Grab: Not as cash-generative as you think

[First Take] Grab Holdings Limited (GRAB US)

Summary

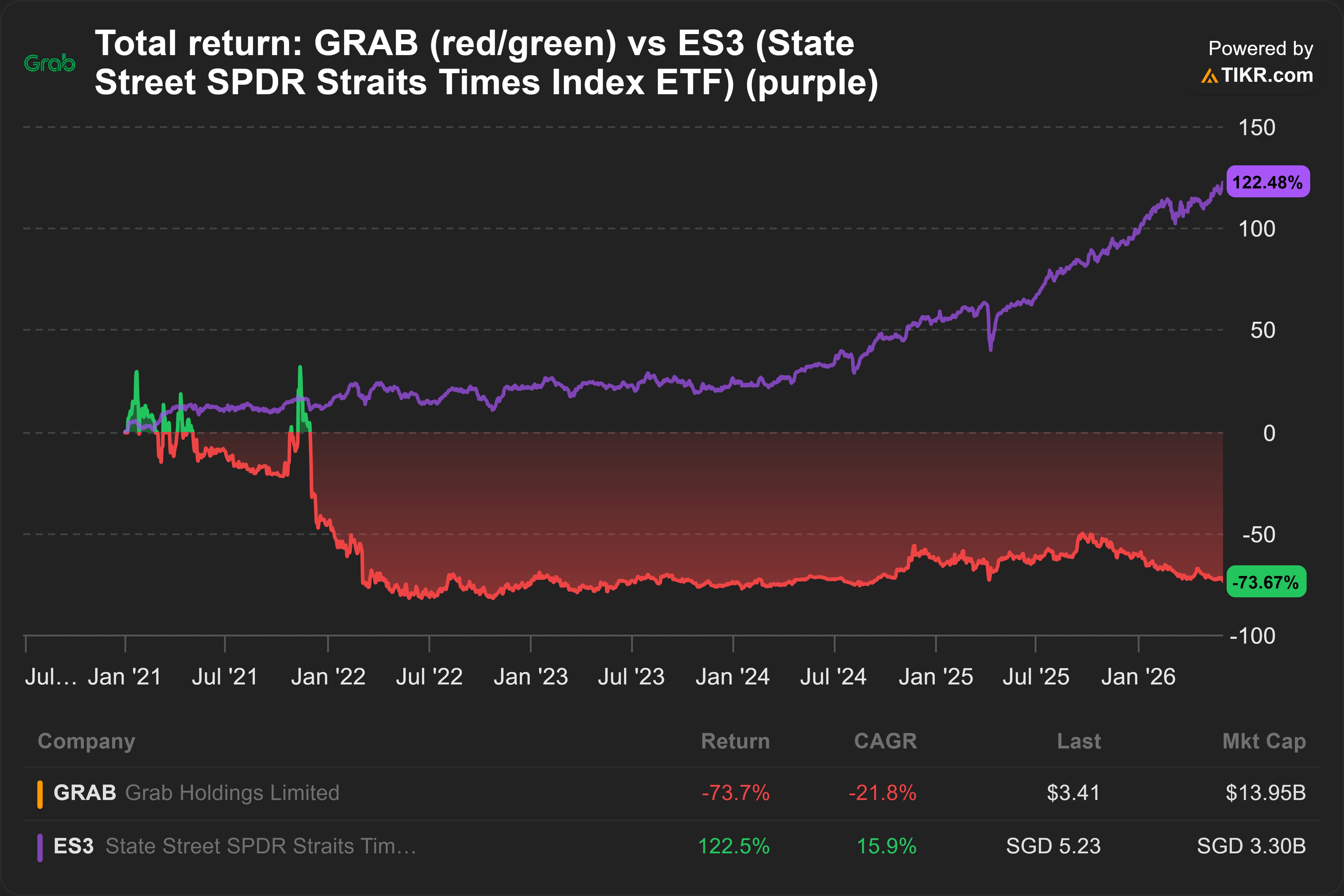

I decided to pass on GRAB US.

GRAB’s adjusted free cash flow overstates its true cash-generating ability because it includes stock-based compensation (SBC). SBC is actually financing from employees.

Despite being the dominant platform across South-east Asia, GRAB’s pricing power is limited.

Several factors contribute to this: more price-sensitive consumers, stronger competition. The factor least appreciated: regulatory pressure.

Although GRAB’s shares are not obviously attractive to me now, I believe the business will likely still do well.

CEO Anthony Tan and his team have demonstrated strong ability to raise funds.

About (4 Jun 2026)

Share price: USD 3.41

Market capitalisation: USD 13,947 mn

Enterprise value (EV): USD 9,437 mn

Average daily volume (ADV): USD 171 mn

NTM P/E: 33x

Time spent: ~1 day

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Pass

Background

“Buy GRAB US! A cash-generative monopoly with high growth in fintech”

That is the consensus bull case.

However, Grab is not as cash-generative as many investors think.

Its pricing power still looks weak, despite being the dominant platform in South-east Asia.

Its expansion into fintech reinforces the challenges in its core segments.

Although its shares are not obviously attractive to me, I believe Grab, as a business, will still do well. The secret weapon? Anthony Tan.

Business model

Breakdown of 2025 revenue (USD 3.4 bn; +20% YoY):

53% Deliveries (+21% YoY)

36% Mobility (+16% YoY)

11% Financial services (+37% YoY)

GRAB operates an app providing deliveries, mobility, and financial services across South-east Asia. As of Q1’26, the company serves 52 mn monthly transacting users.

The Deliveries segment connects drivers and merchants with consumers looking for deliveries of meals, groceries and parcels.

The Mobility segment connects drivers with consumers looking for transport. Consumers can hire private cars, taxis and motorcycles through the Grab app.

The Financial Services segment provides banking services such as digital payments, deposits, loans and receivables factoring.

This segment is carried out by GXS Bank Pte. Ltd (GXS), a joint venture with Singapore Telecommunications Limited (Z74; ST SP). Because GRAB retains control, GXS is consolidated into GRAB’s financial statements.

Customers are typically urban residents across South-east Asia who rely on the Grab app for everyday conveniences like ride-hailing, food delivery, and digital financial services.

No significant portion of GRAB’s revenue can be attributed to a particular customer or group of customers.

GRAB earns 31% of its revenue from Malaysia, 22% from Singapore and 21% from Indonesia. The remaining 26% is derived from the Philippines, Thailand, Vietnam and other countries in South-east Asia.

In 2025, Malaysia and Singapore were the fastest growing markets, with +27% and +26% YoY growth respectively. Indonesia and Vietnam grew the slowest, at +11% and +12% YoY growth in 2025.

The closest public comparable is PT GoTo Gojek Tokopedia Tbk (GOTO IJ).

GOTO is GRAB’s most direct regional competitor in South-east Asia. It competes fiercely with GRAB in the key Indonesian market for mobility, food delivery, and digital payments.

Other comparables include Uber Technologies, Inc. (UBER US) and DiDi Global Inc. (DIDIY US).

UBER is the most direct global comparable due to its dual dominance in both ride-hailing (Uber) and food delivery (Uber Eats). GRAB actually acquired UBER’s South-east Asian operations in 2018.1

DIDIY is the dominant ride-hailing platform in mainland China.

My reasons

Not as cash-generative as you think

Adjusted free cash flow includes SBC. GRAB uses adjusted free cash flow to monitor business performance and assess cash flow activity.

GRAB defines adjusted free cash flow as net cash flows from operating activities less capex plus proceeds from disposal of property, plant and equipment. It excludes changes in working capital related to its banking business.

In my opinion, this definition overstates the true cash flow generated by the business because it includes stock-based compensation (SBC).

SBC is financing from employees. To simplify, GRAB recognizes SBC when it pays salaries with newly issued shares instead of cash. It is the equivalent of raising cash from employees.

This may sound too technical, but it’s actually easy to understand. Let’s use an example.

Company A pays employees with SBC. Company B issues shares and uses the cash to pay salaries.

The economic outcome is the same.

But if we follow GRAB’s definition, then Company A will report higher free cash flow.

Same economic outcome, different numbers reported.

That’s why, to show the business’ true cash-generation ability, SBC should be deducted from operating cash flow.

True free cash flow is much lower. In 2025, GRAB reported USD 290 mn of adjusted free cash flow.

If GRAB had paid its employees with 100% cash, it would have reported USD 49 mn of free cash flow. This is -83% lower than the adjusted free cash flow reported by GRAB.

Source: Angsana Anderson’s estimates based on GRAB’s 10-K

Pricing power is weaker than expected

Dominant player. Grab is dominant in almost all the countries it operates in. In food deliveries, GRAB is estimated to have ~55% gross merchandise value (GMV) market share in South-east Asia.2

But pricing power is weak. Despite its dominance, GRAB seems to struggle with raising its commission. Revenue as % of GMV represents GRAB’s commission or take-rate.

Post COVID-19 boom, GRAB’s take-rate has largely plateaued:

Source: Angsana Anderson’s estimates based on GRAB’s 10-K

UBER, GRAB’s global peer, demonstrates stronger pricing power.

It increased its Mobility take-rate from ~20% in 2021 to ~30% by 2025. During the same period, UBER raised its Deliveries take-rate from 18% to 19%.34

Why does UBER enjoy higher take-rate? Why can it raise its take-rate faster than GRAB?

I believe there are multiple factors.

Consumers in South-east Asia generally have lower income and are more price-sensitive. Competition is more intense. In Singapore alone, GRAB faces off against Gojek, TADA, Ryde, etc.

However, I believe the most underappreciated factor is regulatory pressure.

Regulatory pressure. In 2024, Singapore introduced the Platform Workers Act. The law became effective from 1 Jan 2025 and mandated better benefits for platform workers like Grab drivers.

GRAB mitigated the increased costs by raising its platform fees.5

On 1 May 2026, President Subianto announced Indonesia will reduce the maximum commission of ride-hailing companies from 20% to only 8%.6

GRAB later clarified this new rule will only impact 2-wheelers, which is less than 6% of their GMV.

However, this goes to show that, despite being the dominant platform, GRAB faces significant regulatory pressure. Its pricing power is constrained.

Its drivers are numerous, and are generally among the most economically vulnerable. Between “filthy rich” shareholders and “honest hardworking” drivers (and voters), which group will governments choose?

I suspect the challenge in raising take-rate is a main driver behind GRAB’s hard push to transform itself into a super-app.

GRAB acquired Jaya Grocer, a Malaysian supermarket chain, in 2022. During the same year, GRAB entered into banking services through GXS.

Other matters

Although the shares do not fit into my investment strategy, I believe Grab, as a business, will likely do well.

Anthony Tan and his team are very good at selling their vision to investors.

From nabbing Softbank as an investor to going public in Dec 2021, right before the 2022 bear market, they have demonstrated strong fund-raising abilities.

In Jun 2025, GRAB issued convertible notes. The offer size was USD 1.5 bn, which will support the business’ cash requirements for some time.

The terms were favourable. The notes carried zero interest, and the high conversion premium (40%) minimises dilution.

Factors that could lead to a re-assessment of my decision

GRAB continues to scale and generate significantly more cash than I expect

GRAB can increase take-rate significantly above current levels

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in GRAB, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.

Great write up. One point to add is GRAB’s TTM adjusted FCF is $489 million and SBC was $238 million. That comes out to FCF of $251 million on a TTM basis.

SBC is not an expenses.

After the vesting period, the dilution stays and SBC gone from the statement.

The EPS as well as OCF are self corrected every time the vesting period of a SBC is executed and over.