Haw Par: Crouching tiger, hidden value?

[Thesis] Haw Par Corporation Limited (H02; HPAR SP)

Disclaimer: This is a record of my investment decisions and not financial advice. I may change my decisions at any time without notice. Use this only for educational and entertainment purposes. All analysis and opinions are my own and based solely on public information. H02 has not reviewed or endorsed this post. Do not rely on this for your investment decisions. As of the date of publication, I do not hold any positions, long or short, in H02.

About (15 Jan 2023)

Share price: SGD 9.50

Market capitalisation: SGD 2,103 mn (USD 1,600 mn)

Enterprise value (EV): SGD 1,500 mn (USD 1,140 mn)

Average daily volume (ADV): SGD 1 mn (USD 0.8 mn)

NTM P/E: 11x; LTM P/B: 0.7x

My Decision

I first bought H02 shares in Feb 2021. On 15 Jan 2023, I wrote the first version of this thesis. I have reproduced the thesis here, with corrections and edits for brevity and clarity. The core thesis is unchanged.

Starting Feb 2021, I bought shares in H02 at an average cost of SGD 11.29.

Within 3 to 5 years, I expect to sell my shares for at least SGD 17.00.

Over 3 years, I expect to earn ~18% p.a. (15% capital gains; 3% dividend yield). Over 5 years, I expect to earn ~12% p.a. (9% capital gains; 3% dividend yield).

As of 25 Mar 2026, I have sold all my shares at an average price of SGD 16.62.

My internal rate of return (IRR) is ~14% p.a., including dividends.

Background

Haw Par: Crouching tiger, hidden value?

Haw Par is the maker of Tiger Balm, the popular herbal remedy. It smells awful, but it works.

I first invested in Haw Par Corporation Limited (H02; HPAR SP) in Feb 2021. It was one of my earliest investments.

I was attracted to its inorganic growth potential, which I believed the market had not fully recognized.

Through reading management interviews and analysing its hiring activity, I believed Haw Par was about to make a major acquisition. This could increase its profits by almost 50%.

I also believed the market had not fully recognized the ‘hidden’ assets within H02. Its accounting policies have artificially depressed its return on asset (ROA), making it look like a low-return business.

Finally, Haw Par’s investment properties are actually worth 4x more than the value reported on its balance sheet.

In this Substack post, I will walk through these reasons in detail and explain why I bought Haw Par back in Feb 2021.

Business model

Breakdown of 2021 profit before tax (SGD 118 mn, -6.5% YoY):

75% Investments (-13% YoY)

18% Healthcare products (+32% YoY)

7% Others (-3% YoY)

Investments segment mainly engages in long-term investments of companies listed in Singapore. Profit before tax (PBT) in this segment is mainly derived from dividends.

H02 owns 4.5% of United Overseas Bank Limited (UOB), one of the largest banks in ASEAN. H02 also owns 9% of UOL Group Limited (UOL), a property and hospitality group.

Healthcare products segment manufactures and distributes topical analgesic products under the ‘Tiger Balm’ and ‘Kwan Loong’ brand.

Other segments include property and leisure divisions.

Revenue consists mainly of sales of Healthcare products. Investments segment does not earn any revenue.

H02 earns 13% of its revenue from Singapore, 11% from other ASEAN countries, 36% from other Asian countries and 40% from other regions like Europe and Americas.

Revenue of approximately SGD 46 mn (33% of 2021 group revenue) was contributed by two external customers. These revenues are attributable to the sale of Healthcare products to distributors belonging to the same group of companies.

The largest expense is cost of sales (48% of revenue). This mainly consists of cost of inventories sold.

Investments: Relevant public comparables include Oversea-Chinese Banking Corporation Limited (O39; OCBC SP) and DBS Group Holdings Ltd (D05; DBS SP).

Healthcare products: Relevant public comparables include Hisamitsu Pharmaceutical Co., Inc. (4530 JP) and Pak Fah Yeow International Limited (239 HK).

H02’s shareholder register is dominated by the Wee family (~36%), the family that founded UOB.

Major institutional shareholders include First Eagle Investment Management (~10%), a US global value investor and Kayne Anderson Rudnick (~6%), a US wealth management firm focusing on high-quality businesses.

No prominent activist or private equity investors are on the shareholder register.

My reasons

At current valuation, I believe the market is underestimating H02’s growth potential and asset value.

Under-recognised growth. H02 is often seen as a cash hoarder. Cash had reached ~30% of market cap. However, this will likely soon change. There were strong indications that H02 was looking to grow through M&A.

In Jan 2021, LinkedIn shows H02 hired a new group general manager. He was the former head of M&A at SMBC Nikko.

In Feb 2021, CEO Wee said “…with the economic downturn due to COVID-19, there may be more opportunities for acquisitions, and we may succeed.” He added, “We’re keeping our powder dry so that we can strike when we need to - I have some years to go, and I want to build at least another leg for Haw Par for the next generation.”1

In Jul 2022, H02 hired an associate director from EY-Parthenon to work on corporate development. The new hire will look at deals in the consumer healthcare, branded FMCG, and leisure sectors.

Finally, in 2022 H1, H02 spent ~SGD 47 mn buying shares of a listed company. This is the first purchase in many years.

Hidden assets. H02 is often seen as a poor-quality business because of its low return on asset (ROA) and return on equity (ROE). However, H02 is actually a high-quality business. Its accounting is obscuring this.

H02 accounts for its stake in UOB, UOL, etc at fair value through other comprehensive income (FVOCI). This means H02 recognises their market value (SGD 2.8bn) on its balance sheet.

However, the accounting standards only allow H02 to recognize its dividend income (SGD 85 mn) rather than its share of UOB, UOL and other holdings’ profits (SGD 211 mn). As a result, H02 reports ROA of 3% on its investments rather than the true economic ROA of 7%.

In 2021, H02 owns investment properties valued at SGD 215 mn. However, this value is ‘hidden’ because of H02’s accounting policy.

H02 accounts for its investment properties at cost less accumulated depreciation and impairment instead of fair value. This means these investment properties are reported on H02’s balance sheet at SGD 53 mn, rather than their fair value of SGD 215 mn.

Finally, headline ROA obscures the quality of H02’s healthcare segment. Because the healthcare segment is consolidated with the investment business, H02 reported group ROA (PBT / total assets) of 4% in 2021. In fact, H02’s healthcare segment earned an above-average ROA of 12% in 2021.

H02’s competitive advantage lies in its brand name. Tiger Balm is a very established and trusted brand that customers see as safe and reliable. Because of this trust, it can charge higher prices than rivals and customers still stick with it.

Valuation

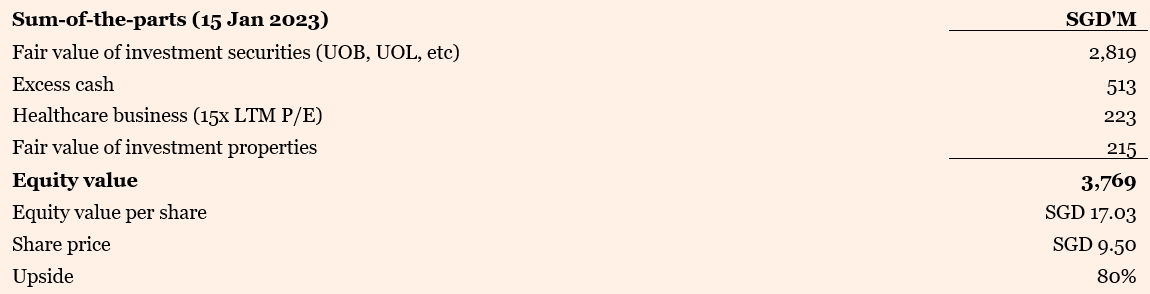

I estimate intrinsic value at SGD 17.00 per share based on a sum-of-the-parts valuation.

At the share price on 15 Jan 2023 (SGD 9.50), I have ~44% margin of safety and ~80% upside.

Catalysts

Growth from M&A. Let’s say H02 uses its SGD 513 million excess cash to make a sensible acquisition and achieves a 10% p.a. return on the acquisition. H02’s net profit after tax (NPAT) will increase by SGD 51 million. This is equivalent to a 46% increase from 2021 group NPAT.

Capital return. H02 periodically reduces its cash pile via special dividends. In 2019, H02 paid out ~36% of its cash as special dividends. As the cash pile continues to grow, the probability of more capital returns increases.

Risks

Poor acquisitions. In 2005, H02 acquired 21% of Hua Han Bio-Pharmaceutical Holdings Limited, a pharmaceutical company listed in Hong Kong.

Hua Han reported strong business performance initially. In 2016, Emerson Analytics, a short seller, alleged Hua Han inflated its revenue, among many other misdeeds.2

Fortunately, H02 had caught wind of the problems earlier. By 2015, H02 had already recovered its initial investment.

This risk is now mitigated by H02’s hiring of professional corporate finance talent. H02’s general manager is the former head of M&A at SMBC Nikko. He is supported by a former associate director from EY-Parthenon.

No acquisitions, continue hoarding cash. There is a risk that H02 continues hoarding cash instead of making accretive M&A.

If this happens, a 20% holding company discount will be required. This will reduce my estimated equity value to SGD 13.60, reducing my margin of safety from 44% to 30% and my upside from 80% to 43%.

Even in the worst-case scenario, a 44% holding company discount will be required to eliminate our upside. This is highly unlikely because (a) for the reasons we discussed earlier, growth will be likely higher than expected and (b) H02 periodically reduces its cash pile through special dividends.

Coming up next

Next week, I’ll follow up with a full post-mortem on my investment: what went right, what went wrong, and why I ultimately sold all my shares recently.

I like to describe my investment as ‘right for the wrong reason’.

Subscribe now to receive the post-mortem in your inbox next week.

Subscribe for 2 to 3 analyses of global equities every week. Discover overlooked ideas and rethink familiar names. Published by Andrew Wong, ACA, CFA

Refer 3 friends, get a deep-dive on 1 company!

I’m trialing Substack’s referral program until Thu 30 Apr 2026.

If you know anyone who would enjoy 2 to 3 analyses of global equities every week, refer them.

For every 3 friends who subscribe, you can send me the name of one listed company you’re interested in.

I’ll publish a post that walks through my fundamental analysis of the business and explain whether I would pass or buy it for my own portfolio. But I do not make investment recommendations.

Get your unique referral link here: https://angsanaanderson.substack.com/leaderboard

As promised, I’ve published my post-mortem on Haw Par Corporation Limited (H02; HPAR SP).

I sold all my shares because more than 5 years on, H02 still has not made any significant acquisitions. There is no convincing evidence it will do so any time soon.

The hidden assets I saw in H02 remain hidden. I now believe these hidden assets will unlikely ever be unlocked and returned to shareholders.

Furthermore, I believe the outlook for Tiger Balm is bleaker than the market expects.

Find out more here: https://angsanaanderson.substack.com/p/haw-par-right-for-the-wrong-reasons?r=5rl2u5