Craneware: Good business, temporary headwinds?

Why I see an opportunity in the top healthcare software in the US

[Shortlist] Craneware plc (CRW LN)

Give me your pitch in one minute.

Shortlist Craneware plc (CRW LN) as a long. The shares are near a 5-year low because they guided FY2026 revenue below consensus.

However, the market is likely over-reacting. Craneware is a good business, and the headwinds are likely temporary. That’s the first point.

Second point: attractive capital returns. Over the next year, Craneware will return ~ 7% of its market capitalisation to shareholders through buybacks and dividends.

I estimate ~ 8% free cash flow yield on enterprise value. For this growth potential, this is an attractive ~4% premium over US 10-year government bond.

Sounds interesting. Basic stats? Is it liquid enough?

Share price: GBP 11.86

Market capitalisation: GBP 402 mn (USD 538 mn)

Enterprise value (EV): GBP 391 mn (USD 524 mn)

Average daily volume (ADV): GBP 3 mn (USD 4 mn)

NTM P/E: 14x

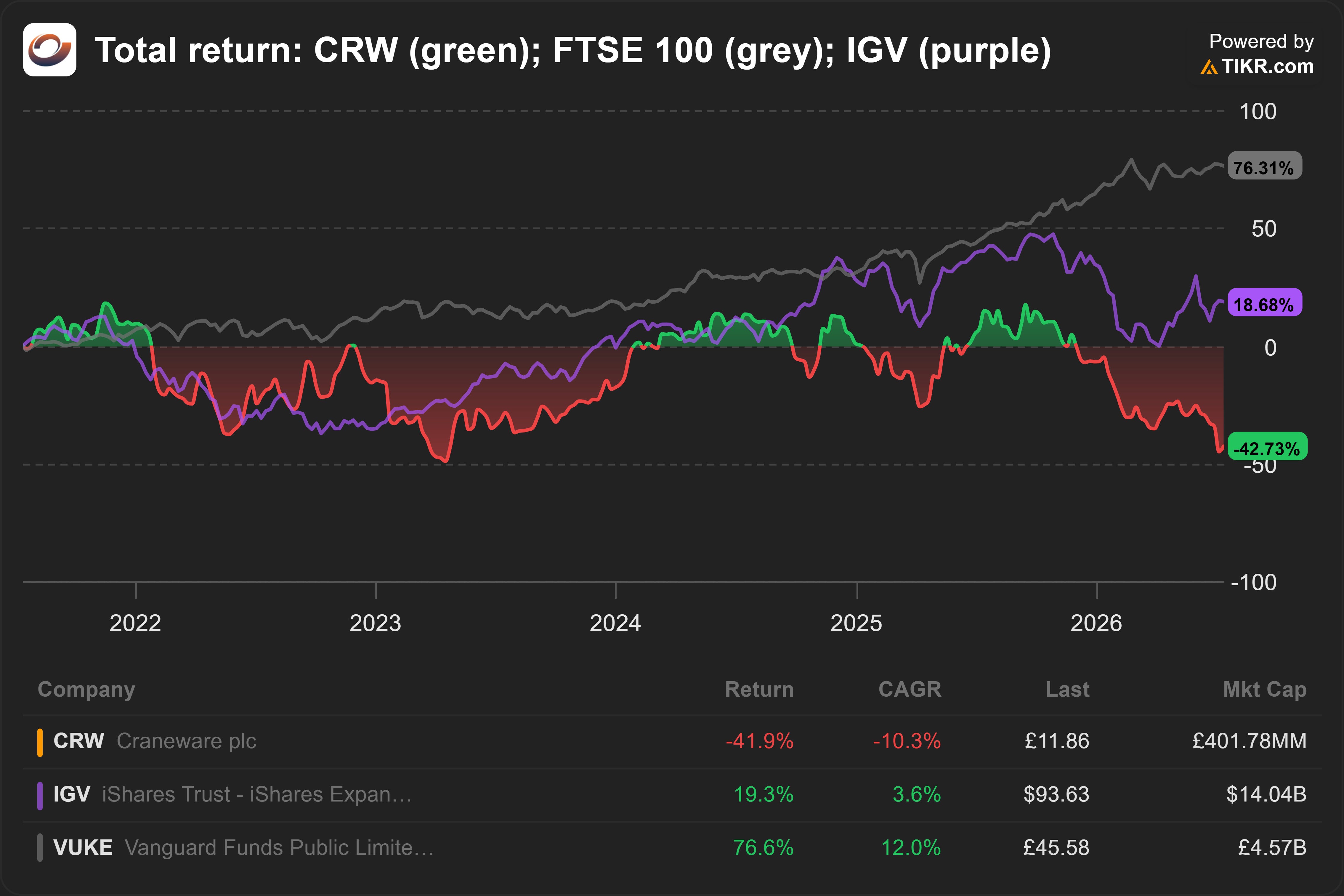

People are trading CRW like a software stock. Look at the sell-off in early 2026.

The shares are moving together with IGV, the US software ETF. Not much correlation with the FTSE 100.

Yes. But I believe the threat from AI is overblown. It is a vertical software, difficult to replicate.

Ok. Tell me what Craneware does.

They sell software to 40% of all hospitals in the US.

Craneware got its start selling software to manage hospital chargemasters. Hospital chargemasters are comprehensive databases containing the pricing for every billable service a hospital provides.

Without Craneware’s software, the hospital would be forced to manage these massive, constantly changing lists manually. A process that becomes too tedious and highly error prone.

So, Craneware’s software is the bridge between the hospital’s treatment and their revenue?

Exactly.

They have significant goodwill. What is that about?

Its software now extends beyond managing chargemasters.

In 2021, Craneware acquired Sentry Data Systems (SDS). SDS sells software that helps hospitals manage compliance with the 340B program. This is a US government program that allows hospitals to purchase prescription drugs at steep discounts. It’s very complex.

By combining its existing hospital clients (who used them for billing and chargemaster software) with SDS’s clients (who used them for pharmacy procurement and 340B compliance), Craneware achieved ~40% market share of all registered US hospitals.

What proportion of revenue comes from chargemaster vs SDS?

Craneware no longer discloses revenue from chargemaster and SDS separately because, after the acquisition, they integrated into a single cloud platform called Trisus.

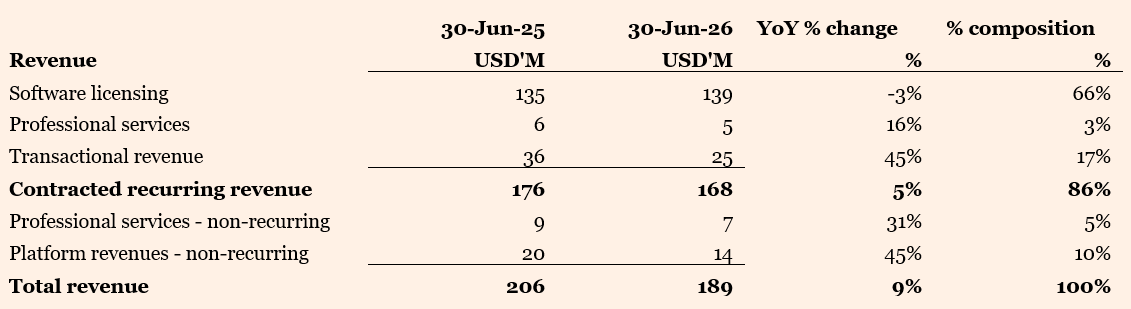

This is how they disclose their revenue now:

86% revenue is recurring.

Software licensing declined -3% in FY2025, but that’s mainly because of reallocation to transactional revenue. Overall recurring revenue still grew +5% YoY.

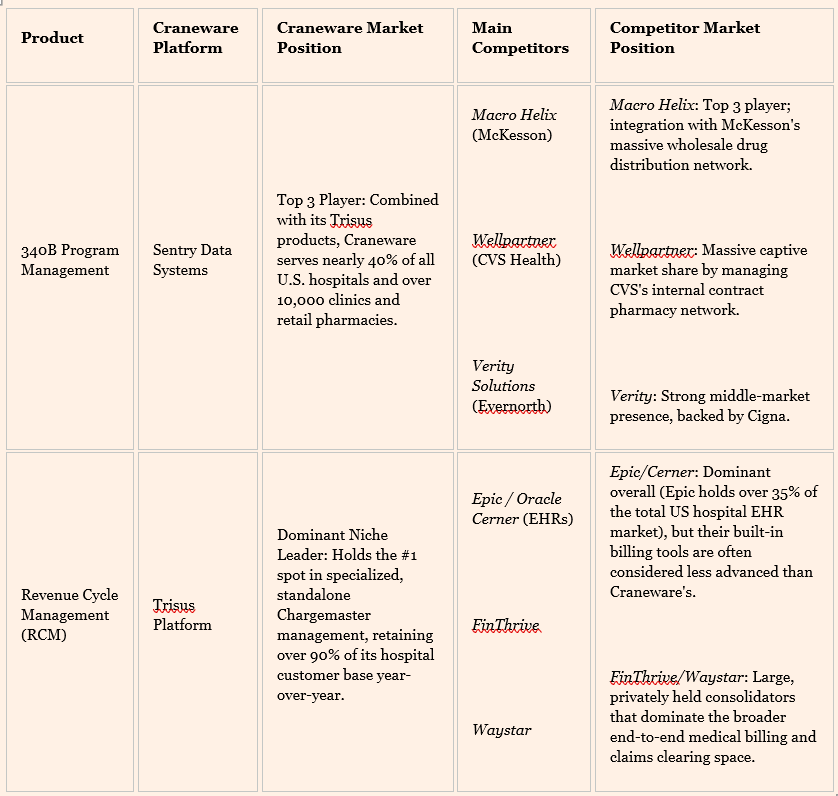

Competitors?

As far as I can tell, Craneware is the largest player, and the only listed pure-play. That’s why there’s not a lot of public information.

Here’s what Perplexity could gather:

Ok. That’s clear enough.

I saw the company released a trading update on 3 Jul 2026. The shares tanked more than -30% in just one day. What happened?

Craneware downgraded revenue for FY2026.

They now expect flat revenue, between USD 205 mn to USD 208 mn. Before the update, consensus expected revenue to grow +10% and reach USD 226 mn.

Why did Craneware downgrade revenue?

Drugmakers increased restriction on the distribution of discount-eligible medicines under the US government’s 340B drug pricing program.

This caused delays in hospitals receiving their 340B-eligible drugs. Because Craneware recognises a significant portion of this revenue only after a hospital receives the drugs, the drugmakers’ restrictions effectively pushed revenue into FY2027.

However, the consensus treats this revenue as ‘lost’ rather than delayed.

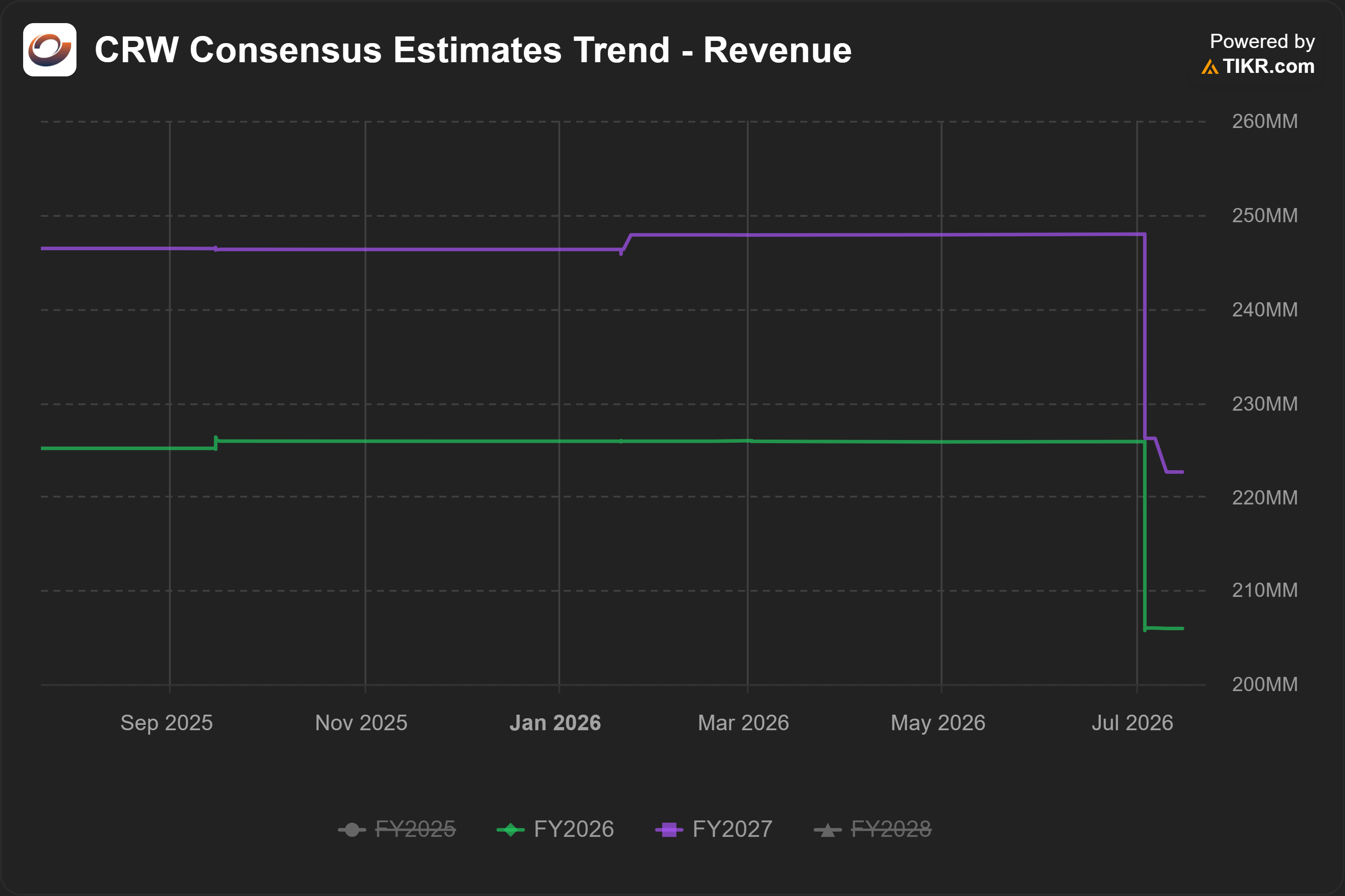

Look at the chart below. It shows the trend in consensus’ estimate of revenue for FY2026 and FY2027.

After the trading update, consensus cut their estimate of FY2026 revenue. At the same time, they also cut their estimate of FY2027 revenue. They did not adjust FY2027 up.

What makes you think the revenue is delayed, not lost? Why is this headwind temporary?

Safety-net hospitals rely the most on 340B discounts. If they do not get 340B discounts, they cannot sustain operations.

These hospitals look after the poor. Their operating margins average ~1%1, compared to ~20% net income margins at the average drugmaker2.

As you know, Trump has been pushing the drugmakers to lower prices.3

Gee… We don’t make bets on Trump here.

This is not a political bet.

Even if the drugmakers win, there will be opportunities for Craneware.

One of the main ways the drugmakers are restricting 340B drugs is through mandatory data submission. Drugmakers are requiring hospitals to submit detailed, itemised medical and claims data for every single 340B drug dispensed.

Which software will be best positioned to help the hospitals organise and submit this data?

So, you’re saying the headwind is temporary.

If the hospitals win, the 340B drugs get delivered in FY2027. Revenue is effectively pushed into FY2027.

If the drugmakers win, the hospitals will need to submit detailed claims data. Craneware, being the software serving 40% of all hospitals in the US, will be best positioned to help them.

Yup.

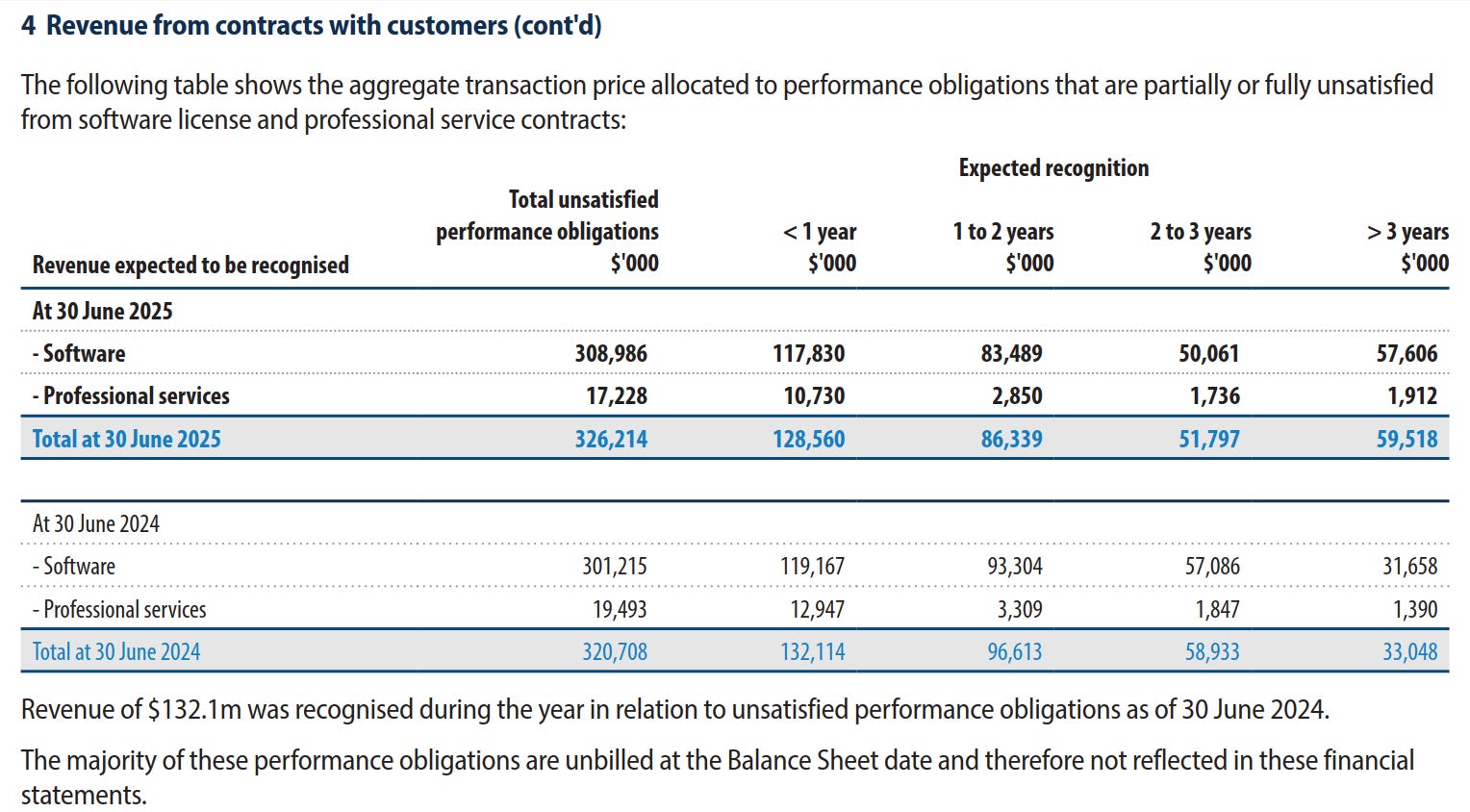

Look, Craneware is a good business. It’s not in terminal decline.

Here’s the future revenue it is expecting to recognise. Revenue expected to be recognised > 3 years later actually grew.

Source: 2025 CRW AR

These are just revenue from existing contracts. We have not even included new contracts.

Strangely, the consensus seems to be missing this data. I did not find much discussion about this.

That’s interesting. What other data do you have?

Trade receivables remain healthy.

As of 30 Jun 2025, 57% of trade receivables are current and not overdue. This is an improvement from 46% the prior year.

As of 31 Dec 2025, management made provision for 8% of trade receivables, an improvement from 10% the year before. This suggests management is not seeing significant difficulties in its customers.

If the business is in decline, customers would be delaying payments and provisions would be surging. That’s not what we’re seeing here.

Anything else?

Existing customers are spending more.

Net revenue retention (NRR) is the percentage of revenue retained from existing customers. In H1’26 and FY2025, Craneware reported NRR of 103% and 107%.

This sounds promising.

But is this the right time? I don’t want to get in and then get blown up right after.

I don’t see a nasty surprise around the corner.

Advance payments from customers, a leading indicator of revenue, finally returned to growth. In H1’26, it grew +2% YoY. It declined -2% in FY2025.

How about revision in consensus estimates?

The same chart above shows consensus estimates for revenue have largely stabilised. The chart is similar for EPS estimates.

Both the CEO and Chairman bought shares after the price collapsed in the wake of the trading update.

I heard Bain Capital offered GBP 26.50 per share, but the board rejected it. They believed it undervalued the company.[4]4

This is a catalyst.

I believe the founder/CEO will likely want to sell. He is the single largest individual shareholder, owning ~9% of the company. Keith is already 56 years old, and there is no clear successor.

The most important question is price.

To get a price way above GBP 26.50, the company will need to show strong growth. That will probably only happen in FY2027 and beyond.

Ok. That’s fine, our investment horizon is 3 to 5 years.

You have my go-ahead to develop this thesis. What should we focus on?

Get more evidence to support my hypothesis that the headwinds are temporary.

Great. Go do that.

Coming up next

In Where are we in the semiconductor cycle?, we looked at how the price and cost of memory chips can predict the semiconductor cycle.

We can also supplement our analysis with working capital trends.

That’s what I will explore in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in CRW, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.