Australian Clinical Labs: Why I see an opportunity in Australia's pathology service provider

[Shortlist] Australian Clinical Labs Limited (ACL AU)

Summary

I shortlisted Australian Clinical Labs Limited (ACL AU).

Consensus seems to be pricing little to no growth. However, the business can likely grow revenue at mid-single digit p.a.

The market may be underestimating ACL’s medium-term growth from pathology indexation, demographic tailwinds, and a recovery in GP attendance.

ACL appears to be a good business going through temporary pressure.

Despite being smaller than its closest competitor, ACL earns a superior ROA. Margin improvement suggests the recent revenue decline is driven more by portfolio clean-up than by structural deterioration.

I estimate sustainable capital returns at ~10% of market capitalisation. This is an attractive ~5% premium over Australia 10y government bond yield.

On 18 May 2026, KKR, a private equity (PE) firm, quietly disclosed it increased its stake to 8.2%, up from 7.2%.1

About (25 May 2026)

Share price: AUD 1.99

Market capitalisation: AUD 370 mn (USD 265 mn)

Enterprise value (EV): AUD 663 mn (USD 475 mn)

Average daily volume (ADV): AUD 1.5 mn (USD 1.1 mn)

NTM P/E: 11x

Time spent: ~1 day

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

Shortlist

Background

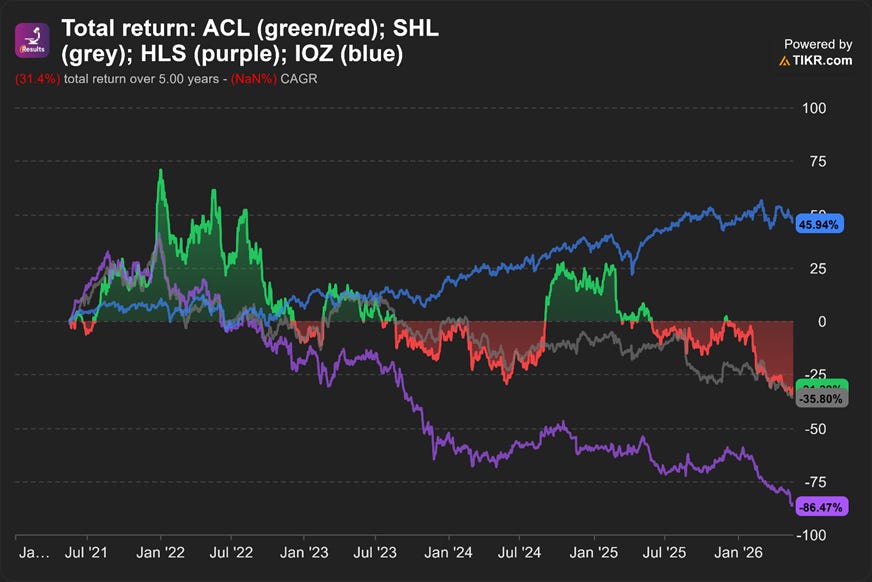

ACL’s share price fell -30% in a year. KKR responds by lifting its stake to 8%.

Why are they buying more when everyone else is selling?

I believe the market is underestimating ACL’s growth potential and overreacting to short‑term headwinds.

It runs a high‑quality business with a clear path to recovery, yet it’s still priced like the problems are permanent.

In the last twelve months, capital returns were about 13% of its market cap. I believe such attractive capital return is sustainable.

Maybe that’s what KKR sees.

Business model

ACL’s financial year ends in June. Unless stated otherwise, all time references will follow the company’s financial year. For example, FY2025 refers to the year ending on 30 Jun 2025.

ACL provides pathology diagnostic services in Australia. This involves the collection, examination and testing of body tissues, fluids, and cells to analyze diseases and medical conditions.

In FY2025, the company recognised revenue of AUD 741 mn (+6% YoY). ACL earns all its revenue in Australia.

~63% of revenue comes from community pathology. ACL operates 50 National Association of Testing Authorities (NATA) accredited laboratories and 1,288 approved collection centres (ACCs) from which it collects samples for community pathology.

ACL’s ACCs are mostly co-located at medical centres, where ACL leases an area within the medical centre and provides an ACL employee to collect samples.

~15% of revenue comes from specialist outpatient and 11% from inpatient hospitals. The remaining 11% comes from commercial contracts. For example, contracts with the Australian Defence Force (ADF).

Medicare bulk billing accounts for ~70% of ACL’s revenue.

This is a payment arrangement under Australia’s national health insurance scheme where a healthcare provider directly bills the government (Medicare) for a medical service, rather than charging the patient. The patient does not have to pay anything out-of-pocket.

Because pathology is a highly regulated and consolidated industry, ACL likely sources its large-scale testing equipment and proprietary chemical reagents from major global medical device manufacturers like Roche Diagnostics, Siemens Healthineers, Abbott, or Beckman Coulter.

The closest public comparables are Healius Limited (HLS AU) and Sonic Healthcare Limited (SHL AU).

SHL is the largest player in Australia with ~51% revenue market share. I estimate HLS and ACL hold ~30% and ~18% respectively.

SHL earns ~36% of its revenue from Australia, with the remaining mainly from United States and Germany. Both HLS and ACL operate purely in Australia.

My reasons

Under-recognised growth?

Consensus is pricing no growth. The iShares Core S&P/ASX 200 ETF (IOZ AU), which tracks the 200 largest listed companies in Australia, trades on a P/E ratio ~21x.2

At 11x NTM P/E, the consensus seems to be pricing ACL for no or low growth indefinitely. Tikr shows that the consensus expects -1% revenue decline in FY2026.

Investors dismiss ACL due to an apparent lack of pricing power.

The company charges for its pathology services based on the Medicare Benefit Schedule (MBS), which in turn, is determined by the Australian government.

For more than 20 years, MBS rates for most pathology services have not been increased to keep pace with inflation (indexation).

Likely to grow at least MSD. However, ACL is likely to grow revenue at mid-single digit (MSD) p.a. over the long-term.

The government has announced that, starting from Jul 2025, certain pathology services will return to annual indexation.3 The MBS indexation factor applied most recently was ~2.4%.4

I estimate that this indexation factor benefitted ~33% of ACL’s pathology services, contributing to ~0.80 percentage points (ppt) of revenue growth in H1’26.

Investors’ focus on pricing misses the growth potential from volume and mix shift.

Since FY2017, overall benefits paid for pathology services under the Medicare system increased ~5% p.a.5 This was mainly driven by 3% volume growth. Despite no annual indexation, fees per service grew ~2% p.a. because of favourable shifts in service mix.

Even without annual indexation, the industry has grown and will likely continue growing revenue at ~MSD p.a., supported by Australia’s growing and ageing population.

People aged over 65 years are the largest users of pathology services, consuming 38% of all services in FY2020 and this population cohort is estimated to grow faster than the general population at a CAGR of 2.9% between FY2020 and FY2030.6

Good business, temporary headwinds?

Headline revenue decline is mainly driven by ACL exiting unprofitable business. ACL’s revenue declined -1.0% YoY (-AUD 3.8mn) in H1’26. At first glance, this is bad.

However, ACL explained that the revenue decline was mainly driven by the company exiting unprofitable ACCs (-AUD 8.2 mn) and unprofitable public hospital/commercial contracts (-AUD 1.4 mn).7

As a result, underlying EBIT margin improved from 7.4% in H1’25 to 7.7% in H1’26.

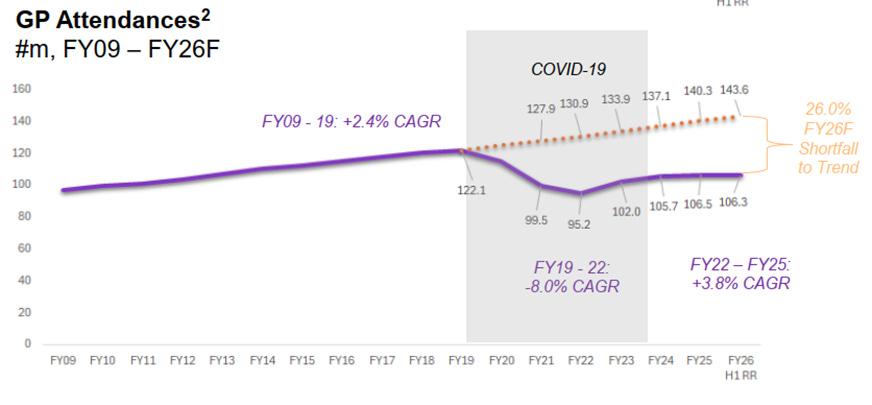

Near-term revenue is likely flat, driven by lower GP attendance. General practitioners (GP) are the largest referrers of pathology tests, ordering approximately 70% of Medicare funded tests.8

In Feb 2026, ACL lowered its FY2026 mid-point revenue guidance by -4%. This was largely driven by weaker-than-expected GP attendance.

The chart below shows that GP attendance in Australia remains below trend and was essentially flat in H1’26.

Source: ACL (2026)

Survey data from the Australian Bureau of Statistics (ABS) suggests this is partly because of the increasing cost of GP services.

The survey shows the percentage of people who said they avoided going to the GP at least once in a year due to the cost is now at the highest level in the 11-year period the survey covers.9

But GP attendance expected to return to growth. From 1 Nov 2025, the Australian government expanded the bulk billing incentives (BBI) to all Australians and created an additional new incentive payment for GPs that bulk bill every patient.10

As a result, the overall bulk billing rate has increased from 77% to 81% between Nov 2025 and Jan 2026. The number of registered Medicare Bulk Billing Practices increased almost +60%.11

GP attendance is expected to rise over the next six months. Because of the lag between a GP’s referral and the patient going for the pathology service, I expect the benefits to flow to ACL only after FY2026.

More efficient. FY2026 guidance downgrade overshadows the quality of the business.

At 18% revenue market share, ACL is almost half the size of HLS (~30%). Despite that, ACL earns 8% return on assets (ROA) while HLS is still suffering losses.

ACL attributes this mainly to the fact that they are the only national pathology provider with a single national Laboratory Information System (LIS) (operating system).

This reduces labour costs. Pathologists from different states can analyse samples across the nation, increasing labour utilization rate. ACL’s labour cost is only ~43% of revenue, compared to the 50%+ reported by HLS.

Capital returns?

Attractive capital returns. In the last twelve months, share buybacks amounted to ~AUD 25 mn and dividends were ~AUD 24 mn. In total, I estimate this is ~150% of free cash flow to firm (FCFF). Capital returns were ~13% of its market capitalisation.

ACL authorised its current share buyback program on 23 Oct 2025, likely in response to the share price falling below the IPO price. The company can still repurchase up to 10.4 mn shares before the program expires in Nov 2026.12

When the share buyback program ends and capital returns normalise to 100% of FCFF, I estimate the sustainable capital return will be ~10% of market capitalisation. This still offers an attractive 5% premium over the Australia 10y government bond.

Catalysts

Private equity takeover? Over the past year, ACL’s share price has fallen around -30%. On 18 May 2026, KKR, a private equity (PE) firm, disclosed it increased its stake to 8.2%, up from 7.2%.

KKR first disclosed its substantial stake (>5%) in ACL around Jul 2024.13 At that time, ACL’s share price was higher at around AUD 2.60.

KKR has shown interest in Australia’s healthcare industry. In Apr 2022, KKR led a consortium to buy Ramsay Health Care Limited (RHC AU), one of Australia’s largest private-hospital operators.14

This offers some downside protection. If ACL’s share price continues to deteriorate despite improving business performance, the probability of a privatisation should increase.

Factors to focus on

Probability and timing of recovery. The expansion of the BBI to all Australians and the introduction of additional incentive payments has increased the GP bulk billing rate.

This should help GP attendance recover. Since GPs are the single largest source of referrals to pathology services, higher GP attendance should accelerate volume growth at ACL.

Are there any factors that can break this relationship?

CEO not renewing contract. On 16 Feb 2026, CEO Melinda McGrath announced that she will not renew her contract when it expires on 30 Aug 2026. ACL is currently conducting an executive recruitment process and will announce an update when available.15

At first glance, CEO McGrath’s departure does not raise immediate red flags. The six-month notice period suggests a planned transition. It should also provide ACL sufficient time to identify and integrate a suitable successor.

That said, her resignation still creates some uncertainty. CEO McGrath has been a key part of ACL’s management over the past 10 years.

Management is important, more so in a regulated industry like healthcare. It will be important to keep an eye on who the board chooses as her successor.

Coming up next

I will be diving deeper into ACL over the next few weeks, alongside other companies on my shortlist: MegaStudyEdu Co. Ltd (215200 KS) and Xinyi Solar Holdings Limited (968 HK).

If any of them turn out to be really attractive opportunities, I will publish my thesis on Substack.

Subscribe to receive the updates immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I do not hold any positions in ACL, either long or short. I may change my views, predictions, or personal portfolio positioning at any time without notice.