GQG: Good business, temporary headwinds?

[Shortlist] GQG Partners Inc. (GQG AU)

Summary

I shortlisted GQG.

Consensus believes funds under management (FUM) will decline.

However, GQG seems to be a good business facing temporary headwinds.

Since Q3’25, investors have been redeeming their funds because GQG is underperforming its benchmarks. GQG’s relative underperformance is driven by its underweighting of AI and semiconductor stocks.

I believe there is a low risk of a sudden and large collapse in FUM.

Net outflows are decelerating. This suggests short-term investors have largely redeemed.

With the S&P 500 concentrated in AI and semiconductor stocks carrying stretched valuations, there is demand for non-AI and non-US funds, like those offered by GQG.

Finally, GQG offers an attractive 15% dividend yield. This seems sustainable. The business does not require significant investment in working capital or capital expenditures.

Key factors to look into: (a) probability and timing of inflection in net flows; (b) customer concentration; (c) key man risks.

About (05 Jun 2026)

Share price: AUD 1.39

Market capitalisation: AUD 4,112 mn (USD 2,897 mn)

Enterprise value (EV): AUD 3,949 mn (USD 2,783 mn)

Average daily volume (ADV): AUD 6.0 mn (USD 4.2 mn)

NTM P/E: 7x

Time spent: ~1 day

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Shortlist

Background

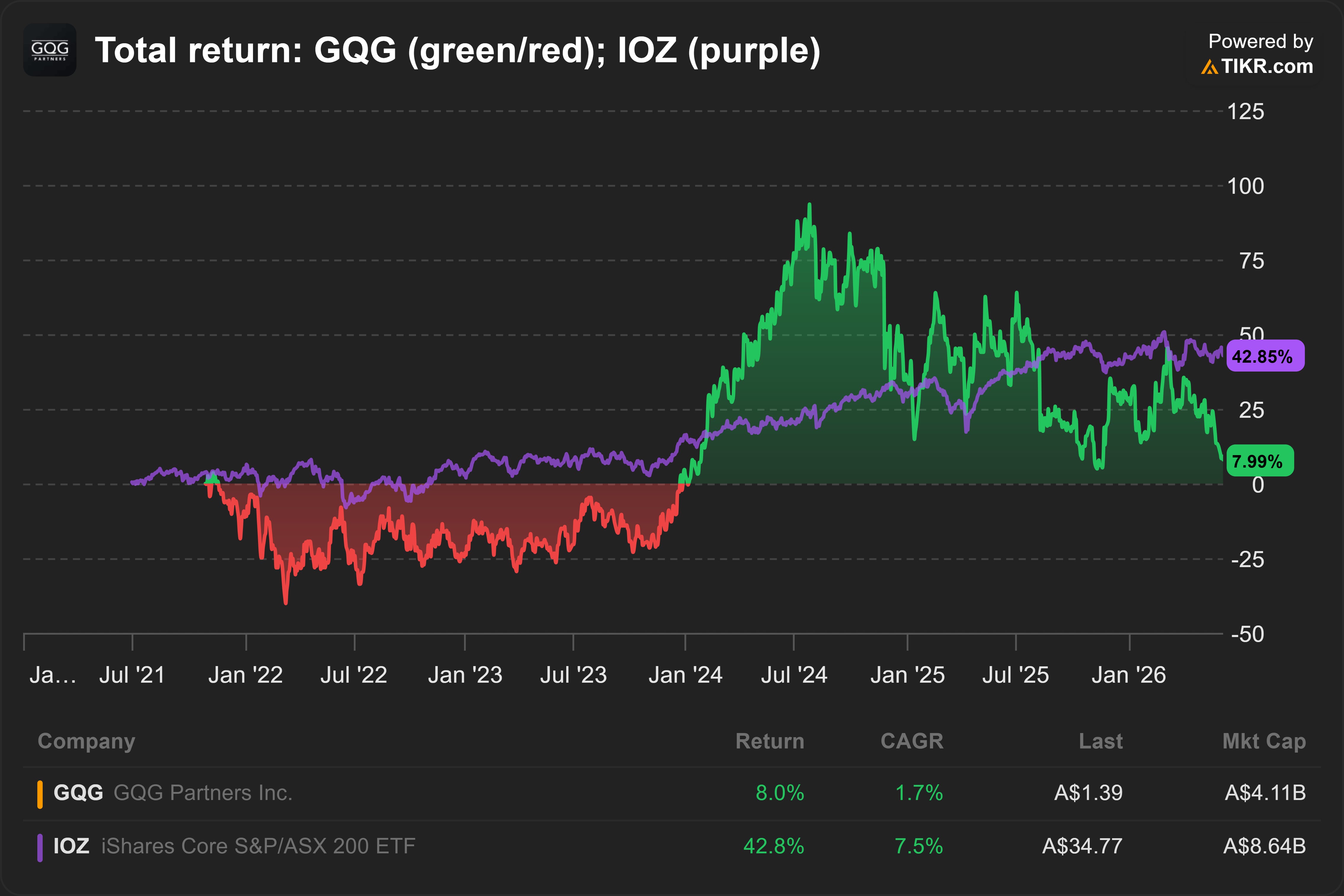

Is there an opportunity in 15% dividend yield?

An investment manager is now back at its IPO price.

The company is wrestling with fund outflows.

Its relative performance has been deteriorating because of its decision to avoid AI stocks.

However, these headwinds seem to be temporary.

Business model

GQG is an investment boutique investing in listed equities globally.

In 2025, 98% of its revenue comes from management fees (+8% YoY). Performance fees (-44% YoY) are immaterial, making up only 2% of total revenue.

GQG earns 81% of its revenue from the United States. No individual foreign country contributed more than 10% of total revenue.

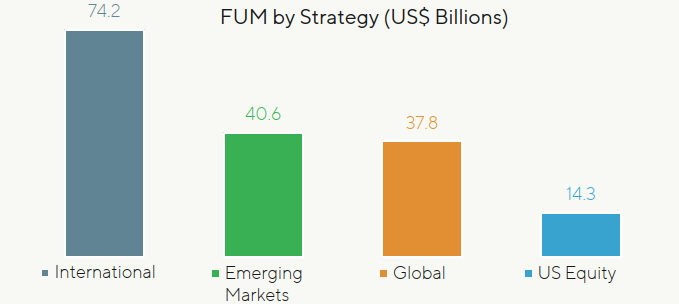

GQG manages four strategies: Global Equity, International (non-US) Equity, Emerging Markets Equity, and US Equity.

As of 30 Apr 2026, the International Equity strategy accounts for 44% of funds under management (FUM). The Emerging Markets strategy accounts for 24%.

Source: GQG (2026)

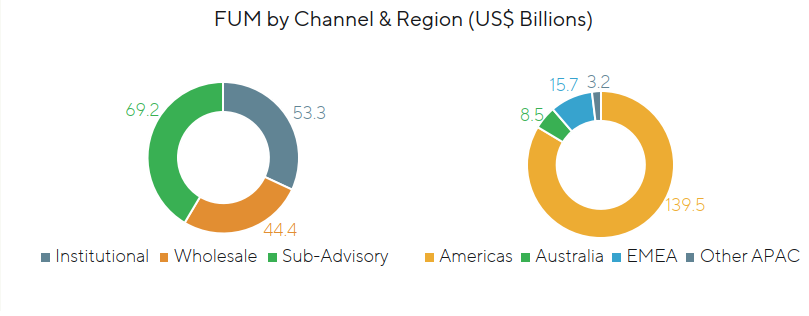

41% of FUM is managed through the sub-advisory channel. A sub-advised fund is an investment fund that is formed and managed by a third-party firm that retains GQG to manage part or all of the fund.

32% of FUM is managed through the institutional channel. These funds come from investors with large pools of investable assets such as insurance funds, pension/superannuation funds, sovereign wealth funds and ultra-high net worth investors.

The remaining 27% is managed through the wholesale channel. This channel is typically financial intermediaries such as financial advisers, wealth management administration platforms or private banks.

Source: GQG (2026)

The investment management industry is fragmented but increasingly consolidating.

Public comparables of similar size include Magellan Financial Group Limited (MFG AU), Perpetual Limited (PPT AU) and Jupiter Fund Management Plc (JUP LN).

My reasons

Good business, temporary headwinds?

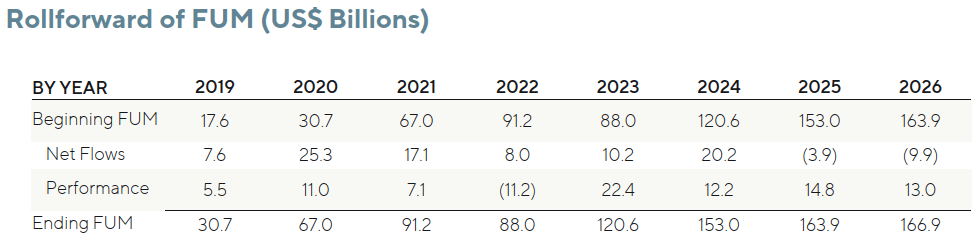

Consensus expects decline. According to Tikr, consensus sell-side forecasts -3% and -4% revenue decline in 2026 and 2027.

Net outflows. Consensus expects revenue to decline because investors have been redeeming their capital, resulting in net outflows since Q3’25:

As of 30 Apr 2026. Source: GQG (2026)

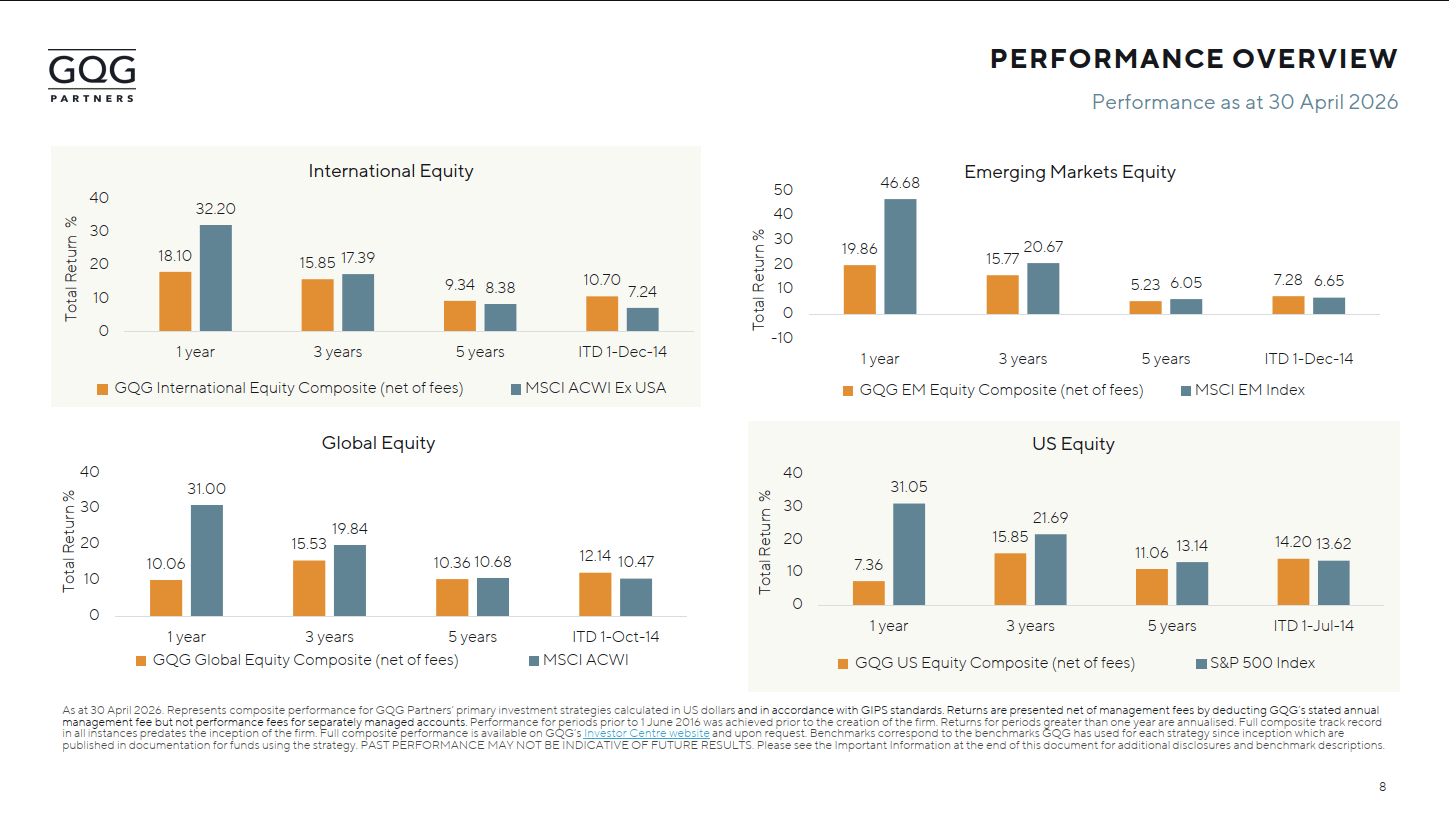

The net outflows are largely the result of relative underperformance.

GQG has outperformed its benchmark across all 4 strategies since inception. However, its performance has been lagging benchmarks in recent years:

Source: GQG (2026)

Defensive positioning. GQG’s relative underperformance has been mainly driven by GQG’s decision to avoid AI-related stocks.

Goldman Sachs GQG Partners International Opportunities Fund is a sub-advisory fund managed by GQG. It accounts for ~33% of GQG’s FUM.

The top 10 holdings consist of companies in consumer staples and energy like Philip Morris International Inc. (PM US) and TotalEnergies SE (TTE FP).1 There are no AI-related companies.

Net outflows are decelerating. The net outflows since Q3’25 likely consist of clients who cannot tolerate short-term underperformance stemming from a defensive positioning.

There are signs that such clients have largely exited.

Monthly net outflows are starting to decelerate:

Low risk of FUM collapse. With the S&P 500 becoming more concentrated in AI-related companies, and valuation reaching historical highs, there will be higher demand for non-US and non-AI funds to diversify risks.

GQG’s products offer that diversification, especially with its largest strategy, International Equity, which focuses on non-US stocks. This is likely what the existing clients are staying for.

I also believe the risk is low of sudden redemptions large enough to disrupt the business. GQG’s FUM is well diversified across institutional, sub-advisory and wholesale channels.

According to my discussion with an equity product specialist, institutional clients can take months before making final decisions on redemptions. The process is long.

They will usually engage consultants, who then conduct extensive performance attribution and studies before they come up with recommendations, etc.

GQG’s relatively low fees are another incentive for clients to stay. On average, GQG charges management fee that is ~0.5% of FUM. The industry average is around 0.7% to 1.0%.

Good business. The focus on the recent net outflows overshadows the quality of the business and management.

CIO Rajiv Jain and CEO Tim Carver founded GQG in 2016. In less than 10 years, they grew the startup into a USD 167 bn FUM business with ~200 professionals.

They built a good long-term track record. Since inception, all strategies have beaten their benchmarks, despite the recent underperformance.

CIO Jain and CEO Carver achieved these despite the challenges confronting active equity managers.

Peers like Aberdeen Group Plc (ABDN LN), MFG and JUP have been experiencing stagnant or even declining FUM, driven by market share losses to low-cost passive equity ETF offered by the likes of BlackRock, Inc. (BLK US).

Capital returns?

15% dividend yield seems sustainable. GQG targets a payout ratio between 50% to 95% of distributable earnings. In the past few quarters, the payout ratio averages ~90%. This means an attractive dividend yield of ~15%.

It seems like GQG can maintain the current level of dividend. The business does not require significant investment in working capital or capital expenditure. As discussed earlier, I believe the risk is low of a sudden and large collapse in FUM.

Catalysts

Inflection in net flows. Net flows is probably the single most important metric for investment managers.

In Apr 2025, JUP’s share price started recovering after it reported significant institutional net inflows in Q1’25, after multiple quarters of net outflows.

Factors to focus on

Probability and timing of inflection in net flows. When the AI and semiconductor rally fizzle, GQG’s relative performance will likely improve, given its defensive positioning. GQG should return to net inflows at that time.

As discussed in Where are we in the semiconductor cycle?, we are likely in the later stages of a semiconductor shortage.

The shortage could end around Q1’27. Because of forward guidance, investors will start reacting one or maybe two quarters before Q1’27. This means the market rally may end around Q4’26.

This is what I expect.

Could there be anything that can break my expectations? Are there any precedents?

Customer concentration. In its 2025 financial statement, GQG disclosed “One of our Mutual Fund clients accounted for 24.6% and 24.9% of the total revenue for the years ended December 31, 2025 and 2024, respectively.”

GQG added, “One of our SMA clients accounted for 22.7% and 20.6% of total revenue for the years ended December 31, 2025 and 2024, respectively.”

I suspect the Mutual Fund client refers to GQG’s sub-advisory relationship with Goldman Sachs, most notably the Goldman Sachs GQG Partners International Opportunities Fund. I believe the concentration risk is low because the end clients are likely numerous.

Who is the separately managed account (SMA) client? Is the concentration risk acceptable? If GQG loses this client, is current valuation still attractive?

Key man risk. Talent is the biggest asset in the investment management business.

The sudden departure of its CEO and CFO contributed to the downfall of a peer, MFG AU.2

In Feb 2025, JUP said outflows in 2024 were driven by more than GBP 6 bn pulled from strategies managed by Ben Whitmore, one of its star portfolio managers.3

For GQG, the key talents are its founders, CIO Jain and CEO Carver. CIO Jain has primary and veto authority over all portfolio management decisions and is chiefly responsible for portfolio parameters.

I do not worry about them leaving GQG. They own ~70% and 4% of GQG, respectively. However, if anything untoward happens to them, it could cause significant disruption to the business.

If the founders were to retire, how would GQG perform? Does the business have potential successors that can take over the CIO and CEO’s duties?

Coming up next

A month ago, I shortlisted MegaStudyEdu Co. Ltd (215200 KS).

Investors seem to be pricing in an indefinite revenue decline and underestimating its growth.

The company is returning ~12% of its market capitalisation to shareholders via dividends and buybacks.

Since then, its share price has fallen almost -17%.

This is despite Q1’26 earnings showing the business maintained revenue, while increasing net profit after tax by 8% YoY during the quarter.

Is there an opportunity?

I will explore this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in GQG, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.

Interesting pitch. The valuation seems interesting but two concerns:

1. This sounds dogmatic but Chris Hohn said on an interview that he has a shortlist of industries he avoids (mostly cyclical) which include asset managers. This seems like a cyclical business where underperformance begets more underperformance as funds are withdrawn AND there are headwinds from passive indexing that could destroy demand for the company's services. It's not a cyclical business like homebuilding where demand will continue existing and will recover when interest rates fall.

2. A high dividend yield is a sign that the business doesn't see opportunities to re-invest.