Haw Par: Right for the wrong reasons

[Post-Mortem] Haw Par Corporation Limited (H02; HPAR SP)

Disclaimer: This is a record of my investment decisions and not financial advice. I may change my decisions at any time without notice. Use this only for educational and entertainment purposes. All analysis and opinions are my own and based solely on public information. H02 has not reviewed or endorsed this post. Do not rely on this for your investment decisions. As of the date of publication, I do not hold any positions, long or short, in H02.

About (07 Apr 2026)

Share price: SGD 16.90

Market capitalisation: SGD 3,741 mn (USD 2,918 mn)

Enterprise value (EV): SGD 2,994 mn (USD 2,335 mn)

Average daily volume (ADV): SGD 7.8 mn (USD 6.1 mn)

NTM P/E: 21x; LTM P/B: 0.9x

My Decision

By 25 Mar 2026, I had sold all my shares at an average price of SGD 16.62.

I started buying shares in H02 from Feb 2021. My average cost was around SGD 11.29. I expected to sell my shares for at least SGD 17.00 within 3 to 5 years.

My internal rate of return (IRR) is ~14% p.a. This is slightly higher than the 12% p.a. I expected over 5 years.

Background

Haw Par: Right for the wrong reasons.

I started buying shares in H02 from Feb 2021. It was one of my earliest investments. I explained my thesis here: Haw Par: Crouching tiger, hidden value?

More than 5 years later, H02 still has not made any significant acquisitions. There is no convincing evidence it will do so any time soon. Why is H02 so hesitant?

The hidden assets I saw in H02 remain hidden. I now believe these hidden assets will unlikely ever be unlocked and returned to shareholders. Furthermore, I believe the outlook for Tiger Balm is bleaker than the market expects. Why?

In this Substack post, I answer these questions and walk through why I sold all my shares recently.

Business model

Breakdown of 2025 profit before tax (SGD 283 mn, +14% YoY):

73% Investments (+16% YoY)

24% Healthcare products (+7% YoY)

3% Others (+4% YoY)

The Investments segment mainly engages in long-term investments of companies listed in Singapore. Profit before tax (PBT) is mainly derived from dividends.

H02 owns 4.5% of United Overseas Bank Limited (UOB), one of the largest banks in ASEAN. H02 also owns 8.5% of UOL Group Limited (UOL), a property and hospitality group.

The Healthcare segment manufactures and distributes topical analgesic products under the ‘Tiger Balm’ and ‘Kwan Loong’ brand.

The Others segment includes property and leisure divisions.

Revenue consists mainly of sales of Healthcare products. The Investments segment does not earn any revenue.

H02 earns 13% of its revenue from Singapore, 31% from other ASEAN countries, 27% from other Asian countries and 29% from other regions like Europe and Americas.

Revenue of approximately SGD 125 mn (54% of 2025 group revenue) was contributed from three external customers. These revenues are attributable to the sale of Healthcare products to distributors belonging to the same group of companies.

The largest expense is cost of sales (44% of revenue). This mainly consists of cost of inventories sold.

Investments: Relevant public comparables include Oversea-Chinese Banking Corporation Limited (O39; OCBC SP) and DBS Group Holdings Ltd (D05; DBS SP).

Healthcare: Relevant public comparables include Hisamitsu Pharmaceutical Co., Inc. (4530 JP), Pak Fah Yeow International Limited (239 HK) and Amrutanjan Health Care Limited (590006; ARJN IN).

H02’s shareholder register is dominated by the Wee family (~35%), which founded UOB.

Major institutional shareholders include First Eagle Investment Management (~9%), a US global value investor. Kayne Anderson Rudnick, a US wealth management firm focusing on high-quality businesses, ceased to be a substantial shareholder in Feb 2025.

No prominent activist or private equity investors are on the shareholder register.

My reasons

H02 appears to be fairly valued at the current share price. My thesis on under-recognised growth and hidden assets did not materialise after 5 years.

Under-recognised growth failed to materialise. I initially believed the market was underestimating H02’s potential to grow through mergers and acquisitions (M&A).

Through reading management interviews and analysing its hiring activity on LinkedIn, I believed H02 was about to make a major acquisition. This could increase its net profits by almost 50%.

More than 5 years have passed but H02 has not make any significant acquisitions. There are no signs this will change anytime soon.

Since 2021, H02 has invested a total of ~ SGD 100 mn. H02 does not disclose details of these investments. My analysis of its financial statements suggests that these are mainly in shares listed in Hong Kong.

SGD 100 mn is only ~18% of its cash balance at the start of 2021. If there are no suitable opportunities, H02 should return the excess cash to shareholders.

To their credit, management paid a special dividend in 2025.1 This has reduced the cash pile by SGD 221 mn.

However, H02’s cash pile remains high. Cash and cash equivalents reached SGD 834 mn in 2025. This is 362% of revenue and 24% of market capitalization.

I suspect H02’s reluctance stems from its close call with Hua Han.

In June 2005, H02 spent ~ SGD 35 mn to acquire a 21% stake in Hua Han Bio-Pharmaceutical Holdings Limited (Hua Han).

Hua Han is listed on the Hong Kong Stock Exchange (HKSE). The company produces pharmaceuticals for women and seniors in mainland China.

By 2014, H02 invested a total of ~ SGD 47 mn in Hua Han. After dividends, the total investment was ~ SGD 26 mn.2 This stake was worth SGD 230 mn, an annual return of about +28% since 2005! Impressive.

All that glitters is not gold.

In Dec 2019, the Hong Kong High Court ordered that Hua Han be liquidated.3

What happened?

In Aug and Sep 2016, short sellers like Emerson Analytics and Zhongkui Research alleged Hua Han had inflated its revenue and overstated its assets to conceal the fake profits.45

On 27 Sep 2016, trading in Hua Han’s shares was suspended. Trading has not resumed since.

Just 3 days later, Ernst & Young (EY) suspended their audit because the auditor found irregularities.

By 31 Oct 2016, Hua Han had defaulted on its convertible notes issued just 4 months earlier.

Fortunately, H02 had caught wind of the problems earlier. As early as 2015, Hua Han’s executive directors pursued fundraising without consulting H02 or addressing its concerns.6

By the end of 2015, H02 had sold enough shares in Hua Han to recover its investment of SGD 26 mn. The remaining shares were worth ~ SGD 154 mn. H02 later wrote these down to 0.

After this roller-coaster ride with Hua Han, I believe management is now cautious, maybe too cautious.

Hidden assets remained hidden. I initially believed the market had not fully recognized the hidden assets in H02.

The true economic return on asset (ROA) on its equities investment is 7%. But because of its accounting policy, H02 reports a 3% ROA instead.

I also believed the quality of the Healthcare segment is obscured because it is consolidated with the larger Investments segment.

The quality and value hidden in the Healthcare segment could be unlocked through a spin-off.

In 2024, a shareholder proposed this. Management declined because they believe it will not be beneficial. They cited Tiger Balm’s past experience as a separate listed company before privatization by H02 in 2003.

In any case, the outlook for the Healthcare segment seems bleaker than what the market is expecting.

Revenue declined -6% in 2025. At first glance, this looks mild. But the half-yearly results paint a drastic picture.

Compared to 2024, the first half saw a +7% increase, but revenue in the second half dropped by an incredible -18%.

Management attributed this to weaker consumer sentiment in export-oriented economies and weaker demand in tourism-reliant markets.

Tiger Balm is a popular travel souvenir. During COVID-19 lockdowns in 2020, revenue declined -55%.

However, there were no travel restrictions in 2025 H2. Number of commercial flights even showed a decent growth during this period.7

Since most of H02’s Healthcare products are inexpensive pain relievers, weaker consumer sentiment also seems like a weak explanation.

I suspect the missing explanation is intensifying competition.

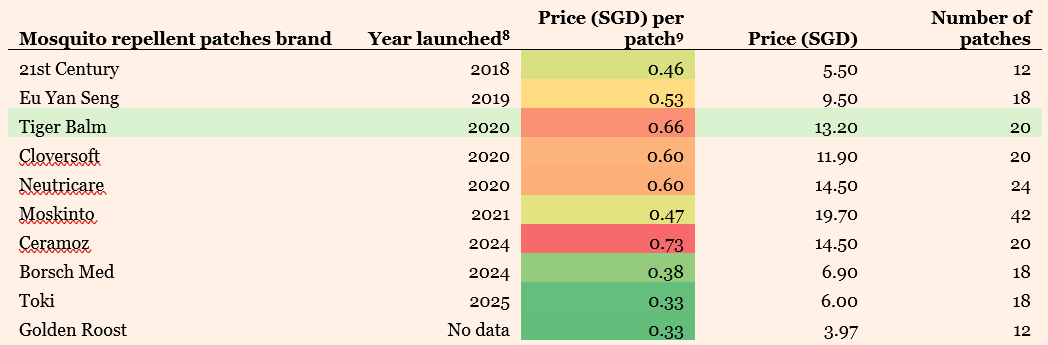

To find out more, I visited a Fairprice supermarket. Fairprice is the largest supermarket chain in Singapore. Yes, for this research, I really visited the supermarket. This is not another of my April Fools’ Day joke.

I collected data on all mosquito repellent patches sold there. I chose mosquito repellent patches because this product range seems to be one of the most popular at H02.

Two important observations.

First, there are many new entrants like Borsch Med.

Second, these new entrants are undercutting the incumbents. Borsch Med offers a unit price that is over 40% cheaper than Tiger Balm.

Of course, this analysis has limitations. I collected data on only one product range at one supermarket on one day. Extrapolating data like this can be very misleading.

I am normally wary of drawing conclusions from such limited data. That said, when taken together with my working capital analysis, the outlook looks bleaker than expected. More on this soon.

In 2024, H02 launched a new product range of essential oils called Tiger Balm Sensorial Therapy.10 It seems like H02’s strategy is to diversify into less competitive product ranges.

However, the demand for the new products looks weak. I observed a significant layer of dust on Tiger Balm Sensorial Therapy in a Guardian store. The adjacent products had little dust. This suggests turnover is very low. True enough, most of the essential oils were manufactured in 2024, some as early as Aug 2024.

A significant layer of dust on Tiger Balm Sensorial Therapy

Source: Angsana Anderson

In a follow-up visit to the same Guardian store, I noticed a newer batch of Tiger Balm Sensorial Therapy on the lower shelves. These were manufactured in 2025.

The store was also offering a 20% discount off the original retail price of SGD 16.90. Heavy discounting is usually done in response to weak demand and overstocking.

With intensifying competition and faltering new products, H02’s outlook looks bleaker than expected. This is reinforced by the trend in its inventory.

In 2025, revenue declined -6% but finished goods increased +11%. This suggests end demand is weak, causing distributors to postpone orders and finished goods to pile up.

Raw materials decreased in line with revenue. Typically, when a company expects strong demand, it increases raw materials to prepare for it.

Work in progress declined -23%, faster than the decline in revenue. This is consistent with a slowdown in production in response to weaker demand.

Valuation

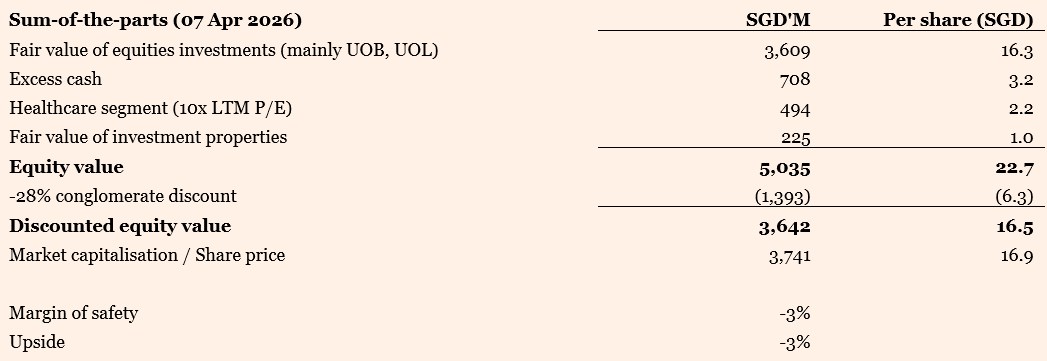

I estimate intrinsic value at SGD 16.50 per share, based on a sum-of-the-parts valuation. At the share price on 7 Apr 2026 (SGD 16.90), H02 shares seem to be fairly valued.

Even though I believe the market has not fully recognized the bleaker outlook for the Healthcare segment, this is not as material as H02’s equities investment and conglomerate discount

A conglomerate discount is required mainly because of capital inefficiency. H02 does not fully pass through its dividend income.

In 2026, I expect H02 will only pass through ~63% of its dividend income to H02 shareholders. The remaining dividends go into its cash hoard that earns only ~2% interest income.

Shareholders would be better off holding shares in UOB and UOL directly.

Over the past 10 years, on average, H02 traded at a -24% discount to its net asset value. Pre-discount equity value is 1.2x net asset value. Therefore, I applied a -28% discount (-24% * 1.2).

Reflections

I started buying shares in H02 from Feb 2021. I believed the market had not fully recognized its inorganic growth potential and its ‘hidden’ assets.

Fast forward 5 years, the inorganic growth failed to materialise. H02 has only deployed ~ SGD 100 mn in equities investments. This is barely 20% of its cash hoard at the start of 2021. There is very little evidence that this will change anytime soon.

The ‘hidden’ assets remain hidden. The Wee family is unlikely to unlock the value in H02’s holdings of UOB because these are crucial for the family to maintain control over UOB. Finally, the outlook for the Healthcare segment became bleaker than expected.

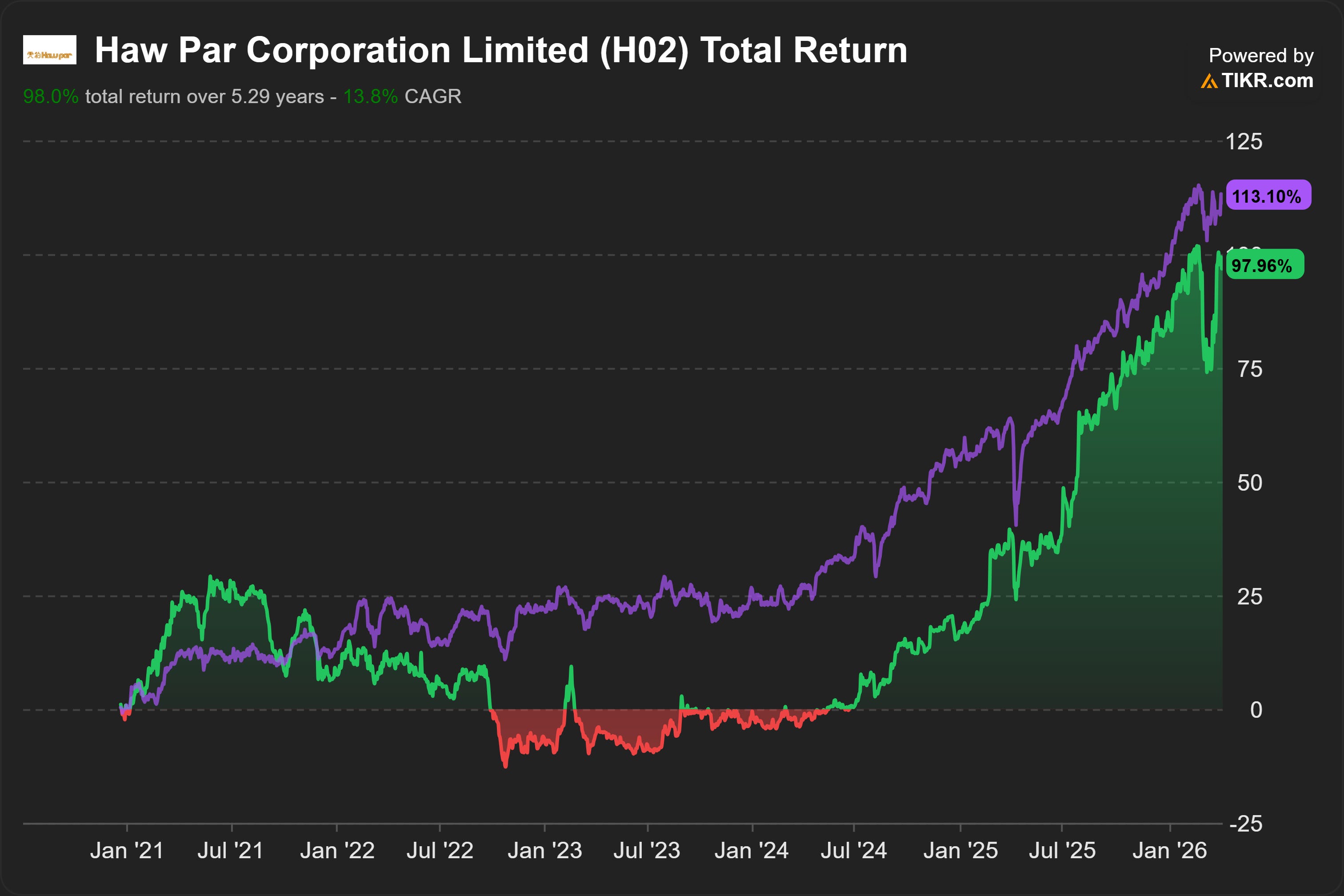

In the graph below, I plotted in green the total return from my investment in H02. The purple line shows ES3, a Straits Times Index ETF. This represents the Singapore stock market.

In Feb 2025, H02 declared a significant special dividend. I somewhat expected this. In my thesis, I said “As the cash pile continues to grow, the probability of more capital returns increases.”

What I did not expect was, in that same month, Singapore launched the Equity Market Development Programme (EQDP), a government programme to boost investment in Singapore-listed shares. H02 rallied together with the Singapore stock market. I got lucky.

The rally broke around the end of Feb 2026 because of the Iran war. However, H02’s share price resumed its rally from mid-Mar 2026 and neared an all-time high by end-Mar. This rally seems to be driven by H02’s addition to the iEdge Next 50, an index that tracks the 50 big Singapore stocks that come after the top 30 blue chips.11

Around the same time, Macquarie, an Australian bank, initiated coverage of H02.12

With these two factors driving strong short-term demand for H02 shares which I believe are valued fairly, I decided this was a good time to sell and move on to investigate other opportunities like SISB Public Company Limited (SISB TB).

If I had invested in ES3, a Straits Times Index ETF, I could have achieved a slightly better result. Nonetheless, I enjoyed learning about business and investing through H02. This was one of my earliest investments.

My experience with H02 also improved my investment philosophy and strategy. It taught me to focus on cash. Investing is laying out cash now for more cash in the future. If my thesis is about hidden assets, then I need to have a reasonable probability of receiving the value from the assets. This is the key lesson.

Factors that can lead to a change in my decision

1. Clear indication that H02 will use excess cash effectively, either through value accretive acquisitions or returning it to shareholders.

2. Strong evidence that H02 will unlock the value in its equities investments. (in my opinion, very unlikely).

3. Discount on net asset rises significantly above average. Current discount is -13% vs -24% 10y average.

4. Strong evidence that the outlook for the Healthcare segment is much brighter than my expectation.

Coming up next

This week, I plan to publish my analysis of Crocs, Inc. (CROX US).

The bull case revolves around CROX as a high-margin, cash‑generative global footwear franchise. The market, however, values like a no‑growth cyclical rather than a durable brand platform.

How true is this? Will I shortlist CROX for my personal portfolio?

Subscribers get to know first. Click on the button below to subscribe for free today.

Subscribe for 2 to 3 analyses of global equities every week. Discover overlooked ideas and rethink familiar names. Published by Andrew Wong, ACA, CFA

References

Various sources, compiled by Perplexity

If there are multiple packaging sizes, I chose the one that gives the lowest price per patch

As promised, I’ve just published my analysis of Crocs, Inc. (CROX US)

Crocs looks very attractive. It trades at only 7x NTM P/E and 10% FCFF yield.

However, I decided to pass.

In my analysis, I discuss the 3 key reasons: (a) High fashion risk; (b) Make China Crocs Again? and (c) Peak margins?

Read it here: https://angsanaanderson.substack.com/p/crocs-ugly-shoes-beautiful-shares?r=5rl2u5