Evolution AB: After falling -65%, how much lower can it go?

[First Take] Evolution AB (publ) (EVO SS)

About (13 Apr 2026)

Share price: SEK 605 (USD 65.87)

Market capitalisation: SEK 121 bn (USD 13 bn)

Enterprise value (EV): SEK 113 bn (USD 12 bn)

Average daily volume (ADV): SEK 430 mn (USD 47 mn)

NTM P/E: 10x

Time spent: 2 days

My Decision

Pass

Background

Evolution AB: After falling -65%, how much lower can it go?

Since 2021, EVO grew its earnings per share by +92%. Yet, its share price has fallen -65%.

Investors point to this and declare: “I am all-in! The fundamentals are sound. How much more can this fall!”

They are likely underestimating the downside risks.

In this post, I will discuss:

Why I believe the regulatory risks are higher than expected

Why Evolution looks likely to miss 2026 consensus estimates

Business model

Breakdown of 2025 revenue by players’ geographical region (EUR 2,067 mn; 0% YoY):

38% Asia (-1% YoY)

35% Europe (-6% YoY)

14% North America (+15% YoY)

8% Latin America (+8% YoY)

5% Others (+14% YoY)

EVO mainly earns commission from licensing its live casino content to customers like online casino operators. Commission is calculated as a percentage of the operators’ winnings generated via EVO’s live casino content.

In live casino, a game presenter runs the game from a casino table that is followed in real time via a video stream. The players (end users) make betting decisions on their devices like smartphones or computers.

According to EVO’s annual report, 54% of its revenue was derived from unregulated markets in 2025.

EVO’s customers include online casino operators like Flutter Entertainment plc (FLUT US) and DraftKings Inc. (DKNG US).

In 2025, its top customer accounts for 12% of its revenue. Together, the top 5 customers account for 39% of EVO’s revenue.

The closest public comparable is Playtech plc (PTEC LN), although its revenue mix is more heavily weighted toward regulated markets.

My reasons

Most of Asia’s revenue seems to be unregulated.

Asia is EVO’s most important market. It contributes ~38% of revenue in 2025. I believe most revenue from Asia is unregulated (i.e., operating in jurisdictions where online gambling is prohibited or has no legal framework).

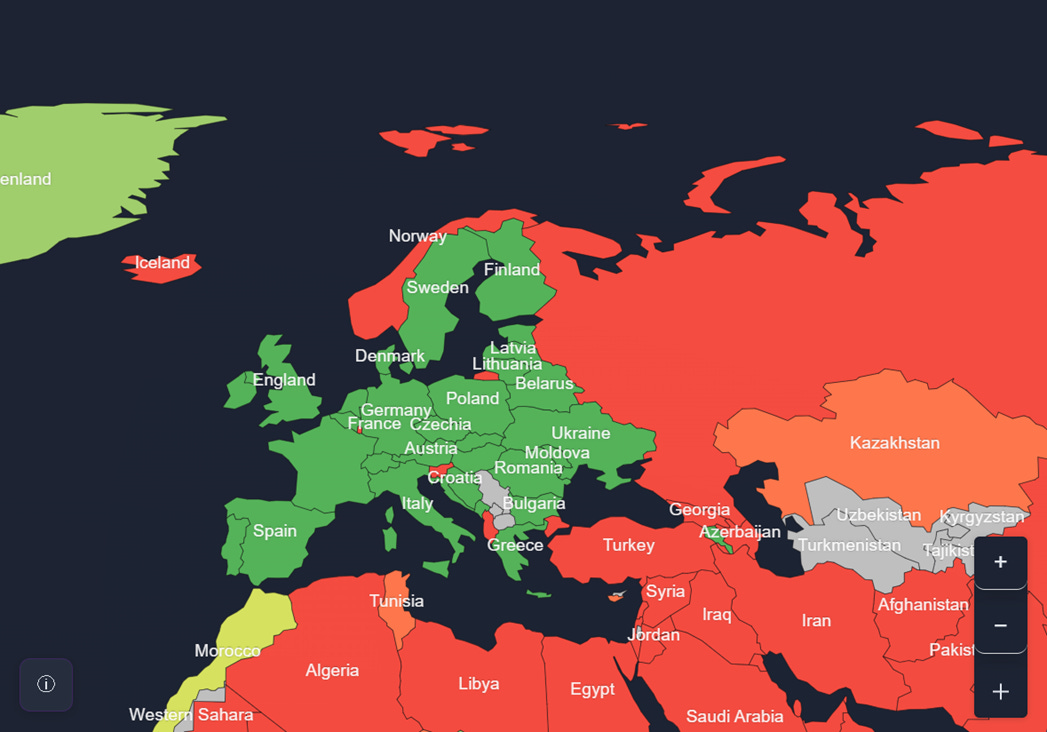

There are only about 6 countries in Asia where online gambling is legal. These include the Philippines and Sri Lanka. They are shaded green in the map below.

This handful of countries are not major economies. Together, they only account for ~3% of Asia’s gross domestic product (GDP).

Green: Regulated; Red: Prohibited; Grey: Unclear.

Source: Legal Pilot (2025)

Europe, where online gambling is mostly legal, contributes 35% of EVO’s revenue. Asia, where online gambling is mostly illegal, contributes 38% to 2025 revenue.

Green: Regulated; Red: Prohibited; Grey: Unclear.

Source: Legal Pilot (2025)

Taken together, these facts suggest most of EVO’s revenue in Asia is coming from countries where online gambling is illegal (red) or unregulated (grey).

The second reason why I believe most revenue from Asia is unregulated: EVO’s Asia growth surged after competitor PTEC started scaling down its Asian operations in 2018, following regulatory crackdowns.1

PTEC’s Asia revenue peaked at ~ EUR 283 mn in 2017, then fell -40% in 2018 and had shrunk so much by 2022 that it was no longer disclosed separately. By contrast, EVO’s Asia revenue was too small to break out in 2018, but by 2025, Asia accounted for 38% of total revenue.

Taken together, this evidence suggests that the majority of EVO’s Asia revenue likely originates from illegal markets.

Asia’s regulators are closing in.

EVO is facing severe headwinds in Asia. Revenue from Asia declined -1% in 2025. For a ‘growth’ company, this is a disaster.

EVO attributes this mainly to cybercriminals illegally streaming or copying its gaming content in the Asian market. However, I can’t help but question this.

Why is Playtech plc (PTEC), EVO’s main listed competitor, not reporting the same issue? Why are the cyberattacks so prevalent in Asia but not other regions?

I suspect regulatory crackdown is a bigger contributing factor.

EVO’s Asia revenue growth decelerated from +41% in 2023 to +19% in 2024, before collapsing to -1% in 2025. This coincides with the timing of regulatory crackdowns in Asia.

In 2024, Indonesia created a new task force and vowed to crack down on ‘blood sucking’ online gambling.2 In Jun 2025, Japan updated its law to prohibit the operation and promotion of online casino sites targeting Japanese users, including those hosted overseas.3 In Aug 2025, India’s parliament banned the online gambling industry.4

Regulation is tightening even in the Philippines, where online gambling is legal. After banning offshore gaming operators (POGO) in 2024, the Philippines ordered payment service providers to suspend in-app access to online gambling. Online gambling transactions declined by as much as -50% following the order.5

The bulls will argue that EVO has reduced unregulated revenue from 69% of revenue in 2018 to 54% in 2025. However, there is a risk that this % is understated.

According to InPractise, a research provider, a reporting change in 2018 led to significant changes in how EVO reports unregulated revenue. The true exposure remains unclear.6

The bulls may also argue that the regulatory risks are limited because EVO merely supplies the infrastructure for an online casino. It is the online casino operators’ responsibility to comply with the regulation, not EVO.

However, regulators like the UK Gambling Commission (UKGC) have stated that their strategy on combatting illegal gambling is to cause as much up-stream disruption as they can.7

To that end, in Nov 2024, the UKGC launched a review of EVO’s licence in the UK, as the regulator has found EVO is supplying unlicensed operators in the country.8 The investigation is still ongoing.

Consensus still too optimistic.

With regulatory crackdown accelerating in Asia, EVO’s most important market, the outlook for EVO looks bleak.

Yet, the consensus is forecasting revenue growth to recover from 0% in 2025 to +3% in 2026.9 This seems too optimistic.

Demand in 2026 looks set to be weaker than 2025. In 2025, contract liabilities declined -17%. Accounts payable declined -32%. Accounts receivable increased +11%, faster than revenue (0%). Days receivable increased +19% and reached 80 days, near an all-time high. Taken together, these working capital trends suggest near-term demand is weak. Some revenue may even have been pulled forward.

Earnout liability decreased in 2024 and 2025. Because it is based on the expected future performance of the acquirees, a decrease suggests future performance is weaker than initially expected.

Other matters: EVO scrapped dividends for 2025

For 2024, EVO paid EUR 572 mn dividends and spent EUR 500 mn on share buybacks. The total EUR 1,072 mn represents slightly more than 100% of net profit after tax in 2024. The most recent share buyback was done in Dec 2025.

On 18 Mar 2026, EVO scrapped its 2025 dividend, breaking from its long‑standing 50% payout policy. The company said it will update investors once 2026 capital allocation decisions are finalised.

There are 5 possible reasons why EVO paused its dividends:

Reinvest to revive its struggling business

Reserve for its litigation against PTEC

Share buybacks

Privatisation

Mergers & acquisitions (M&A)

Points (1) and (2) seem unlikely. EVO already has a lot of cash. In 2025, its cash and bonds are ~45% of revenue.

Some suggested the major shareholder, Kenneth Dart, may prefer share buybacks over dividends for tax reasons.10 Share buybacks could also make it easier for him to privatise EVO. If this were the main motivation, EVO would likely have announced a share buyback together with the suspension of dividends.

This leaves us with the final reason: M&A. I believe this is the most likely explanation. With organic growth stalling, it can make sense to rely more on inorganic growth.

There is a precedent. In Feb 2025, Joint Stock Company Kaspi.kz (KSPI US) paused its dividends around the same time it acquired Hepsiburada.

PTEC looks like a natural M&A target for EVO. While 92% of PTEC’s revenue comes from regulated markets, the figure for EVO is just 46%. Buying PTEC would instantly tilt EVO’s mix toward regulated markets and de‑risk its revenue base.

If EVO acquires PTEC, it could also eliminate the costly, distracting litigation between them. In Apr 2026, EVO sued PTEC, claiming that a 2021 report PTEC commissioned was defamatory and intended to damage EVO’s business.11

In Apr 2025, PTEC sold Snaitech, its Italian B2C casino operator. With this sale, it became primarily a B2B business, making it more aligned with EVO’s B2B model.

From PTEC’s perspective, a sale to EVO could therefore be attractive: it would end the ongoing litigation and give shareholders a clean exit.

Back in Feb 2022, Aristocrat Leisure Limited (ALL AU) nearly acquired PTEC for GBP 2.7 bn, but the deal collapsed after activist shareholders rejected the price.12

Since then, those activists no longer appear to be substantial shareholders.

If PTEC is acquired at a 40% premium today, shareholders would receive at least GBP 3.0 bn, including the special dividend of GBP 1.6 bn already paid in 2025. This is slightly more than the GBP 2.7 bn offered by ALL in 2022 and arguably reasonable given the bleaker outlook for the industry today.

For a good introduction to PTEC, I recommend Something’s Off’s analysis of the company.

Factors that could lead to a change in my decision

1. Revenue from legal and regulated markets increases to > 90% of total revenue

2. Strong evidence that overall revenue has stabilised

Coming up next

Thailand has one of the most underpenetrated international school markets in Asia. One listed operator is growing revenue every year.

This operator looks set to grow revenue at high-single-digit over the next few years. Yet, it trades at just 11x NTM P/E.

My next post covers whether it is worth buying for my personal portfolio.

Subscribers get it first. Free to join.

Subscribe for 2 to 3 analyses of global equities every week. Discover overlooked ideas and rethink familiar names. Published by Andrew Wong, ACA, CFA

Disclaimer: This is a record of my investment decisions and not financial advice. I may change my decisions at any time without notice. Use this only for educational and entertainment purposes. All analysis and opinions are my own and based solely on public information. EVO has not reviewed or endorsed this post. Do not rely on this for your investment decisions. I do not hold any positions, long or short, in EVO.

References

Tikr (2026)

As I like to say, the bottom is zero. 😛

It does look compelling at present prices, however.

Enjoyed reading, thanks for the writeup - the argument regarding the bearish outlook for Asia regulation was clear and well-researched.