenue.

Grab and Uber are agents. They are only in charge of arranging the sale. They recognise net revenue.

That’s too much accounting for me. I am an investor, not an accountant.

Many investors think accounting is not important. But if only they had scrutinised how Enron recognised revenue, they would have dodged the big bullet.

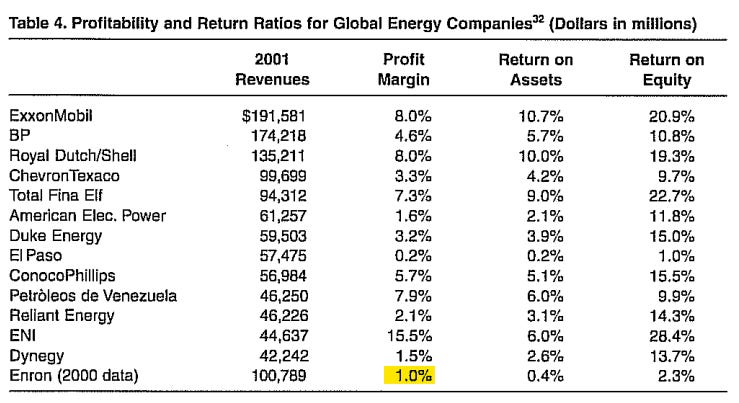

In 1995, Enron reported ~ $9 bn in revenue. By 2000, its revenue had skyrocketed to over $100 bn, making it the 7th largest company on the Fortune 500.

But this explosive growth was largely an accounting illusion.

Enron was a middleman matching buyers and sellers of energy contracts. Its peers operated under the agent (net) model. If a bank brokered a $1 mn trade and took a 1% cut, they reported $10,000 in revenue.

Enron, however, aggressively exploited accounting. The company temporarily took title to the contracts before the trade closed. By virtue of that, they argued they are the principal and they should recognise gross revenue.

Therefore, if Enron brokered that same $1 million trade and made a $10,000 commission, they didn’t report $10,000. They reported $1,000,000 as top-line revenue.4

Wow! But these kinds of accounting issues are so difficult to catch.

It is actually quite easy to spot.

The hint is unusually low margins.

Source: Dharan and Bufkins (2004)

Enron reported unusually low profit margins, despite revenues comparable to the top global energy companies.

Whether revenue is reported as gross or net, profits remain the same. But when you report gross revenue, you inflate the denominator of your profit margin formula, causing your margins to be abnormally low.

Both Grab and Uber reported gross margins ~39%. However, DiDi’s gross margin is only 16%.

So, DiDi is like Enron?

No, no, no… That’s not what I am saying.

There is no evidence that DiDi is doing anything wrong. If the law requires them to be the principal, then they are rightfully recognising gross revenue.

All I am saying is we cannot conclude DiDi is so much cheaper simply because its price-to-sales ratio is only 0.4x.

For a more accurate comparison, we need to use DiDi’s net revenue.

Once we adjust to net revenue, DiDi’s price-to-sales ratio is closer to 2.7x. This is not that much different from Uber’s 2.5x and Grab’s 3.6x.

DiDi is …

Wait, where are you going?

Cheap, cheap, cheap, chip, chip, chip…

Coming up next

Among the 3 interesting ideas I shared, you voted Craneware plc (CRW LN) the most interesting.

I agree.

The recent sell-off seems to have squeezed out all optimism.

However, there is a chance that CRW’s headwinds are temporary. Unearned revenue returned to growth (+2% YoY) in H2’25.

Bain Capital offered GBP 26.50 per share in May 2025. The board rejected it. If private equity likes it at GBP 26.50, they’ll like it even more at GBP 11.10?

Is there an opportunity for us? That’s what I will explore next.

But first, I will share 3 more interesting ideas next Monday.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in GRAB, UBER and DIDIY, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.

Excellent! Thanks for this:-)