Fu Shou Yuan: China’s largest cemetery operator suspended, and faces delisting

The 3 big red flags hiding in plain sight: Surging goodwill, Unnecessary borrowing, High Board turnover

“[We will] stay focused on managing Fu Shou Yuan, a living entity that carries memories and emotions, with a view to consistently rewarding our Shareholders with the best returns.”

That was the last interim report Fu Shou Yuan published on 23 Sep 2025.1

6 months later, the Hong Kong Stock Exchange (HKEX) suspended the company.2

Why did HKEX suspend Fu Shou Yuan?

Investigators found 47 questionable transactions amounting to around RMB 20 mn from 2016 to 2025.

Employees said some of these transactions were made under the former CEO’s instructions without any supporting documents.

The former CEO also withdrew cash without proper approval.3

Am I screwed? I bought a lot of shares back in 2022

I can’t tell for sure. The investigation is still ongoing.

I poured 20% of my portfolio into the company

That’s crazy! Why did you do that?

In Dec 2022, the Chinese government suddenly relaxed COVID-19 lockdowns. Everyone was expecting deaths to increase.4

I thought Fu Shou Yuan should benefit. It is China’s largest cemetery operator. Most of their revenue comes from selling and maintaining burial plots.

Despite the rally in its share price, I thought the shares were still too cheap for such a high-quality compounder with a long runway.

The share price was still below its previous peak. It’s too cheap.

Ok, but that doesn’t mean you should put 20% in, right?

Buffett said, “Big opportunities come infrequently. When it’s raining gold, reach for a bucket, not a thimble.”

Ok.

Actually, I was interested in the shares some time ago.

But I quickly passed.

I ran my eyes over their 10-year financials, and I had too many questions.

What did you see?

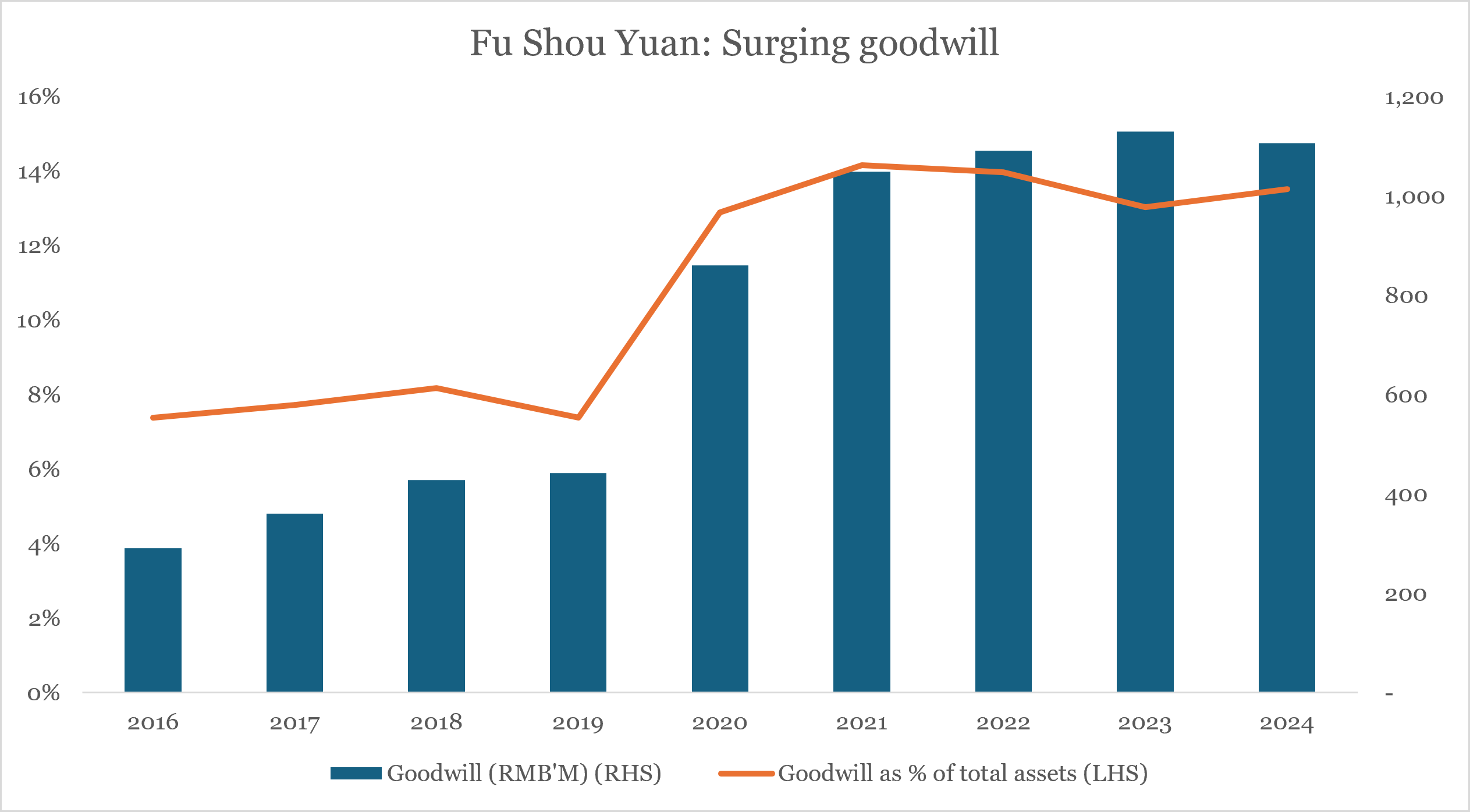

First, surging goodwill.

Goodwill nearly tripled between 2016 and 2020. In just five years, it went from 7% of total assets to 13%.

Source: Fu Shou Yuan, Angsana Anderson estimates

What is goodwill?

In an acquisition, the acquirer must record the acquired assets and liabilities at fair value.

The acquirer then compares the fair value against the acquisition price. If the acquisition price exceeds the fair value, the acquirer records the excess as goodwill.

Essentially, goodwill is the accountant’s way of saying, “The fair value of the target company is only $100 mn, but the acquirer is willing to pay $150 mn.

The acquirer must have seen some benefits in paying that extra $50 mn.

Let’s call this ‘hidden asset’: goodwill.”

Goodwill is common in the software industry.

Much of the value in a software company is not in their physical assets. Rather, their value comes from intangibles like the value of their software engineers, talented management, etc.

These get captured in goodwill.

Ok. Why are you concerned over surging goodwill at Fu Shou Yuan?

Cemetery operators are essentially in the real estate business. The only difference is they sell to the dead.

Goodwill is rare in real estate. Fair value is easily determinable and there are not a lot of intangibles like human capital, etc. that can result in goodwill.

Let’s illustrate with an acquisition Fu Shou Yuan made in 2017.

Fu Shou Yuan acquired Guangxi Huazuyuan, another cemetery operator. The company recorded RMB 23 mn of goodwill against the RMB 46 mn acquisition price.5

Why is Fu Shou Yuan recognising so much goodwill for a business where cemetery assets (real estate) are the main asset (51% of total assets acquired)?

What else did you see?

Unnecessary borrowing.

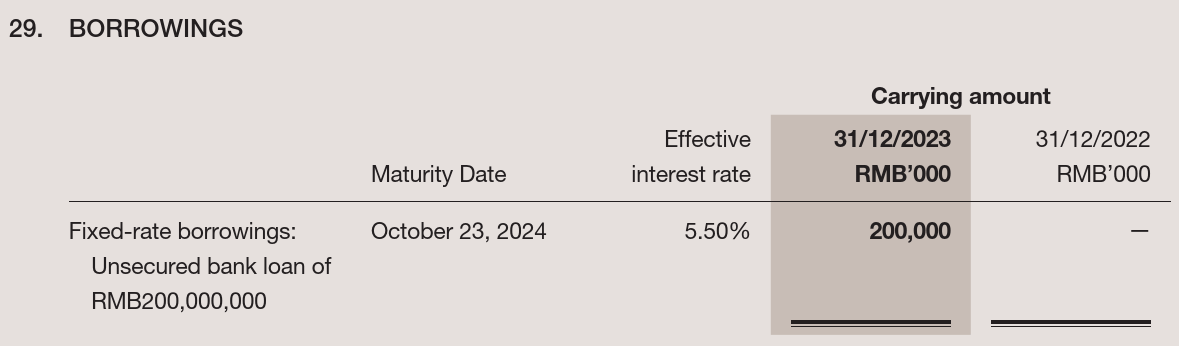

In 2023, Fu Shou Yuan borrowed RMB 200 mn. This was unexpected because the company had so much cash.

In fact, over the past 10 years, the company’s cash to revenue ratio never dropped below 100%. The median for real estate companies is only ~38%.6

Source: Fu Shou Yuan, Angsana Anderson estimates

I don’t think this is a red flag.

In their 2024 annual report, Fu Shou Yuan clarified the loan was “an overseas bank loan designated for the purpose of dividend payout.” They fully repaid the loan in 2024.7

Yes, companies operating in the mainland but listed in Hong Kong sometimes borrow to fund their dividends.

Moving large sums of cash across the border from mainland subsidiaries to the offshore listing entity requires passing through China’s strict foreign exchange controls (SAFE regulations). Cross-border dividends also often trigger a 10% withholding tax.

To bypass the delays, bureaucratic friction, and immediate tax leakage of moving cash outward, a company’s offshore entity will simply take out an offshore bank loan or issue HKD-denominated bonds to fund the immediate dividend payout.

But!

If Fu Shou Yuan borrowed to fund its dividends, why did they borrow in RMB instead of HKD?

Their bank charged 5.50%. Why is the interest rate so high?

A 5.50% rate is even higher than the average rate banks charge for loans to 小微 (micro and small) enterprises. These businesses are often considered higher-risk borrowers, yet the average rate for these loans in 2023 was only 4.78%.8

Fu Shou Yuan disclosed it borrowed RMB 200 mn at 5.50% in 2023.

Source: Fu Shou Yuan (2023)

Oh. I didn’t realise that… That’s really weird. I’ll have to think about that.

What was the last red flag you saw?

High turnover.

On 12 Dec 2025, the Board relieved Wang Jisheng of his CEO duties, though he remained as an executive director.9

That same day, Luo Zhuoping, an independent non-executive director resigned.10

Finally, on 13 Feb 2026, a week before the trading suspension, another non-executive director resigned.11

All departing staff confirmed they have no disagreements with the Board, and there are no other matters relating to their resignation that need to be brought to the attention of the shareholders of the Company or the Stock Exchange.

Later, on 18 Jun 2026, Fu Shou Yuan revealed that in Jul 2025, there were discussions on a mainland online forum alleging that the then-CEO Wang Jisheng, together with certain management of a subsidiary, breached compliance requirements for personal gain when operating projects of the subsidiary.12

Go figure.

Coming up next

Last Thu 25 Jun 2026, Reuters reported that Bumble Inc. is exploring a sale.13

I estimate the dating app generated ~ USD 200 mn of free cash flow to firm, against USD 867 mn enterprise value.

Could there be an opportunity in BMBL 0.00%↑?

I will explore this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in Fu Shou Yuan International Group Limited (1448 HK), either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.