iFAST: Singapore’s homegrown fintech, penetrating Hong Kong and beyond

[First Take] iFAST Corporation Ltd. (AIY; IFAST SP)

Summary

I passed on iFAST, Singapore’s homegrown fintech.

The business is what many investors would describe as a high quality compounder.

Indeed, iFAST has grown its revenue by 36% p.a. and EPS by 131% p.a. over the past 3 years.

However, I am not sure why customers are now taking more than 300 days to pay iFAST. I am also not sure about the durability of the profits from its UK banking subsidiary.

Finally, iFAST seems overvalued relative to global comparables. The consensus seems to be underestimating the industry’s cyclicality.

About (22 Jun 2026)

Share price: SGD 9.15

Market capitalisation: SGD 2,786 mn (USD 2,154 mn)

Enterprise value (EV): SGD 1,799 mn (USD 1,391 mn)

Average daily volume (ADV): SGD 11 mn (USD 9 mn)

NTM P/E: 23x

Time spent: ~2 days

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Pass

Background

Is iFAST Corporation Ltd. (AIY; IFAST SP) overvalued?

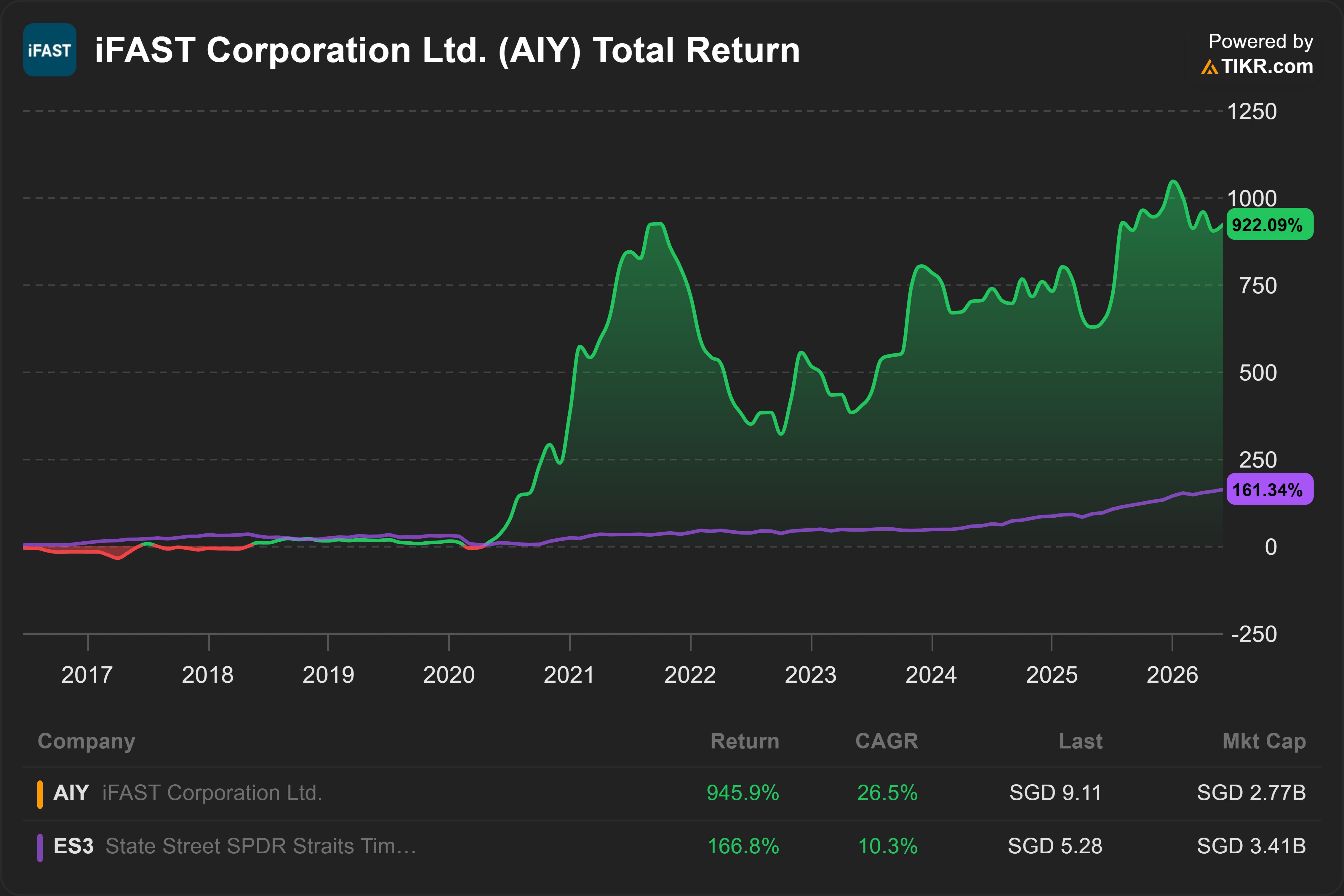

Over the past 10 years, shareholders have been rewarded with ~27% p.a. total return.

Today, IFAST trades at 23x NTM P/E. It targets SGD 100 bn assets under administration by 2030. Its UK banking division just turned profitable.

However, I have some questions.

Why did receivable days increase so much?

Why are global peers like Allfunds Group plc (ALLFG NA) trading at only 18x NTM P/E?

Business model

Estimated breakdown of 2025 net revenue (SGD 340 mn; +37% YoY):

39% iFAST ePension (+65% YoY)

38% Business-to-Business (B2B) Wealth Management (+18% YoY)

12% Business-to-Consumer (B2C) Wealth Management (+10% YoY)

11% iFAST Global Bank (+64% YoY)

iFAST is a global digital banking and wealth management platform with assets under administration (AUA) of SGD 33 bn as of 31 Mar 2026.

The iFAST ePension segment provides pension administration services and white-labelled solutions to enable digital access, management and processing of pension scheme transactions.

This segment is the prime subcontractor for the eMPF Platform project. This project, funded by the Hong Kong government, aims to create a digital experience for the city’s Mandatory Provident Fund (MPF) system.1

The Wealth Management segment provides access to investment products such as unit trusts, bonds, stocks, and ETFs. This segment connects product providers like fund houses with Business-to-Consumer (B2C) self-directed investors and Business-to-Business (B2B) partners, such as financial advisory firms and banks.

The most important source of revenue here is trailer fees. This is a recurring fee paid by fund houses to iFAST for distributing their investment products, typically calculated as a percentage of the AUA held on iFAST’s platform.

The iFAST Global Bank segment is a fully licensed UK bank acquired in 2022.

In 2025, iFAST earned 51% of its net revenue from Hong Kong, 33% from Singapore, and 11% from the UK. Malaysia contributed 5% while China’s revenue is immaterial.

The UK and Hong Kong were the fastest-growing markets, with +64% and +52% YoY net revenue growth respectively. China and Malaysia grew more slowly, at +24% and +14% YoY. Singapore grew +16%.

Unit trusts make up 56% of AUA. Stocks & ETFs contribute 24% while bonds contribute 11%. The remaining 9% is held in cash accounts and deposits.

The most relevant public comparables are Allfunds Group plc (ALLFG NA) for B2B and Futu Holdings Limited (FUTU US) for B2C.

My reasons

Why are customers taking so long to pay?

Revenue and profits are growing. The bull case involves high growth. In the past 3 years, iFAST has grown its revenue by 36% p.a. EPS grew even faster, at 131% p.a.

iFAST’s growth was mainly driven by strong net inflows in AUA and its involvement in Hong Kong’s eMPF Platform project.

But little cash. Despite growing profits, iFAST seems to need more cash. iFAST borrowed a combined SGD 220 mn in Jun 2024 and Mar 2026. Why?

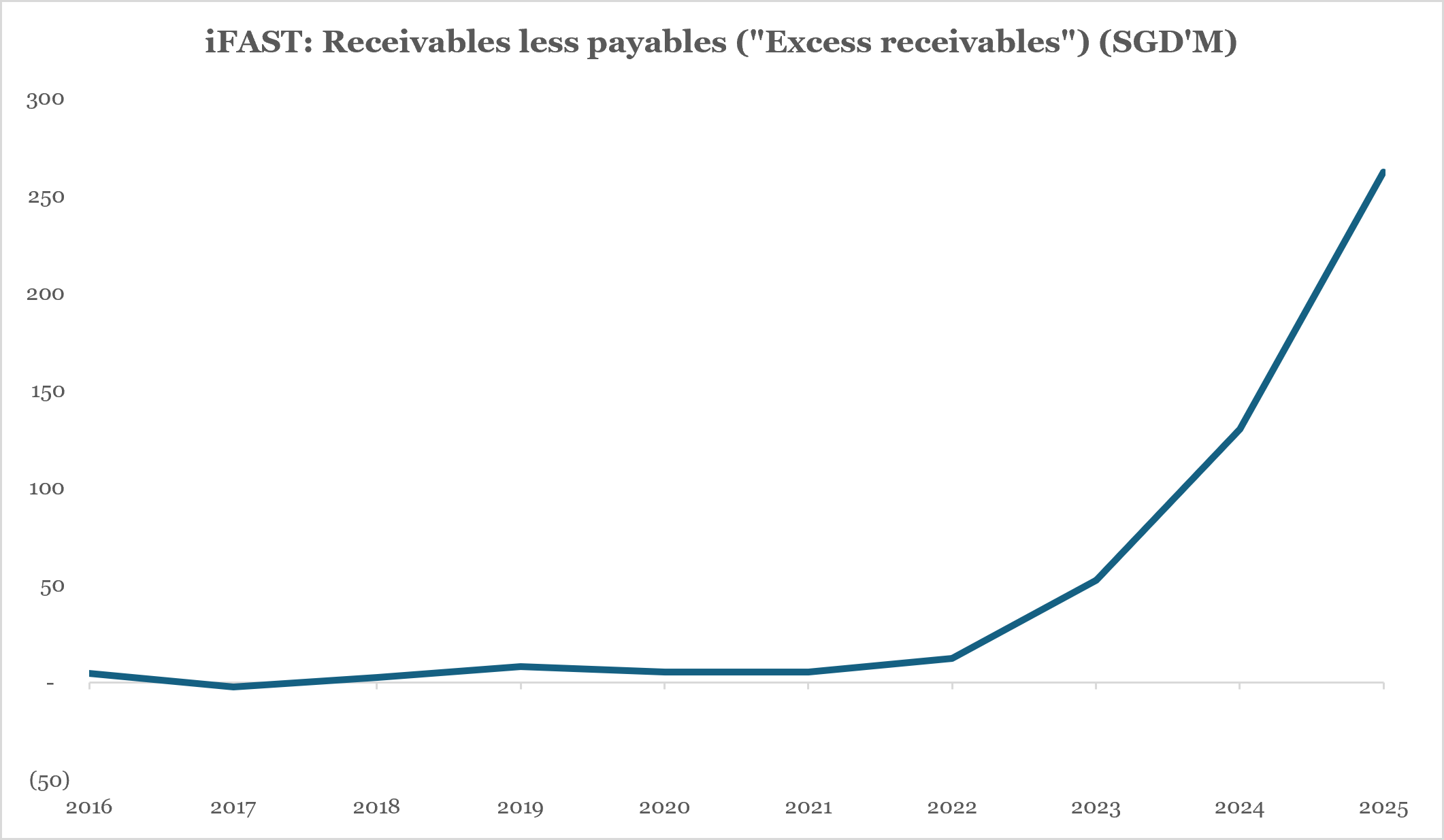

The problem seems to be growing receivables. Over the past 3 years, receivables grew +88% p.a., far outpacing +35% p.a. revenue growth.

Are receivables increasing due to 3rd party financial advisers? Unlikely. When a customer buys investment products on iFAST’s platform through a 3rd party financial adviser, iFAST collects a fee from the customer. A portion of the fee is due to the 3rd party financial adviser.

iFAST records both a receivable (from customer) and a payable (to financial adviser).

Could the receivables growth be due to increasing contribution from transactions like these? If this is true, both receivables and payables should grow in line. There should be no significant growth in excess receivables (receivables less payables).

But this is not what I observed.

Before 2022, excess receivables were stable. They started surging from 2022 onwards, suggesting the recent receivables growth is likely due to other factors.

Source: iFAST annual reports, Angsana Anderson estimates

In 2016, customers took around 91 days to pay iFAST. By 2025, this has increased 330%. Customers are now taking around 301 days to settle invoices.

Likely due to Hong Kong’s eMPF. The surge in excess receivables coincided with the start of revenue recognition from the eMPF Platform project.

In fact, the SGD 262 mn of excess receivables coincides with my estimate of all the revenue that iFAST has recognized from the project (~ SGD 244 mn).

Projects like this are usually based on milestone billing, where iFAST is paid when it completes certain predefined stages.

iFAST reported a credit term of 4 to 6 months for its project fee receivables.2 During the Q4’25 earnings call, management reported trustees onboarding was largely completed in 2026. If so, why did receivables still grow +3% YoY in Q1’26?

Problems with eMPF Platform. In Jun 2025, Bloomberg reported glitches on the eMPF platform, which it described as built by PCCW with operational support from iFAST. The glitches include log-in difficulty and missing information.3

As recently as Mar 2026, the platform is still receiving many complaints. The government has announced that affected members can claim compensation.4

iFAST stated that its role is limited to operational and user delivery services.5

Has iFAST’s UK bank finally turned around?

Finally profitable in 2025. The bull case also involves a turnaround at iFAST Global Bank, its fully licensed banking subsidiary in the UK. iFAST acquired this subsidiary in 2022 when it was suffering from persistent losses. By 2025, the bank finally turned a profit.

Steepening yield curve contributed to profits, but this is beyond the bank’s control. The UK yield curve steepened significantly during the first three quarters of 2025. This benefited banks like iFAST, which borrow at short-term rates and lend at long-term rates.

iFAST’s net interest margin (NIM) improved from 0.8% in the prior year to 1.1% in 2025. Net interest income increased by GBP 5.6 mn, contributing to the lion’s share of the GBP 1.9 mn profit before tax (PBT).6

Given that the yield curve is beyond the bank’s control, I don’t think the profits in 2025 should be seen as durable. In fact, the UK yield curve flattened during Q4’25. iFAST Global Bank reported PBT declined -31% YoY in Q1’26.

Why is margin so high? 2025’s profits were aided by GBP 3.0 mn increase in net fee and commission income. Fee and commission income increased while the corresponding transaction expense decreased. As a result, net fee margin jumped from 72% to 87%.

It is quite rare to see such drastic improvement in margins, and such high margins. For comparison, Remitly Global, Inc. (RELY 0.00%↑ US), another remittance provider, reports only margins around 68%.7

iFAST Global Bank explained that fee and commission income increased due to increased transaction volume at EZRemit, as a result of onboarding new originating counterparties in the Middle East.8

However, I could not find further details on these counterparties, and the end-customers.

Why is iFAST trading at a premium over comparables?

Industry is cyclical. In 2022, AUA declined -8%. The broader stock market decline caused valuation losses and also slowed down net inflows. As a result, operating profit fell -55%.

The bear market in 2018 caused a similar deterioration in performance.

Consensus seems to underestimate cyclicality. iFAST trades at 23x NTM P/E, much higher than its B2B comparable, ALLFG (18x) and its B2C comparable, FUTU (7x).

The consensus seems to justify the premium multiple because of iFAST’s growing earnings visibility and its AUA target of SGD 100 bn by 2030. Sell-side consensus forecasts double-digit growth rates in each of the next three years.

However, I believe such high multiple does not leave enough margin of safety for the industry’s cyclicality.

That said, short-term looks ok. Uncompleted contracts represent contract amounts for client trades that have been executed but not yet settled. It is a leading indicator because of the correlation between trades and AUA.

In Q4’25, uncompleted contracts increased +45% YoY and appears to have continued increasing in Q1’26.

Factors that could lead to a re-assessment of my decision

iFAST starts collecting its receivables (i.e. days receivable normalize below 6 months, the upper limit of the company’s credit terms).

iFAST Global Bank reaches sufficient scale. (e.g. Loan book scales up. Currently, investment grade corporate bonds still form the bulk of its interest-earning assets).

Share price falls >30% without a significant deterioration of business fundamentals.

Coming up next

Previously, I discussed PayPal: Undervalued at 7.8x P/E?

Like PayPal PYPL 0.00%↑ , Block, Inc. XYZ 0.00%↑ has sold off significantly over the past 5 years, dropping almost -70%.

Unlike PayPal, Block is expected to grow its EPS by +45% p.a. over the next two years. PayPal is expected to grow its EPS by only +4% p.a.

Could Block be more attractive?

I will explore this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in AIY, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.