Block: The illusion of top-line growth

[First Take] Block, Inc. (XYZ US)

Summary

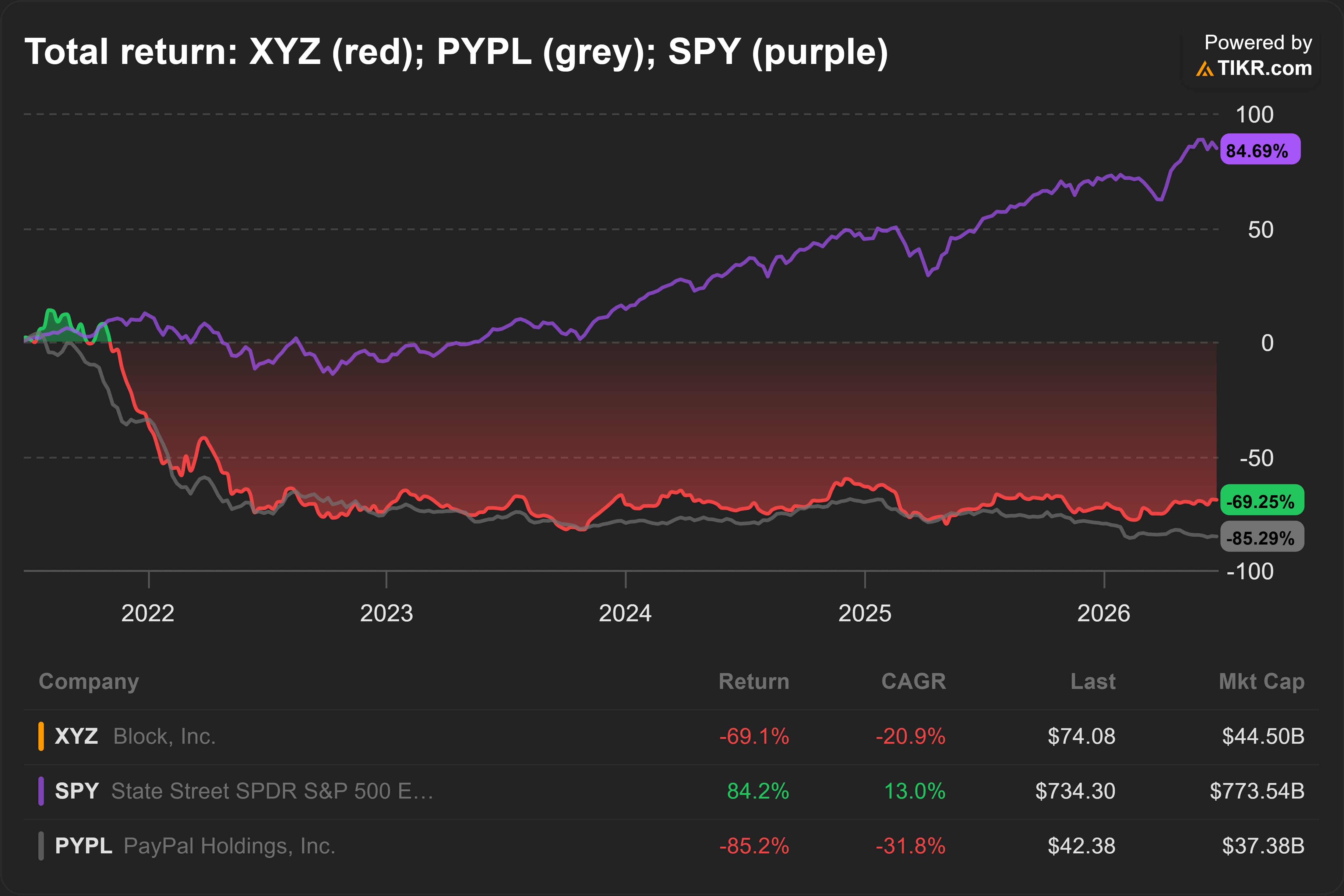

I passed on Block, Inc. (XYZ US), PayPal’s rival.

Initially, I thought XYZ looks more attractive. Although Block trades more than twice PayPal’s NTM P/E, it is expected to grow much faster.

However, I concluded PYPL is more attractive. Its customers seem less saturated, and its loan book less risky.

The market also seems to have not fully recognised the regulatory risks surrounding XYZ.

Finally, I explain why Block’s faster revenue growth was misleading, and why a bet on Block is also a bet on Bitcoin.

About (25 Jun 2026)

Share price: USD 74.08

Market capitalisation: USD 44,501 mn

Enterprise value (EV): USD 45,280 mn

Average daily volume (ADV): USD 424 mn

NTM P/E: 18x

Time spent: ~2 days

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Pass

Business model

Gross profit is more meaningful because headline revenue is significantly inflated by how XYZ 0.00%↑ accounts for its Bitcoin transactions. More on this later.

Breakdown of 2025 gross profit (USD 10,417 mn; +16% YoY):

59% Commerce Enablement (+10% YoY)

37% Financial Solutions (+31% YoY)

4% Bitcoin Ecosystem (0% YoY)

The Commerce Enablement segment enables customers to transact. It includes Square payment processing, Cash App Card, Cash App Pay, and all Buy Now, Pay Later (BNPL) products (Afterpay).

Square allows businesses to accept card payments, whether in-person or online. Its customer base is concentrated among small-to-medium-sized businesses.

Cash App is a popular digital wallet. Customers can make peer-to-peer payments, make direct deposits to earn interest, and borrow money. The customer base skews towards lower-income Gen Z and Millennials who are underbanked.

The Financial Solutions segment includes banking and money management tools like Square Loans and Cash App Borrow.

Square Loans provides loans to businesses that use Square’s point-of-sale hardware and payment processing software. Cash App Borrow is a short-term, personal micro-lending feature embedded within the Cash App digital wallet.

The Bitcoin Ecosystem segment includes all Bitcoin-related activities, including buy/sell functionality in Cash App, Bitcoin withdrawal fees, and hardware projects like Bitkey and Proto.

In 2025, XYZ earned approximately 87% of its gross profit from the United States, while international markets, heavily led by its Afterpay operations in Australia, accounted for the remaining 13%.

The most relevant public comparable is PayPal Holdings, Inc. (PYPL 0.00%↑ US). Though, there are important differences which we will discuss later.

My reasons

PYPL looks more attractive

PYPL’s customers appear less saturated. In my previous post, I discussed how the market is under-recognising PYPL’s growth potential.

PYPL’s BNPL volume is ~ USD 176 per monthly active user (MAU). The US industry average sits significantly higher at USD 848 per active BNPL user.1

I estimate the same number for XYZ is ~ USD 910 per MAU. Of course, this is not an apples-to-apples comparison because this includes non-BNPL lending.

But if you consider that Cash App users skew towards lower-income population2, XYZ’s customers are likely closer to their borrowing limits than PYPL’s.

PYPL’s loan book looks less risky. I estimate PYPL’s net charge-off (NCO) rate ~ 6.0%, lower than XYZ’s 7.8% in 2025.

XYZ’s NCO rate will likely rise. Its NCO rate in 2025 is unduly low because XYZ started retaining more loans on its balance sheet only from Q2’25.

There is another risk that I believe the market has not fully appreciated.

Has regulatory risk been fully priced in?

Short report in 2023. In Mar 2023, Hindenburg Research, a short seller, accused XYZ of overstating its active user metrics while being complicit with fraud by prioritising growth over compliance. The short seller pointed to the insiders’ stock sale as their motive.3

USD 255 mn penalties and restitution. In Jan 2025, the Consumer Financial Protection Bureau (CFPB), a government agency, ordered XYZ to pay USD 55 mn fine and up to USD 120 mn compensation to consumers.

The CFPB found “Block allowed fraud to proliferate, closed cases of reported fraud without even opening a legally required investigation.”4

XYZ also agreed to pay an USD 80 mn fine imposed by states that alleged its money transfer service Cash App violated banking laws.5

DOJ investigations are ongoing. In Q1’26, XYZ accrued USD 240 mn as an estimate of its loss to settle the Department of Justice (DOJ)’s investigation.

XYZ also warned that “… it is reasonably possible that the ultimate resolution could result in losses in excess of the amount accrued and such losses could be material. The Company cannot provide any assurance that the ultimate resolution will not have a material adverse effect on the Company.”6

Is culture appropriate? Ultimately, the Hindenburg report and ensuing regulatory issues highlight a risk that the aggressive growth culture may have compromised controls.

Banks and fast growth usually don’t mix well. When banks chase aggressive growth, they often unwittingly sacrifice healthy controls to hit those growth targets.

Exposure to Bitcoin

Revenue growth depends on Bitcoin. At first glance, XYZ looks more exciting than PYPL. In 2020, XYZ more than doubled its revenue. PYPL only grew a meagre +21%.

The difference is largely because of accounting.

XYZ’s 101% revenue growth was primarily driven by its Bitcoin revenue. XYZ buys Bitcoin and resells them to its customers. It records the gross value of these Bitcoins as revenue, which will naturally increase during a rally. Without this, XYZ’s revenue would have grown only +17%.

PYPL also offers Bitcoin. But because PYPL only facilitates the Bitcoin transaction, it records only its processing fee as revenue.

That’s why I said faster revenue growth is not always better. It’s equally important to dig beyond the accounting and understand the economic reality.

In accounting parlance, we call this the principal vs agent problem.

Imagine you’re an investor trying to value a loss-making company. P/E does not work because earnings do not exist.

So, you use price/revenue. If the company incorrectly records gross revenue, slapping a price/revenue multiple on it will inflate its valuation. You’ll overpay.

In fact, I’ve seen multiple cases like this. But that’s a story for another day. Maybe I’ll share some cases with my subscribers, if there’s enough demand. Let me know in the comments.

XYZ holds Bitcoin. During Q1’26, XYZ reported USD 173 mn remeasurement loss on its Bitcoin investments. This is slightly bigger than its USD 172 mn operating loss.

Although the loss is non-operating, it is still an economic loss for shareholders.

As of Q1’26, XYZ still holds ~ USD 617 mn of Bitcoin.

Bitcoin exposure likely to increase. CEO Jack Dorsey is a big fan of Bitcoin.7

Nothing wrong with that. I just don’t have enough knowledge or skills to take a position on Bitcoin right now.

Factors that could lead to a re-assessment of my decision

Evidence of under-recognised growth potential (e.g. new revenue streams).

Resolution of the DOJ investigation, and strong evidence that the culture prioritises healthy controls.

XYZ reduces its exposure to Bitcoin, or I have enough information to take a position on Bitcoin.

Coming up next

Fu Shou Yuan International Group Limited (1448 HK) was a market darling.

At its peak in 2021, shares in the funeral services provider changed hands at HKD 8 per share. Investors expected booming business from COVID-19.

But it all came crashing down.

In Mar 2026, the Hong Kong Stock Exchange suspended trading in Fu Shou Yuan’s shares. There were questionable transactions spanning from 2016 to 2025.

The suspension didn’t come as a complete surprise to me. The company was already flashing red flags years ago.

What were the red flags?

I will explore this in my next post.

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in XYZ, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.