Crocs: Ugly shoes, beautiful stocks?

[First Take] Crocs, Inc. (CROX US)

Disclaimer: This is a record of my investment decisions and not financial advice. I may change my decisions at any time without notice. Use this only for educational and entertainment purposes. All analysis and opinions are my own and based solely on public information. CROX has not reviewed or endorsed this post. Do not rely on this for your investment decisions. I do not hold any positions, long or short, in CROX.

About

Share price: USD 101.95

Market capitalisation: USD 4,877 mn

Enterprise value (EV): USD 6,360 mn

Average daily volume (ADV): USD 132 mn

NTM P/E: 7x

My Decision

Pass

Background

Crocs: Ugly shoes, beautiful stocks?

“You can buy the stocks, but not the shoes”

That’s what my girlfriend said when I told her I am interested in Crocs. At 7x NTM P/E and 10% FCFF yield, Crocs looks very attractive.

Much to her chagrin, I will probably buy the shoes, but not the stocks.

In this Substack post, I discuss the 3 key reasons I passed on the shares: (a) High fashion risk; (b) Make China Crocs Again? and (c) Peak margins?

In the final analysis, Crocs, Inc. (CROX US) is highly dependent on fashion trends. I am as good at forecasting fashion trends as I am at calling coin flips.

High frequency data like Google Trends are already showing weakness. If its clogs continue falling out of fashion, like in 2013, Crocs may unexpectedly slip into losses.

Business model

Breakdown of 2025 revenue (USD 4,041 mn; -1% YoY):

82% Crocs Brand (+1% YoY)

18% HEYDUDE Brand (-13% YoY)

Crocs Brand is CROX’s original line of colourful foam clogs, sandals, and related casual shoes, plus Jibbitz charms for personalisation.

HEYDUDE Brand is a casual footwear line, founded in Italy and acquired by CROX in 2022. It offers lightweight slip‑on shoes and loafers with relaxed styling.

In 2025, CROX 0.00%↑ earns ~48% of its revenue from wholesale channels. These include domestic and international multi-brand retailers, mono-branded partner stores, e-tailers, and distributors.

Direct-to-consumer (DTC) accounts for ~52% of its revenue. These include company-operated e-commerce sites, third-party marketplaces, company-operated full-price retail stores, outlet stores, and kiosks/store-in-store locations.

In the past 3 years, no single customer contributed 10% or more of consolidated revenue.

In 2025, CROX’s top 2 suppliers accounted for 73% of its production. These 2 suppliers operate mainly in Vietnam and China.

The closest public comparables are Deckers Outdoor Corporation (DECK US), Birkenstock Holding plc (BIRK US) and Steven Madden, Ltd. (SHOO US).

For a detailed look at CROX’s business model, check out Leeder Capital’s post. Although we arrived at different conclusions, on Substack, his post contains the best description of CROX’s business and its recent issues.

My reasons

High fashion risk. Moody’s, a credit rating agency, rates CROX’s debt as junk.1 Why?

Moody’s cited a key factor being CROX’s high fashion risk as a result of its significant exposure to the clog style. This represents an estimated over 50% of revenue and is key to its brand identity.

CROX launched its clogs in 2002, and it rapidly became a global fad by the mid‑2000s. Its popularity peaked in 2007 before stabilising around 2012.

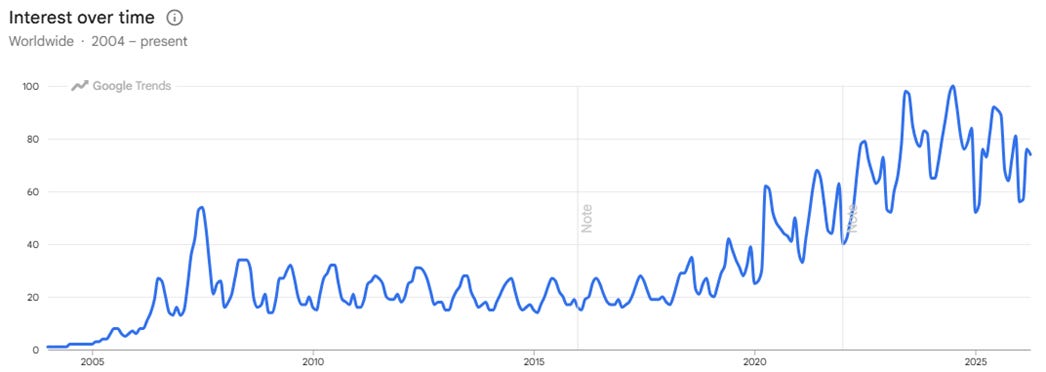

Between 2013 and 2017, CROX became less fashionable. This shows up in the gradual decline of Google Search interest. CROX struggled.

Source: Google Trends

The unexpected decline in demand left CROX with excess inventory and underperforming retail stores. Margins were squeezed by the heavy discounts to clear inventory and the high fixed costs of running many full-price retail stores.

Operating profits never recovered to the highs achieved in 2012 until 2020, when COVID-19 lockdowns brought Crocs back into fashion again.

Today, it seems like CROX is yet again on the wrong side of the fashion trend. Google Trends shows interest in Crocs has peaked in 2024. CROX may now be entering another period of declining popularity.

That said, there seems to be some stabilisation. Interest in Jan 2026 is slightly higher YoY.

After significant provision for doubtful receivables in 2023 and 2024, CROX finally recovered some doubtful receivables in 2025.

The decline in purchase commitments for materials and supplies decelerated, suggesting management still sees demand declining in 2026, but slower than before.

Inventory donations held steady in 2025, and inventory days reached close to a record low in the fourth quarter. These trends indicate healthier inventory levels, which may reduce margin pressure in 2026.

Will Crocs’ popularity stabilise? Or will the next few years be a repeat of 2013 to 2017? At least for me, I find it challenging to forecast long-term fashion trends.

Management seems to believe the same. To mitigate its high fashion risk, previous CEOs had been trying to diversify from clogs.

In 2010, then-CEO John McCarvel tried to diversify CROX by introducing new lines such as high heels, dress shoes and golf shoes. The idea was to turn CROX into a broad lifestyle brand rather than just a clogs-maker.

By 2014, it was clear this diversification attempt had failed, leaving Crocs with high overhead and excess inventories. CEO McCarvel got the boot.

The current CEO Andrew Rees was tasked to turnaround CROX. CEO Rees began closing underperforming stores and cutting back many of these lines to refocus on clogs. By 2017, CROX finally returned to positive operating profits.

But I suppose the high fashion risk resulting from over-reliance on clogs never left CEO Rees’ mind. If it is difficult to diversify organically, why not try getting it done with a big acquisition?

In 2022, CEO Rees led CROX’s acquisition of HEYDUDE, a casual footwear brand that sells lightweight, slip‑on shoes. CROX bought HEYDUDE for about USD 2.5 bn. This was roughly one‑third of CROX’s market capitalisation.

CROX framed the acquisition as moving from a single‑brand company to a multi‑brand portfolio, diversifying beyond clogs and into relaxed slip‑on/loafer silhouettes.

The acquisition was a disappointment. CROX admitted as much when it wrote down USD 738 mn of HEYDUDE’s goodwill and other intangibles in 2025. This was 83% of the year’s operating profit.

On a side note, I worry the write-down may not be sufficient. Some of the key assumptions and forecasts used to estimate the write-down seem optimistic: annual revenue growth rates averaging ~ 8% and projected EBITDA averaging ~20%.2

HEYDUDE’s revenue declined -14% in 2025 and is expected to decline another -8% in 2026. In 2025, its EBITDA margin was only ~10%.

On the other hand, CROX used 15% discount rate, which seems on the high side. CROX did not provide further details.

This is the main reason I decided to pass on CROX. The company’s reliance on a single product line exposes it to high fashion risk. Historical precedents such as 2013 to 2017 demonstrates that when fashion trends shift away from CROX, the company will likely experience substantial challenges.

CROX’s recent performance and Google Search interest suggest that another shift away from Crocs may be underway. But I lack the data to confidently predict long-term fashion trends.

Make China Crocs Again? With revenue from North America declining -9% in 2025, the bulls point to China as CROX’s growth opportunity.

Revenue from China grew +64% in 2024 and another +30% in 2025. China is now CROX’s second largest market, accounting for ~ 8% of revenue.

However, I am not so certain about the growth opportunity in China. Fashion trends in China are also difficult to predict.

In 2014 Q3, CROX saw a sharp drop in wholesale volume and double-digit declines in retail sales at comparable stores in China, while US same store sales increased by 10%.3

Despite entering the Chinese market in 2006, CROX only managed to get 8% of its revenue from China by 2025. This is only slightly up from 6% in 2016, the earliest data I can find.

Unless there is strong evidence that the demand from China is durable, I would be cautious about extrapolating the currently strong demand in China.

Peak margins? Since COVID-19, Crocs Brand’s gross profit margin (GPM) has hit record levels, prompting concerns about its long-term sustainability.

It appears unlikely that such a high gross profit margin can be maintained long term, especially since demand seems to be falling. However, you could argue that it is sustainable because direct-to-consumer (DTC) now plays a bigger role in consolidated revenue.

In 2025, DTC contributed 52% to group revenue, up from 47% in 2016. At first glance, DTC should carry significantly higher margins than wholesale because CROX captures the retail margin.

I am not so sure about this. In 2025, 61% of Crocs Brand and 100% of HEYDUDE company-operated retail stores are outlet stores.4 In 2016, only 42% of company-operated stores are outlet stores.5

Outlet stores are targeted at value shoppers. They mainly sell discontinued and overstocked merchandise directly to consumers at discounted prices.

The margin gains from higher DTC contribution may be offset by a shift toward outlet stores.

For this first take, it is not cost‑effective to quantify these effects.

However, recent results seems to justify concerns over the sustainability of such high margins. In 2025, operating profit margin declined at both Crocs Brand (36% to 33%) and HEYDUDE Brand (17% to 10%).

The bulls would argue that CROX’s pricing power can mitigate margin weakness.

The average selling prices (ASP) for Crocs Brand and HEYDUDE Brand are only USD 25 and USD 32 respectively. Compared to Skechers (~USD 50 to 70) and Birkenstock (~USD 130 to 140), there seems to be a lot of room for CROX to raise prices.

However, the ASP that CROX reported is a blend of wholesale and DTC, including discounted outlet prices. The ASPs for Skechers and Birkenstock are retail prices. The retail prices of Crocs Brand and HEYDUDE Brand are closer to USD 50 and USD 70 instead.

I could not find any historical evidence of pricing power. In the past 10 years, ASP of Crocs Brand increased at 3.2% p.a., barely outpacing 3.0% p.a. inflation.

In Aug 2025, CEO Rees reported “They’re [customers] not even going to the stores and we see traffic down,” he said, adding the current conditions are preventing the company from raising prices to compensate for the impact of tariffs on countries where Crocs produces footwear.6

Factors that could lead to a change in my decision

1. Strong evidence that CROX’s fashion risk is lower than I expected (e.g. core customers view Crocs as a utility footwear rather than a fashion statement)

2. Convincing evidence that current margins are sustainable (e.g. management provides detailed breakdown of unit economics)

3. Management is making better than expected progress in turning around HEYDUDE (e.g. return to positive revenue growth and margin expansion)

4. Significant decline in valuation without deterioration in business fundamentals

Coming up next

Next week, I plan to publish my analysis of Evolution AB (publ) (EVO SS).

The bull case revolves around EVO as a cash-gushing, market‑dominating “Netflix of live casino” that’s still priced like a risky niche player despite its towering margins, fortress balance sheet, and long global growth runway.

How true is this story? Will I shortlist EVO for my personal portfolio?

I also plan to update you on SISB Public Company Limited (SISB TB), the largest operator of international schools in Thailand. Revenue is expected to grow high-single digit, yet SISB trades at only 11x NTM P/E.

Subscribers get priority on updates. Click on the button below to subscribe for free today.

Subscribe for 2 to 3 analyses of global equities every week. Discover overlooked ideas and rethink familiar names. Published by Andrew Wong, ACA, CFA

Interesting arguments, thanks for the write-up.

As promised in the “Coming up next” section in my analysis of Crocs, Inc. (CROX), I’ve just published my thoughts on Evolution AB (publ) (EVO SS).

I decided to pass on EVO.

I believe the market is underestimating the regulatory risks.

Based on my analysis of working capital trends, demand in 2026 looks set to weaken further. Yet, the consensus is still too optimistic.

Read my analysis here: https://angsanaanderson.substack.com/p/evolution-ab-after-falling-65-how?r=5rl2u5